Pharmaceuticals

India Oncology Therapeutics Market Analysis

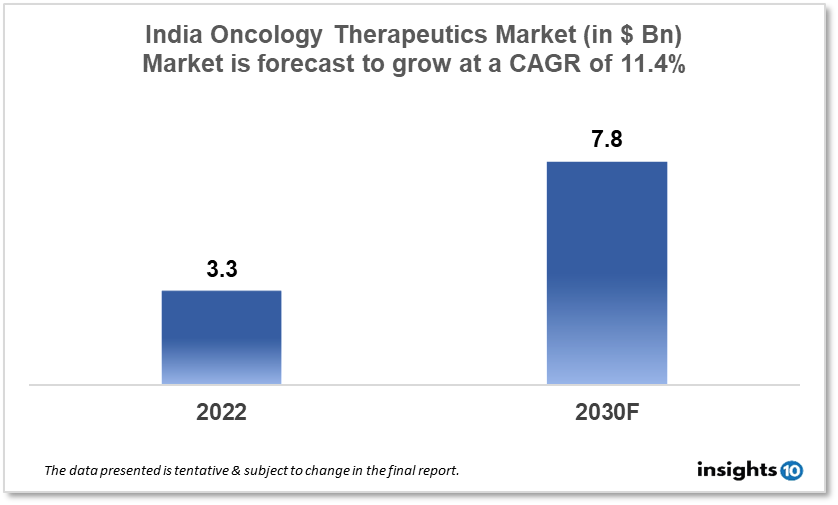

By 2030, it is anticipated that the India Oncology Therapeutics Market will reach a value of $7.8 Bn from $3.3 Bn in 2022, growing at a CAGR of 11.4% during 2022-2030. The Oncology Therapeutics Market in India is dominated by a few domestic pharmaceutical companies such as Cipla, Cadila Medical care, and Dr. Reddy's Research facilities. The Oncology Therapeutics Market in India is segmented into different types of cancer and different therapy type. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for India Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

India Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the India Oncology Therapeutics Market will reach a value of $7.8 Bn from $3.3 Bn in 2022, growing at a CAGR of 11.4% during 2022-2030.

India is a lower middle-income, developing country located in Southern Asia bordering the Arabian Sea and the Bay of Bengal. The public health burden of cancer in India is constantly increasing, with 1.4 Mn new instances of cancer expected in 2020. The estimated number of cancer patients in India was 2.7 Mn (2020). In India, between 60% and 75% of cancer patients are treated in private hospitals, where they face high OOP expenses and troubled finance. By 2025, India's cancer burden is expected to exceed 1.5 Mn cases. The "Health Minister's Cancer Patient Fund (HMCPF)" inside the Rashtriya Arogya Nidhi (RAN) has also been formed to provide financial assistance to cancer sufferers. In metropolitan regions, the average medical expense per hospitalisation case for cancer treatment was 68,259 dollars.

A study by the Parliamentary Standing Committee highlighted concern about the inaccessibility and rising cost of cancer treatment. Cancers of the mouth cavity, stomach, and lungs account for more than 25% of cancer fatalities in men, while cancers of the uterine cervix, breast, and oral cavity account for 25% of cancer deaths in women. India's government spent 3 % of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers

Tobacco products are used by around 28.6 % of the Indian population, accounting for 267 Mn tobacco users in the country. Tobacco use has a significant impact on health in India, notably cancer. To assist suffering patients in affording medical care, the National Pharmaceutical Pricing Authority (NPPA) used exceptional powers in the public interest to start a Pilot on Trade Margin Rationalization for 42 anti-cancer medications. The National Programme for the Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases, and Stroke (NPCDCS) is being implemented at the district level by the National Health Mission (NHM). These aspects could boost India's Oncology Therapeutics Market.

Market Restraints

Treatment in the private sector is too expensive for low- and middle-income patients. The required radiation equipment for a developing country, according to WHO criteria, is 1380, compared to the current 686, which is insufficient to service over half of India's population. India has only 514 radiation facilities, according to the most recent statistics from the Atomic Energy Regulatory Board. Despite having one-fifth of the world's population, India is barely represented in 1.5 % of global clinical trials. The 2018 Ayushman Bharat insurance policy does not cover full prescriptions, the most recent cancer medicines, or numerous diagnostic tests. These factors may deter new entrants into the India Oncology Therapeutics Market.

Competitive Landscape

Key Players

- Biocon: Biocon is an Indian biopharmaceutical organization that creates and delivers a scope of disease therapeutics, including biosimilars, monoclonal antibodies, and little particles. The organization has a few imaginative disease sedates that are as of now in clinical turn of events

- Dr. Reddy's Research facilities: Dr. Reddy's Research facilities is an Indian global drug organization that creates and delivers a scope of malignant growth therapeutics, including chemotherapy drugs, designated treatments, and biosimilars. The organization has a few oncology medicates that are as of now in clinical turn of events

- Cipla: Cipla is an Indian global drug organization that creates a scope of malignant growth therapeutics, including chemotherapy sedates and designated treatments. The organization has a few imaginative oncology medicates that are right now in clinical turn of events

- Cadila Medical care: Cadila Medical care is an Indian drug organization that spotlights the turn of events and creation of a scope of malignant growth therapeutics, including chemotherapy sedates and designated treatments

Notable Recent Deals

January 2023: Sun Pharmaceutical Industries Ltd. said on Wednesday that one of its wholly-owned subsidiaries has released Palbociclib, a breakthrough anti-cancer medicine, in India for patients with advanced breast cancer. Palenotm (Palbociclib) 75 mg, 100 mg, and 125 mg will be offered from the pharmaceutical giant. Sun Pharma is launching Palbociclib at a low cost, which will aid in patient access. Palenotm will provide treatment to a number of advanced breast cancer patients in India.

November 2022: Biocon Biologics, Biocon's biosimilars manufacturing subsidiary, has finalised the acquisition of Viatris. The acquisition is anticipated to increase cancer therapy by giving it full ownership of its cooperation assets, which include the anti-cancer drugs Bevacizumab, Trastuzumab, Pertuzumab, and Pegfilgrastim, which is used to treat low white blood cells.

Healthcare Policies and Reimbursement Scenarios

In India, the administrative power liable for the endorsement and guideline of helpful items, including malignant growth therapeutics, is the Central Drugs Standard Control Organization (CDSCO). In expansion, India has laid out a public health care coverage framework that gives repayment to a scope of clinical costs, including the expense of disease therapeutics. The health care coverage framework is planned to guarantee that all residents approach important clinical considerations, no matter what their capacity to pay. India has carried out an exceptional program called the "National List of Essential Medicine" (NLEM), which is a rundown of meds that are considered fundamental. Also, some lung cancer medications may be made available through specific programmes within the Indian healthcare system, such as the National Health Protection Scheme (Ayushman Bharat).

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

India Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Middle East Orphan Diseases Drugs Market Analysis

Pharmaceuticals

Malaysia Type 2 Diabetes Mellitus Drugs Market Analysis

Related reports (by geography)

Healthcare Services

India Diagnostics Imaging Services Market Analysis

Rare Diseases

India Fabry Disease Therapeutics Market Analysis

Medical Devices

India Hemodialysis Vascular Grafts Market Analysis

Pharmaceuticals