Pharmaceuticals

Italy Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Analysis

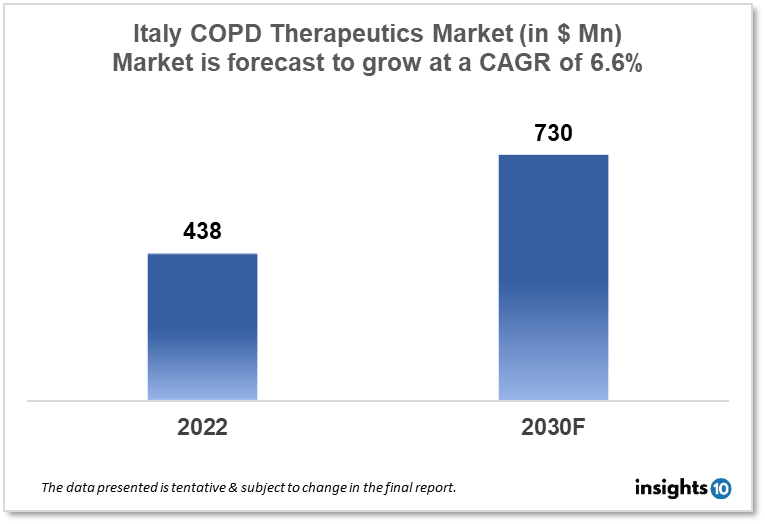

Italy's Chronic Obstructive Pulmonary Disease (COPD) therapeutics market was valued at $438 Mn in 2022 and is estimated to expand at a CAGR of 6.6% from 2022 to 2030 and will reach $730 Mn in 2030. One of the main reasons propelling the growth of this market is the increasing prevalence rate of an aging population. The market is segmented by drug class and by distribution channel. Some key players in this market are Menarini Group, Chiesi Pharma, Almirall, Molteni Pharmaceutics, Boehringer Ingelheim Pharmaceuticals, Novartis, Pfizer, Teva Italy Limited, and others.

Buy Now

Italy Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Executive Summary

Italy's Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market was valued at $438 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 6.6% from 2022 to 2030 and will reach $730 Mn in 2030. The main cause of illness and mortality globally is a chronic obstructive pulmonary disease (COPD), a lung condition that worsens breathing problems. A sizable fraction of the population in Italy is afflicted by COPD, especially those who are 65 and older. In the upcoming years, the COPD therapeutics market in Italy is anticipated to expand as a result of a number of factors, including an aging population, an increase in COPD prevalence, and the availability of cutting-edge treatment alternatives.

Market Dynamics

Market Growth Drivers

Italy has one of the oldest populations in the world, with an estimated 22% of the population aged 65 and over. Older adults are more likely to develop COPD, which is a major contributor to the growth of the market. According to the Italian National Institute of Statistics, the percentage of people aged 65 and above is expected to increase to 31% by 2050. COPD is a common respiratory disease in Italy, with an estimated 3.5 Mn people affected. The prevalence of COPD is expected to increase due to risk factors such as smoking, air pollution, and occupational exposure to dust and chemicals. Advances in medical research and technology have led to the development of new and innovative therapies for COPD, including combination therapies and drugs that target specific molecular pathways involved in the disease. These innovative treatments are likely to drive growth in the market.

Market Restraints

One of the major challenges in the Italy COPD therapeutics market is the high cost of medications. COPD is a chronic disease that requires ongoing treatment, and the cost of medication can be a significant burden for patients and healthcare systems. This can limit access to effective treatments and impact market growth. Despite being a common disease, many people with COPD in Italy are undiagnosed and untreated. This can be due to a lack of awareness about the disease and a lack of routine screening. The low diagnosis rate can limit market growth and prevent patients from accessing appropriate treatments. The Italy COPD therapeutics market is highly competitive, with several major players offering similar products. This can lead to pricing pressure and limit the ability of companies to maintain market share and profitability.

Competitive Landscape

Key Players

- Menarini Group: Menarini is an Italian pharmaceutical company that offers a range of medications for respiratory diseases, including COPD. The company offers bronchodilators, corticosteroids, and combination therapies.

- Chiesi Pharma

- Almirall

- Molteni Farmaceutici

- Astellas Pharma

- AstraZeneca

- Boehringer Ingelheim Pharmaceuticals

- Novartis

- Pfizer

- Teva Italy Limited

Healthcare Policies and Regulatory Landscape

The healthcare policy and regulatory framework in Italy play an important role in shaping the COPD therapeutics market. The Italian healthcare system is based on a universal coverage model, with public and private providers delivering services to citizens. In Italy, the Italian Medicines Agency (AIFA) is responsible for regulating the pharmaceutical industry, including the approval and pricing of medications. AIFA sets prices for medications based on a cost-effectiveness evaluation and considers factors such as therapeutic value, clinical benefits, and the burden of disease.

The Italian government also plays an important role in shaping the healthcare policy framework. The National Health Plan (NHP) is a document that outlines the strategic objectives and priorities of the Italian healthcare system. The NHP includes a focus on the prevention and early diagnosis of chronic diseases, including COPD. The Italian government has also introduced policies aimed at reducing smoking rates, a major risk factor for COPD. These policies include the prohibition of smoking in public places, increased taxes on tobacco products, and public awareness campaigns.

In recent years, the Italian government has also introduced measures aimed at promoting the use of innovative therapies for COPD. For example, the government has introduced incentives for companies to invest in the research and development of new treatments and has introduced programs to facilitate patient access to innovative therapies.

Reimbursement Scenario

In Italy, healthcare is publicly funded and available to all citizens and permanent residents. However, some individuals may have private health insurance through their employer or purchase it independently. Private insurance plans may have different reimbursement policies and may not cover all of the same drugs as public drug plans. Many provincial drug plans require patients to pay a portion of the cost of their prescription drugs, known as a co-payment. The co-payment amount varies by province and may be based on income or other factors. Some provincial drug plans have tiered formularies, which categorize drugs into different tiers based on their cost and effectiveness. Drugs in higher tiers may have higher copayments or may not be covered at all.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Italy Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Segmentation

By Drug Class

Bronchodilators: Bronchodilators are medications that help to relax the muscles around the airways, making it easier to breathe. These can be further classified as short-acting or long-acting bronchodilators.

Corticosteroids: Corticosteroids are anti-inflammatory medications that can help reduce swelling and inflammation in the airways. These can be used alone or in combination with bronchodilators.

Combination therapies: Combination therapies combine bronchodilators and corticosteroids in a single medication. These are often used for patients with more severe COPD.

Phosphodiesterase-4 inhibitors: Phosphodiesterase-4 inhibitors are medications that help to reduce inflammation and improve airflow in the lungs.

Others: Other medications that may be used to treat COPD include mucolytics, oxygen therapy, and vaccines for influenza and pneumococcal disease.

By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Brazil Encephalitis Vaccines Market Analysis

Pharmaceuticals

Argentina Sleep Disorders Market Analysis

Pharmaceuticals

Malaysia Cord Blood Banking Service Market Analysis

Related reports (by geography)

Rare Diseases

Italy Sickle Cell Disease Drugs Market Analysis

Pharmaceuticals

Italy Liver Cancer Therapeutics Market Analysis

Rare Diseases