Pharmaceuticals

Indonesia Compression Therapy Market Analysis

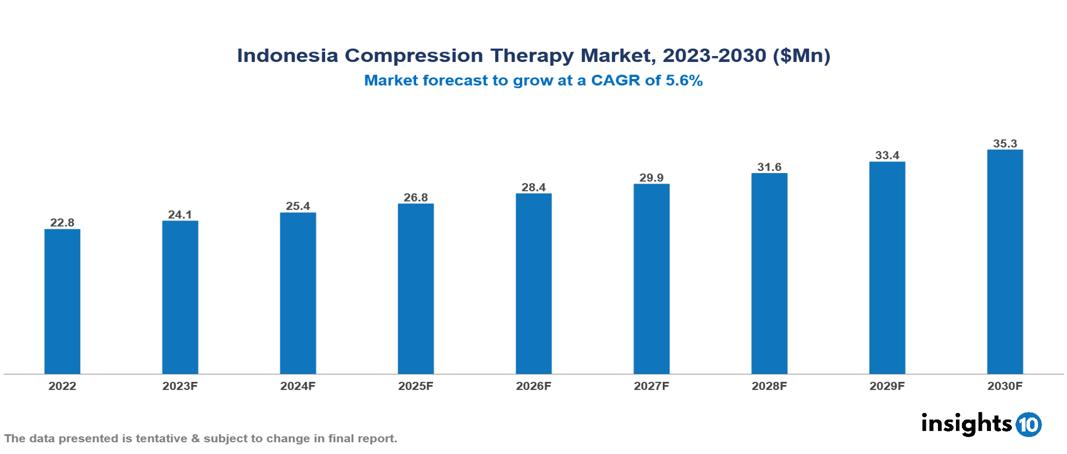

Indonesia's Compression Therapy Market was valued at $23 Mn in 2022 and is estimated to reach $35 Mn in 2030, exhibiting a CAGR of 5.6% during the forecast period. The increasing occurrence of venous disorders such as leg ulcers, deep vein thrombosis, lymphedema, varicose veins, and blood clots is a major factor contributing to the expansion of the compression therapy market. Major participants in this sector include companies like Medtronic plc, Sigvaris, Bauerfeind, Juzo, McKesson Corporation, Cardinal Health, BSN Medical, Hartmann, Lohmann & Rauscher, and Molnlycke Health Care.

Buy Now

Indonesia Compression Therapy Market Executive Summary

Indonesia Compression Therapy Market was valued at $23 Mn in 2022 and is estimated to reach $35 Mn in 2030, exhibiting a CAGR of 5.6% during the forecast period.

Compression therapy, a medical procedure commonly used on limbs, aims to enhance blood circulation and reduce swelling. It is frequently employed for conditions like lymphedema, venous disorders, and specific edemas, with the primary goal of improving venous blood flow and preventing fluid buildup in tissues. Depending on the severity and individual needs, compression therapy may take various forms, such as elastic stockings, sleeves, or bandages. Techniques like compression wraps involve applying multiple layers for graduated compression, while intermittent pneumatic compression (IPC) mimics natural muscle contractions to aid venous return. Consulting with a healthcare provider is crucial to determine the most suitable technique and compression level, especially when developing comprehensive treatment plans for issues like poor circulation, swelling, or fluid retention.

In Indonesia, Chronic Venous Disease (CVD) presents a significant health concern, with a prevalence of approximately 26% for the C1 stage (visible varicose veins) and 8% for the C3 stage (skin changes and edema). Deep Vein Thrombosis (DVT) also poses a substantial risk, with a notably high incidence of 40.3%, suggesting a potentially higher prevalence compared to Western populations. Several factors contribute to the increased risk of these venous conditions in Indonesia. Rising obesity rates in the country may contribute to an elevated risk of CVD, while frequent childbearing, particularly common in certain regions, is identified as a risk factor for women. Lifestyle factors such as standing occupations, limited physical activity, and poor diet are likely contributors as well. Additionally, genetic predispositions within the Indonesian population could vary, further influencing susceptibility to venous conditions.

Compression therapy integration with telehealth platforms is a strategic approach toward improving patient convenience and access. Prominent corporations such as Bauerfeind and Juzo are actively participating in this endeavor, providing telehealth solutions that facilitate remote patient monitoring and assistance during compression therapy. This creative strategy offers a more individualized and patient-centred way to manage compression therapy, in line with the growing trend of digital health and adapting to changing patient needs.

Market Dynamics

Market Growth Drivers

Rising Prevalence of Venous Disorders: A significantly elevated rate of 40.3% for deep vein thrombosis (DVT) and the potential rise in chronic venous disease (CVD) attributed to lifestyle elements such as obesity and reduced physical activity. The expanding number of affected individuals is fuelling the need for compression therapy interventions.

Rising Geriatric Population: In 2022, Indonesia's senior citizen population comprises almost 19 Mn individuals, making up 9.6% of the overall population. Projections from the United Nations suggest that this figure is set to increase significantly, reaching 25% by 2050. The surge in demand for compression therapy in Indonesia is primarily fuelled by the aging demographic. The country is confronting the challenges posed by a swiftly growing elderly population, leading to a higher prevalence of conditions such as lymphedema, varicose veins, and cardiovascular diseases.

Increasing Healthcare Awareness: The increasing awareness among healthcare professionals and the general public about the benefits of compression therapy is propelling the market's growth. The market is growing as a result of educational initiatives, professional and athlete support, and other factors.

Market Restraints

High Cost of Products: Expensive compression garments, particularly from international brands, can be costly. For a significant segment of the populace, especially those with limited disposable income or those who depend on public healthcare programs, this could be an obstacle to access.

Low Patient Compliance: Consistently wearing compression apparel throughout the day may cause discomfort and restrictions, diminishing adherence and effectiveness of the treatment. This is particularly evident in non-medical scenarios such as sports recovery or daily wear. Insufficient patient education and awareness regarding the lasting advantages of compression therapy also play a role in fostering low compliance.

Lack of Insurance Coverage: Comprehensive insurance options for compression therapy are not widely accessible in Indonesia, thereby restricting patients' ability to receive treatment, particularly for preventive or extended durations.

Healthcare Policies and Regulatory Landscape

The National Agency of Drug and Food Control (Badan Pengawas Obat dan Makanan, or BPOM) and the Ministry of Health (Kemenkes) collaborate closely to control the pharmaceutical treatment landscape in Indonesia. To guarantee the effectiveness, safety, and quality of pharmaceutical marketing authorizations, BPOM plays a crucial role in their approval and oversight. The Ministry of Health provides overarching guidelines for healthcare, shaping the standards adhered to by these medications. The availability and payment processes for medicines are greatly impacted by the national health insurance program, Jaminan Kesehatan Nasional (JKN). Ongoing efforts to establish health technology assessment mechanisms and enact laws governing clinical trials and research also impact the review and approval processes in this regulatory environment.

Competitive Landscape

Key Players

- Medtronic plc

- Sigvaris

- Bauerfeind

- Juzo

- McKesson Corporation

- Cardinal Health

- BSN Medical

- Hartmann

- Lohmann & Rauscher

- Molnlycke Health Care

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Indonesia Compression Therapy Market Segmentation

By Product

- Compression Bandages

- Compression Wraps

- Compression Stockings

- Compression Tapes

- Compression Pumps

- Compression Braces

- Other Compression Garments

By Technique

- Static Compression Therapy

- Dynamic Compression Therapy

By Application

- Varicose Vein Treatment

- Deep Vein Thrombosis Treatment

- Lymphedema Treatment

- Leg Ulcer Treatment

- Other Applications

By Distribution Channel

- Pharmacies and Retailers

- Hospitals and Clinics

- E-Commerce Platforms

- Home Care Settings

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

France Tetanus Toxoid Vaccine Market Analysis

Pharmaceuticals

Australia Acne Drugs Market Analysis

Pharmaceuticals

Germany Seasonal Flu Vaccine Market Analysis

Related reports (by geography)

Medical Devices

Indonesia Dental Endodontics Market Analysis

Pharmaceuticals

Indonesia Oral Care Market Analysis

Pharmaceuticals