Pharmaceuticals

Indonesia Cardiovascular Diseases Therapeutics Market Analysis

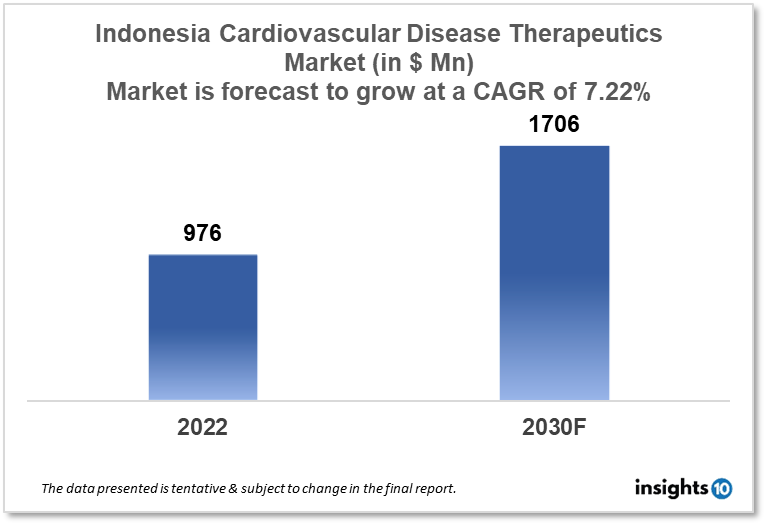

The Indonesia cardiovascular disease therapeutics is projected to grow from $976 Mn in 2022 to $1,706 Mn in 2030 with a CAGR of 7.22% for the year 2022-2030. Rapid urbanization leading to shifting lifestyle behaviours in the population of Indonesia resulting in the increased incidence of cardiovascular diseases is responsible for the growth of the market. The Indonesia cardiovascular disease therapeutics market is segmented by disease indication, drug type, route of administration, drug classification, mode of purchase, and by the end user. Combiphar, Ivosights, and Bayer are the major players in the Indonesia cardiovascular disease therapeutics market.

Buy Now

Indonesia Cardiovascular Disease Therapeutics Market Executive Analysis

The Indonesia cardiovascular disease therapeutics market size is at around $976 Mn in 2022 and is projected to reach $1,706 Mn in 2030, exhibiting a CAGR of 7.22% during the forecast period. In 2023, the Indonesian ministry will put aside $5.96 billion of the $11 Bn total health budget for health transformation. The transformation of primary services through public education, primary prevention, and secondary prevention, as well as boosting the capacity and competence of primary services, will be accomplished with the aid of $4 Bn, according to the minister. Additionally, $1.2 Bn will be allocated for the transformation of referral services through enhancements to intermediate and tertiary services' accessibility and quality. $96 Mn is allocated for the health security system to strengthen disaster preparedness and the resiliency of the pharmaceutical and medical device industries.

In Indonesia, cardiovascular disease (CVD) is responsible for about one-third of all fatalities, with coronary heart disease (CHD) and stroke being among the top fatalities there. According to estimates, stroke and coronary heart disease (CHD) account for more than 470 000 yearly fatalities in Indonesia. The most popular method for removing clots and restoring blood vessel endothelial membrane elasticity is statin treatment. Aspirin is also the medication that Indonesians use the most frequently for the secondary prevention of CVDs. International recommendations on the primary prevention of CVDs only suggest aspirin if the risk of cardiac events persists for at least 10 years due to aspirin's reported increased risk of bleeding.

Nanomedicine is a convergent science that modifies disease treatment and diagnosis by fusing the disciplines of biology, biochemistry, physics, engineering, genetics, and biotechnology. The problems with the currently used traditional stents are being addressed by the investigation of nano polymeric-coated biodegradable stents. These innovative stents can lessen platelet adhesion rates and enhance drug release characteristics. Extensive study is being done on nanomedicines with various properties and compositions for the treatment of CVDs in Indonesia. They consist of polymeric nanoparticles (NPs), silica-based nanoconjugates, micelles, liposomes, liposomes, exosomes, metallic NPs, dendrimers, composite nanosystems, poly (ethylene glycol)-ated (PEGylated) nanospheres, and immunopurified nanoshells.

Market Dynamics

Market Growth Drivers

In Indonesia, the prevalence of cardiovascular diseases is rising due to rapid urbanization and behavioural shifts like poor diets and insufficient exercise. To manage and treat these conditions, there is an increasing need for efficient cardiovascular disease therapeutics. To enhance the general health of its citizens, the Indonesian government has been increasing its spending on healthcare, including cardiovascular disease therapeutics. This increased spending is anticipated to fuel growth in the Indonesia cardiovascular disease therapeutics market. To increase access to healthcare, the Indonesian government established in place a few programs, including therapeutics for cardiovascular disease. For instance, the government has established a national health coverage program that gives access to reasonably priced healthcare services, such as therapeutics for cardiovascular disease.

Market Restraints

The healthcare system in Indonesia is still being built, especially in remote regions. This may restrict access to cardiovascular disease treatments, especially for people who live outside of big cities. The government's plan for comprehensive health coverage gives people access to reasonably priced medical services, including treatments for cardiovascular diseases. Access to some treatments, however, may be restricted by the reimbursement rules for these procedures. The cost of cardiovascular disease therapeutics can be expensive, especially for novel treatments. This may make these treatments less accessible, especially for those with restricted financial means restricting the growth of Indonesia's cardiovascular disease therapeutics market.

Competitive Landscape

Key Players

- Pharos (IDN)

- Etana Biotechnologies (IDN)

- Herlina Indah (IDN)

- Combiphar (IDN)

- Ivosights (IDN)

- Bayer

- Sun Pharmaceutical

- Novartis

- Mylan

- Teva Pharmaceutical

- Zydus

- Pfizer

- Lupin

Healthcare Policies and Regulatory Landscape

The National Health Insurance (Jaminan Kesehatan Nasional or JKN) scheme, which was introduced in 2014 to provide universal healthcare coverage to all residents, mainly governs cardiovascular healthcare and reimbursement in Indonesia. All Indonesian citizens have access to essential healthcare services, including cardiovascular care, under the JKN program. Indonesia has been making investments to increase accessibility to high-quality cardiovascular care facilities. Improve the standard of care, this entails creating specialized cardiovascular centres and hospitals, expanding the pool of qualified medical personnel, and offering training and educational initiatives. The JKN scheme reimburses for a variety of medical services, including cardiovascular treatment. For some therapies or services, there might be restrictions on coverage and reimbursement rates. For some treatments, patients might also need to cover co-payments or other out-of-pocket costs.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiovascular Disease Therapeutics Segmentation

By Disease Indication (Revenue, USD Billion):

- Hypertension

- Coronary Artery Disease

- Hyperlipidaemia

- Arrhythmia

- Others

By Drug Type (Revenue, USD Billion):

- Antihypertensive

- Anticoagulants

- Antihyperlipidemic

- Antiplatelet Drugs

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Drug Classification (Revenue, USD Billion):

- Branded Drugs

- Generic Drugs

By Mode of Purchase (Revenue, USD Billion):

- Prescription-Based Drugs

- Over-The-Counter Drugs

By End Users (Revenue, USD Billion):

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

China Irritable Bowel Syndrome Drugs Market Analysis

Pharmaceuticals

Finland Infectious Disease Therapeutics Market Analysis

Pharmaceuticals

Philippines Cold Plasma Market Analysis

Related reports (by geography)

Pharmaceuticals

Indonesia Glutathione Market Analysis

Pharmaceuticals

Indonesia Pharmacy Market Analysis

Pharmaceuticals

Indonesia Addiction Therapeutics Market Analysis

Pharmaceuticals