Healthcare Services

Italy Clinical Diagnostics Market Analysis

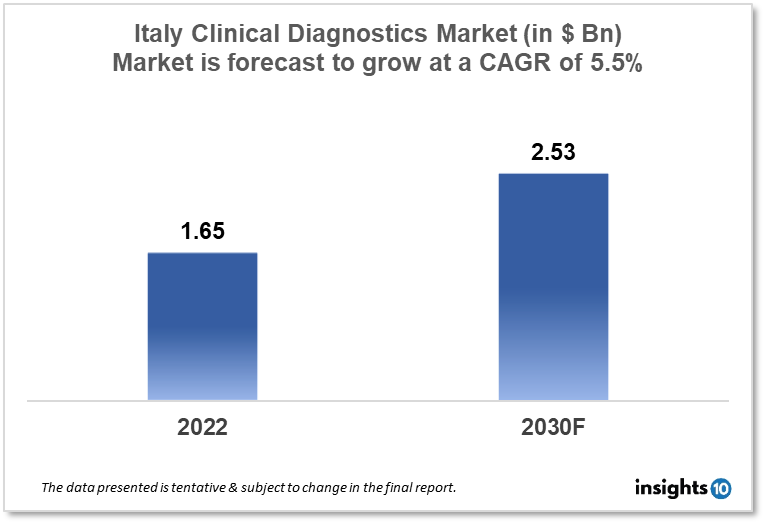

Italy's clinical diagnostic market was valued at $1.65 Bn in 2022 and is estimated to expand at a CAGR of 5.5% from 2022-30 and will reach $2.53 Bn in 2030. One of the main reasons propelling the growth of this market is an increase in technology and the aging population. The market is segmented by type, drug, and distribution channel. Some key players in this market are Abbott, BD, bioMérieux, Sysmex, Giesse Diagnostics Srl, Diagnostic Center NSL Italy, Sentinel Diagnostics, DiaSorin, Menarini Diagnostics, Epitech Group and others.

Buy Now

Italy Clinical Diagnostic Market Executive Summary

The Italy clinical diagnostic market was valued at $1.65 Bn in 2022 and is estimated to expand at a CAGR of 5.5% from 2022 to 2030 and will reach $2.53 Bn in 2030. A disease, sickness, or damage is diagnosed based on a patient's signs and symptoms, as well as the patient's health history and physical exam. Italy's clinical diagnostics market is an important component of the country's healthcare sector. Italy has one of Europe's largest healthcare marketplaces with a vast number of hospitals, clinical laboratories, and research facilities.

The COVID-19 pandemic has also had a significant impact on the clinical diagnostics market in Italy, with an increased demand for diagnostic tests for the virus. The government has taken steps to increase the capacity of diagnostic laboratories to meet the rising demand for testing. Overall, the clinical diagnostics market in Italy is expected to continue to grow in the coming years, driven by increasing demand for early disease detection and personalized medicine, as well as government initiatives to improve healthcare infrastructure.

Market Dynamics

Market Growth Drivers

Italy has a high prevalence of chronic diseases such as diabetes, cardiovascular diseases, and cancer. According to the Global Burden of Disease Study, in 2019, cardiovascular diseases accounted for 34.6% of deaths in Italy, while cancer accounted for 28.7%. This increasing burden of chronic diseases is driving the demand for clinical diagnostics in the country. Italy has one of the largest populations of elderly individuals in Europe.

According to the World Population Prospects 2019, the population aged 65 years and above in Italy was 13.7 Mn in 2020 and is expected to reach 16.6 Mn by 2050. The elderly population is more susceptible to chronic diseases, which is driving the demand for clinical diagnostics. There is a growing awareness among people in Italy regarding the importance of early disease detection. This is driving the demand for diagnostic tests, especially for cancer and infectious diseases. There is a growing trend towards personalized medicine in Italy, where treatments are tailored to individual patients based on their genetic makeup and other factors. This is driving the demand for advanced diagnostic tests such as molecular diagnostics. The Italian government has taken steps to improve healthcare infrastructure and increase investment in healthcare. For example, the National Health Service (SSN) has launched a strategic plan for 2020-2022 to improve the quality and efficiency of healthcare services in the country.

Market Restraints

The Italian healthcare system is facing budget constraints, which are putting pressure on healthcare providers to contain costs. This has led to a reduction in reimbursement rates for diagnostic tests, which could affect the profitability of diagnostic companies. The Italian regulatory environment for medical devices and diagnostic tests is becoming increasingly stringent, which could increase the time and cost required to bring new products to market. The clinical diagnostics industry requires a highly skilled workforce, including pathologists, laboratory technicians, and biomedical engineers. However, there is a shortage of skilled workers in Italy, which could affect the industry's growth potential. The clinical diagnostics market in Italy is highly competitive, with the presence of large multinational companies as well as local players. This could lead to price pressure and could affect the profitability of diagnostic companies. The COVID-19 pandemic has also presented significant challenges for the clinical diagnostics market in Italy. The pandemic has disrupted the supply chain of diagnostic products, leading to shortages of critical testing equipment and reagents. In addition, the pandemic has led to a reduction in demand for non-COVID-19 related diagnostic tests, which has affected the revenue of diagnostic companies.

Competitive Landscape

Key Players

- Abbott

- F. Hoffmann-La Roche

- Thermo Fisher Scientific

- Sysmex

- BioMérieux

- Giesse Diagnostics Srl

- Diagnostic Center NSL Italy

- Sentinel Diagnostics

- DiaSorin: DiaSorin is a leading Italian diagnostic company that specializes in developing and manufacturing diagnostic tests for infectious diseases, endocrinology, and immunology. The company was founded in 2000 and is headquartered in Saluggia, Italy

- Menarini Diagnostics Italia: A. Menarini Diagnostics Italia is a subsidiary of the Menarini Group and is based in Florence, Italy. The company develops and manufactures diagnostic tests for hematology, immunology, and microbiology

- Epitech Group: Epitech Group is an Italian company that specializes in developing and manufacturing diagnostic tests for infectious diseases, oncology, and molecular diagnostics. The company also provides laboratory automation solutions and software

Healthcare Policies and Regulatory Landscape

The healthcare policy and regulatory framework in Italy for clinical diagnostics is overseen by the Italian Ministry of Health and the Italian Medicines Agency (AIFA). The framework consists of various laws, regulations, and guidelines that govern the development, production, marketing, and distribution of medical devices and diagnostic tests. AIFA is responsible for the authorization and monitoring of medical devices and diagnostic tests in Italy. It provides guidelines and requirements for the registration and approval of these products.

Italian Medical Devices Regulation (MDR), which came into effect on May 26, 2021, establishes a new regulatory framework for medical devices in Italy. It replaces the previous Medical Devices Directive (MDD) and introduces new requirements for clinical evidence and post-market surveillance.

Italy Good Manufacturing Practice (GMP) follows the European Union's GMP guidelines, which provide standards for the production and quality control of medical devices and diagnostic tests.

The International Organization for Standardization (ISO) provides various standards for medical devices and diagnostic tests, including ISO 13485 for quality management systems and ISO 15189 for medical laboratories.

The regulatory framework for clinical diagnostics in Italy is designed to ensure the safety and efficacy of diagnostic tests, as well as to protect public health. Companies that wish to market their products in Italy must comply with the relevant regulations and guidelines, which may require significant time and resources.

Reimbursement Scenario

In Italy, the National Health Service (SSN) provides universal healthcare coverage to all citizens and legal residents. The SSN is funded by taxes and contributions from employees and employers, and it covers most of the costs of medical treatments, including diagnostic tests. Reimbursement for diagnostic tests in Italy is regulated by AIFA. AIFA establishes a list of diagnostic tests that are eligible for reimbursement under the SSN, known as the Essential Levels of Assistance (LEA). The LEA includes a range of diagnostic tests, including laboratory tests, imaging tests, and genetic tests.

To be eligible for reimbursement under the SSN, diagnostic tests must meet certain criteria, such as being clinically necessary and cost-effective. The reimbursement rate for diagnostic tests is determined by AIFA based on the cost of the test, the expected volume of tests, and the clinical benefits of the test. Private healthcare insurance also exists in Italy, and individuals can choose to purchase additional insurance coverage for diagnostic tests that are not covered under the SSN or to receive faster.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Italy Clinical Diagnostics Market Segmentation

By Test

- Lab Test

- Imaging Test

- Other Tests

By Product

- Instruments

- Reagents

- Other Products

By End User (Revenue, USD Bn)

- Hospital Laboratory

- Diagnostic Laboratory

- Point-of-care Testing

- Other End Users

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Brazil Nootropics Market Analysis

Healthcare Services

Japan Clinical Trial Packaging Market Analysis

Healthcare Services

Egypt In Vitro Fertilisation (IVF) Service Market Analysis

Related reports (by geography)

Rare Diseases

Italy Rett Syndrome Drugs Market Analysis

Healthcare Services

Italy Dry Eye Disease Diagnostic Market Analysis

Rare Diseases

Italy Huntington's Disease Drugs Market Analysis

Rare Diseases