Medical Devices

Indonesia Diabetes Devices Market Analysis

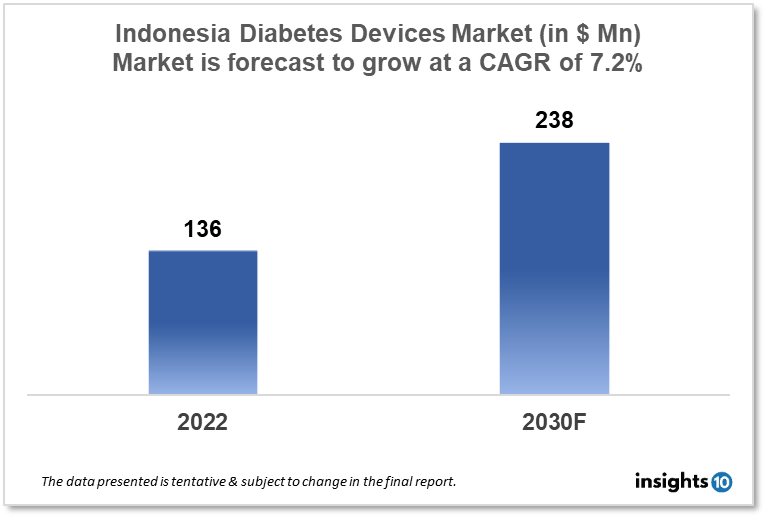

Indonesia's Diabetes Devices Market is expected to witness growth from $136 Mn in 2022 to $238 Mn in 2030 with a CAGR of 7.20% for the forecasted year 2022-2030. With roughly 10 million sufferers, diabetes is a condition that is very common in Indonesia. This indicates a sizable market for diabetes devices. The market is segmented by type and by the end user. Some key players in this market include PT. Ravindra Putrapratama, Tawada Healthcare, Johnson & Johnson, Medtronic, Roche, Ascensia Diabetes Care and Dexcom.

Buy Now

Indonesia Diabetes Devices Healthcare Market Executive Analysis

Indonesia's Diabetes Devices Market is at around $136 Mn in 2022 and is projected to reach $238 Mn in 2030, exhibiting a CAGR of 7.20% during the forecast period. Between 2022 and 2028, Indonesia is expected to increase its healthcare spending by $30.18 billion. Spending is projected to total $69.3 billion in 2028. Indonesia is viewed as a newly industrializing country with a middle-income level. In terms of GDP, it is the seventh-largest economy in the globe, while nominal GDP places it in 17th place. The $40 billion Internet industry in Indonesia is expected to grow to $130 billion by 2025.

Indonesia ranked seventh in the globe in terms of the number of people with diabetes in 2021 with 10.3 million cases. In people aged 20 to 79, the prevalence of diabetes was projected to be 6.7% in 2021. With an expected 1.4 million new cases of diabetes being diagnosed in 2021 alone, Indonesia has a high prevalence of the disease as well. This indicates that Indonesia has among the greatest incidences of diabetes worldwide. In Indonesia, type 2 diabetes accounts for nearly 95% of all instances and is the most prevalent type of disease. Genetic predisposition, an inactive lifestyle, an unhealthy diet, and obesity are risk factors for type 2 diabetes in Indonesia.

In Indonesia, tools for managing blood glucose levels in individuals with diabetes include diabetes devices. At home, blood glucose levels are checked using blood glucose meters. They are straightforward and simple to use, and they can assist diabetics in routinely monitoring their blood glucose levels. In order to constantly administer insulin throughout the day, insulin pumps are used. They can assist diabetics in maintaining more stable blood glucose levels because they can be programmed to deliver precise amounts of insulin at particular times. Rather than using conventional insulin injections, insulin pens are used to deliver the medication. They can be used at home or while travelling because they are lightweight and portable. Improvements in blood glucose management, a decreased chance of complications, and an improvement in quality of life are all advantages of using diabetes devices in Indonesia. Diabetes gadgets can also aid patients in understanding their disease, which can improve self-management and prompt medical attention.

Market Dynamics

Market Growth Drivers

With roughly 10 million sufferers, diabetes is a condition that is very common in Indonesia. This indicates a sizable market for diabetes devices, such as insulin pumps, glucose monitoring systems, and other tools for managing the condition. People with diabetes in Indonesia are finding it simpler to control their condition due to developments in diabetes device technology, such as Continuous Glucose Monitoring (CGM) systems. Manufacturers now have more chances to create and market cutting-edge products. In Indonesia, people are becoming more and more conscious of the significance of managing their diabetes. This is boosting the demand for diabetes devices and opening doors for companies to produce new goods and increase their market share.

Market Restraints

In Indonesia, both patients and healthcare professionals lack adequate information about diabetes and its management. If people were unaware of the advantages or how to use diabetes devices properly, they might not be used as frequently as they could be. The high expense of diabetes supplies like insulin pumps, continuous glucose monitoring systems, and glucose meters prevents many Indonesian patients from purchasing them. As a consequence, there might be a decrease in the market's size and demand for these devices.

Competitive Landscape

Key Players

- PT. Ravindra Putrapratama (ID)

- Tawada Healthcare (ID)

- Johnson & Johnson

- Medtronic

- Roche

- Dexcom

- Ascensia Diabetes Care

Recent Notable Deals

September 2022: To sell its Eversense continuous glucose monitoring system in Indonesia, Senseonics announced in September 2022 that it had teamed up with PT Transmedic Indonesia. Through this partnership, individuals with diabetes in the nation should have easier access to technology.

2021: In Indonesia, the MiniMed 770G insulin device was introduced by Medtronic in 2021. In order to help people with diabetes better control their condition, this pump uses artificial intelligence to automatically modify insulin delivery based on a patient's glucose levels.

Healthcare Policies and Regulatory Landscape

The National Agency of Drug and Food Control and the Ministry of Health (BPOM), and other regulatory agencies oversee the healthcare policies and regulatory framework in Indonesia's market for diabetes devices. Before being distributed in Indonesia, diabetes devices, such as insulin pumps and glucose meters, must be registered with BPOM. Manufacturers must submit information about the effectiveness and safety of their products as part of the registration procedure. The BPOM also establishes quality and safety requirements for diabetes devices sold in Indonesia. To guarantee that their products are safe and effective for use by individuals with diabetes, manufacturers must abide by these standards. Before they can be marketed in Indonesia, diabetes devices imported into that country must pass testing and certification requirements set forth by the BPOM. When shipping goods from Indonesia to other nations, manufacturers must also adhere to export laws.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Diabetes Devices Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into blood glucose monitoring systems, insulin delivery systems, and mobile applications for managing diabetes within the type segment. Due to its convenience, ease of use, and usefulness in providing patients and healthcare professionals with real-time insights regarding diabetic conditions for integrated diabetes management, the segment for diabetes management mobile applications is anticipated to grow at the highest rate during the forecast period. Bare-metal Stents

- Blood glucose monitoring systems

- Self-monitoring blood glucose monitoring systems

- Continuous glucose monitoring systems

- Test strips/Test papers

- Lancets/Lancing Devices

- Insulin delivery Devices

- Insulin pumps

- Insulin pens

- Insulin syringes and needles

- Diabetes management mobile applications

By End User (Revenue, USD Billion):

The diabetes market is divided into hospitals & specialty clinics and self & home care, based on the end user.

- Hospitals & Specialty Clinics

- Self & Home Care

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

India Bio-Implant Market Analysis

Medical Devices

New Zealand Contraceptive Devices Market Analysis

Medical Devices

Vietnam Bariatric Surgery Devices Market Analysis

Related reports (by geography)

Pharmaceuticals

Indonesia Remicade Biosimilar Market Analysis

Medical Devices

Indonesia Cardiac Surgery Instruments Market Analysis

Healthcare Services

Indonesia Bioinformatics Market Analysis

Pharmaceuticals