Pharmaceuticals

India Radiotherapy Market Analysis

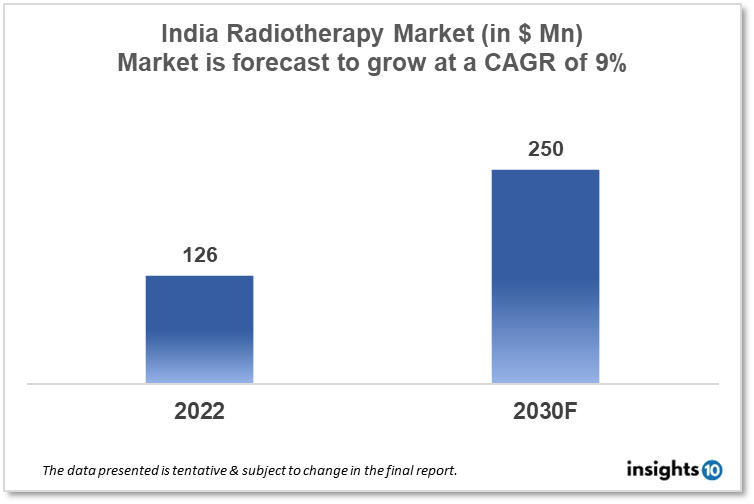

By 2030, it is anticipated that the India Radiotherapy Market will reach a value of $250 Mn from $126 Mn in 2022, growing at a CAGR of 9% during 2022-30. The Radiotherapy Therapeutics Market in India is dominated by a few domestic players such as Bhabha Atomic Research Centre (BARC), HCG Group, and Elekta. The radiotherapy market in India is segmented into different types, technology, procedures, application, and end-user. The major risk factors associated with awareness of radiotherapy shortage of skilled staff, government initiatives and reimbursement policy. The demand for India Radiotherapy is increasing on account of the rise in cancer cases in the country.

Buy Now

India Radiotherapy Market Analysis Summary

By 2030, it is anticipated that the India Radiotherapy Market will reach a value of $250 Mn from $126 Mn in 2022, growing at a CAGR of 9% during 2022-30.

India is a lower middle-income, developing country located in Southern Asia bordering the Arabian Sea and the Bay of Bengal. Cancer's public health burden in India is steadily increasing, with 1.4 Mn new cases projected in 2020. In India, the expected number of cancer patients was 2.7 Mn (2020). In India, between 60% and 75% of cancer patients are treated in private hospitals, where they confront substantial out-of-pocket payments and financial difficulties. The cancer burden in India is predicted to exceed 1.5 Mn cases by 2025. The Rashtriya Arogya Nidhi (RAN) has also established the "Health Minister's Cancer Patient Fund (HMCPF)" to assist cancer patients financially.

In India, radiotherapy centres currently offer either teletherapy alone or combined teletherapy and brachytherapy. Currently, India has 545 teletherapy machines and 22 advanced therapy equipment. India's government spent 3 % of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

In India, about two-thirds of cancer patients require radiation (RT), amounting to 8,00,000 patients per year. India has the greatest growth rate in the APAC radiotherapy market. Annual cancer cases in LMICs are predicted to climb by 30% by 2020, to 10.3 Mn. Radiotherapy programmes, including training courses supplied by the International Atomic Energy Agency (IAEA), are therefore critical for cancer treatment capacity building. These aspects could boost India's, Radiotherapy Market.

Market restraints

The International Atomic Energy Agency's Directory of Radiation Centers (DIRAC) 2012 listed India as well as the poorest Sub-Saharan African country with fewer than one radiotherapy equipment per Mn inhabitants. Based on the number of already installed units in India, this would still result in a shortage of more than 4500 machines. Every year, around 40 units are added and 15 units are decommissioned, bringing the total number of new units to 25. These 25 additional units are insufficient to meet India's annual population growth rate of 25 Mn people. These factors may deter new entrants into the India Radiotherapy Market.

Competitive Landscape

Key Players

- Varian Medical Systems: Varian is a leading provider of radiotherapy equipment and software solutions. The company has a strong presence in India, with offices in major cities such as Delhi, Mumbai, and Bangalore

- Elekta: Elekta is another leading provider of radiotherapy equipment and software solutions. The company has been operating in India for over two decades and has a strong customer base in the country

- Siemens Healthineers: Siemens Healthineers is a global medical technology company that provides a range of solutions for healthcare providers. The company offers a range of radiotherapy solutions for cancer treatment in India

- Accuray: Accuray is a leading provider of advanced radiation therapy solutions. The company's products include the CyberKnife and TomoTherapy systems, which are used in the treatment of cancer

- Bhabha Atomic Research Centre (BARC): BARC is a research institution that is also involved in the development and deployment of radiotherapy solutions in India. The institution has developed several indigenous radiotherapy systems, including the Bhabhatron

- HCG Group: The HCG Group is a healthcare provider that operates a network of cancer hospitals across India. The company offers a range of radiotherapy solutions, including IMRT, IGRT, and SRS/SRT

- Apollo Hospitals: Apollo Hospitals is a leading healthcare provider in India that offers a range of cancer treatment options, including radiotherapy

Recent Notable Updates

September 2022: Elekta has announced that Karkinos Healthcare, a renowned healthcare provider in India, will purchase more than ten linear accelerators (linac) systems, which will be strategically deployed around the country. The firms share a desire to increase patient access to innovative precision cancer therapies.

Healthcare Policies and Reimbursement Scenarios

The Atomic Energy Regulating Board (AERB), India's primary regulatory agency for radiation safety, oversees radiotherapy. The government also pays for radiotherapy under the National Health Insurance Scheme. Individuals from economically disadvantaged groups receive financial assistance for cancer treatment, including radiotherapy.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

India Radiotherapy Segmentation

By Type (Revenue, USD Billion):

- External Beam Radiation Therapy

- Linear Accelerators

- Compact Advanced Radiotherapy Systems

- Cyberknife

- Gamma Knife

- Tomotherapy

- Proton Therapy

- Cyclotron

- Synchrotron

- Internal Beam Radiation Therapy

- Brachytherapy

- Seeds

- Applicators and Afterloaders

- Electronic Brachytherapy

- Systemic Radiation Therapy

- Others

By Technology (Revenue, USD Billion):

- External Beam Radiotherapy

- Intensity-Modulated Radiation Therapy (IMRT)

- Image-Guided Radiation Therapy (IGRT)

- Stereotactic Radiation Therapy (SRT)

- 3D Conformal Radiation Therapy (3D-CRT)

- Particle Therapy

- Internal Beam Radiotherapy

- Brachytherapy

- High-Dose Rate Brachytherapy

- Low-Dose Rate Brachytherapy

- Image-Guided Brachytherapy

- Pulse-Dose Rate Brachytherapy

- Systemic Radiation Therapy

- Intravenous Radiotherapy

- Oral Radiotherapy

By Application (Revenue, USD Billion):

- Breast Cancer

- Cervical Cancer

- Colon and rectum Cancers

- Stomach Cancer

- Lung Cancer

- Prostate Cancer

- Skin Cancer

- Liver Cancer

- Other types of cancer

By End User (Revenue, USD Billion):

- Hospitals

- Radiotherapy Centers & Ambulatory Surgery Centers

- Cancer Research Institutes

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

South Korea Diabetes Drugs Market Analysis

Pharmaceuticals

India Alzheimer’s Disease Drugs Market Analysis

Pharmaceuticals

Indonesia Unresectable Hepatocellular Carcinoma Market Analysis

Related reports (by geography)

Healthcare Services

India Healthcare Diagnostics Market Analysis

Clinical Trials

India Neurology Clinical Trials Market Analysis

Pharmaceuticals

India Vaccines Market Analysis

Rare Diseases