Pharmaceuticals

Indonesia Oncology Therapeutics Market Analysis

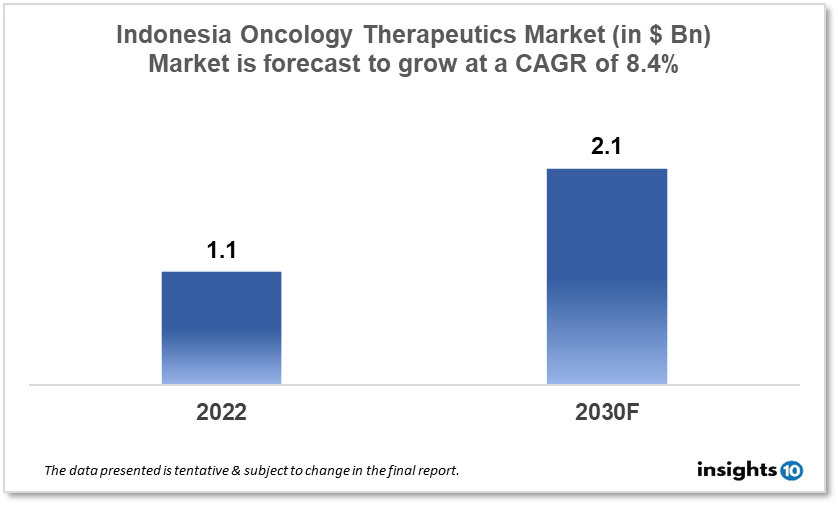

By 2030, it is anticipated that the Indonesia Oncology Therapeutics Market will reach a value of $2.1 Bn from $1.1 Bn in 2022, growing at a CAGR of 8.4% during 2022-2030. The Oncology Therapeutics Market in Indonesia is dominated by a few domestic pharmaceutical companies such as Dexa Medica, Kalbe Farma, and Tempo Scan Pacific. The Oncology Therapeutics Market in Indonesia is segmented into different types of cancer and different therapy type. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for Indonesia Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

Indonesia Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the Indonesia Oncology Therapeutics Market will reach a value of $2.1 Bn from $1.1 Bn in 2022, growing at a CAGR of 8.4% during 2022-2030.

Indonesia is a lower middle-income, developing country located in Southeastern Asia between the Indonesian Ocean and the Pacific Ocean. Overall, the most prevalent malignancies in Indonesia are lung (11.58 %), breast (11.55 %), and colorectum (10.23 %), with lung (18.43 %), liver and bile duct (9.91 %), and stomach (10.23 %) having the greatest death rates (8.19 %). Currently, about 70% of all diseases, including cancer, are noncommunicable, and this ratio will climb as Indonesia completes its epidemiological shift. In 2020, the number of incident instances of oncological diseases in Indonesia is expected to be 396,000. Indonesia's government spent 3.4% of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers

Patients with cancer in Indonesia are eventually directed to both Dharmais National Cancer Center and Cipto Mangunkusumo Hospital, both of which are public hospitals, except for a few patients who are treated at private institutions or fly overseas. The National Healthcare Insurance (BPJS-JKN) now covers around 82.3 % of Indonesia's 270 Mn inhabitants, including the poor (whose contributions are paid for by the government). Low labour costs and a demographic dividend provide a competitive advantage while doing business in Indonesia. These aspects could boost Indonesia's Cancer Therapeutics market.

Market Restraints

Admission to cancer care in Indonesia is limited, particularly in provincial districts with few or no illness treatment offices. Patients commonly need to travel long distances to receive treatment, which can be costly and time-consuming. Indonesia is vulnerable to fluctuations in Chinese demand, as well as continuous corruption and a lack of openness. These factors may deter new entrants into the Indonesia Oncology Therapeutics Market.

Competitive Landscape

Key Players

- Dexa Medica: Dexa Medica is an Indonesian pharmaceutical company that produces a range of cancer therapeutics, including chemotherapy drugs and targeted therapies. The company has a strong focus on research and development and has several innovative cancer drugs that are currently in clinical development

- Kalbe Farma Tbk: Kalbe Farma Tbk is an Indonesian pharmaceutical company that produces a range of cancer therapeutics, including chemotherapy drugs and targeted therapies. The company has a strong presence in the Indonesian market and is expanding into other countries in Southeast Asia

- Pharos Indonesia: Pharos Indonesia is an Indonesian pharmaceutical company that produces a range of cancer therapeutics, including chemotherapy drugs and targeted therapies. The company has a strong focus on research and development and has several innovative cancer drugs that are currently in clinical development

- Tempo Scan Pacific Tbk: Tempo Scan Pacific Tbk is an Indonesian pharmaceutical company that produces a range of cancer therapeutics, including chemotherapy drugs and targeted therapies. The company has a strong presence in the Indonesian market and is expanding into other countries in Southeast Asia

Notable Recent Deals

January 2023: The Dharmais National Cancer Center in West Jakarta, Indonesia's government-owned key cancer care facility and major cancer referral institute, has begun a collaboration with the University of Indonesia (Depok City, West Java, Indonesia), the University of New Mexico (Albuquerque, NM, USA), and the Tata Memorial Centre (Mumbai, India) as part of government-led efforts to improve cancer diagnosis and treatment. The collaboration is involved in three new programmes: Project Extension for Community Healthcare Outcomes (ECHO), Cancer Patient Navigation (NAPAK), and an oncology nurse capacity-building effort.

October 2022: To improve access to critical leukaemia therapy in seven countries, including Indonesia, Novartis, the world's largest pharmaceutical firm with headquarters in Switzerland, and an UN-backed public health organisation signed the first-ever licence agreement for cancer medicine.

Healthcare Policies and Reimbursement Scenarios

The National Agency of Drug and Food Control (BPOM) and the Social Security Agency for Health regulate the regulation and payment of cancer therapies in Indonesia (BPJS Kesehatan). In Indonesia, the administrative body liable for the endorsement and guideline of restorative items, including malignant growth therapeutics, is the National Agency of Drug and Food Control (NA-DFC), otherwise called Badan Pengawas Obat dan Makanan (BPOM).In the public medical care framework, the expense of disease therapies, including disease therapeutics, is halfway covered by the National Health Insurance (Jaminan Kesehatan Nasional, or JKN). The repayment of disease therapeutics under the JKN framework in Indonesia is dependent upon the National Formulary (Formularium Nasional, or FN), which frames the qualified medications and the related paces of inclusion.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Indonesia Dermatological Therapeutics Market Analysis

Pharmaceuticals

Singapore Mammography Device Market Analysis

Pharmaceuticals

Malaysia Conjunctivitis Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Indonesia Breast Cancer Therapeutics Market Analysis

Pharmaceuticals

Indonesia TNF Inhibitors Market Analysis

Pharmaceuticals

Indonesia Medical X-ray Market Analysis

Pharmaceuticals