Healthcare Services

India Home Healthcare Market Analysis

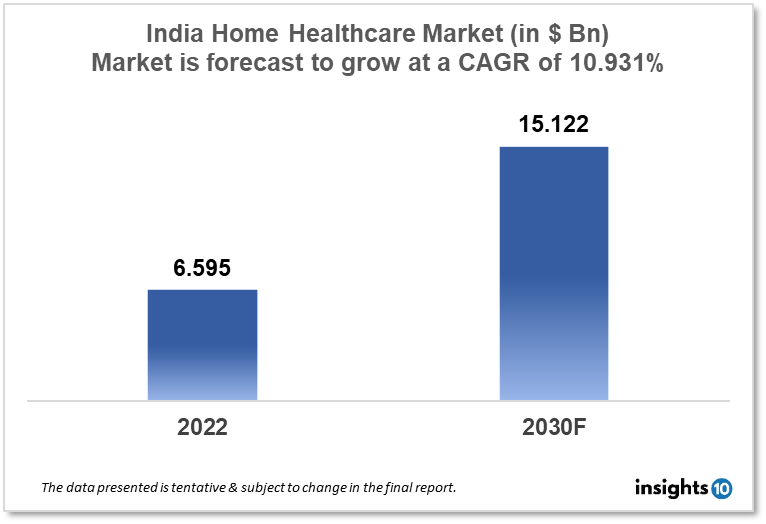

India's home healthcare market was valued at $179 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 6.40% from 2022 to 2030 and will reach $295 Mn in 2030. One of the main reasons propelling the growth of this market is the introduction of newer technologies, The increased prevalence of chronic ailments. The market is segmented by equipment outlook and by services. Some key players in this market are Apollo Homecare, Portea Medical, India Home Health Care, Healthcare at Home, and Care24.

Buy Now

India Home Healthcare Market Executive Summary

India's home healthcare market was valued at $179 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 6.40% from 2022 to 2030 and will reach $295 Mn in 2030. The demand for home healthcare is anticipated to increase as India's geriatric population and dependency ratio both grow. India's ageing population is anticipated to total 298 million by 2051, or 17% of the country's total population, according to the Economic and Social Commission for Asia and the Pacific.

In India, the healthcare industry has grown significantly in both revenue and employment. Hospitals, medical equipment, pharmaceutical products, and services including clinical trials, telemedicine, e-health, health tourism, home healthcare, and health insurance are all included in the definition of healthcare. The extension of services increased coverage, and rising governmental and private investment in the healthcare industry in India have all contributed to the sector's growth.

The home healthcare market in India has a big number of participants and is still in its early stages of development. Some of these players only provide a particular specialty service, while others provide a wide range of services in different geographic areas. 30-35 businesses have experienced rapid expansion in the organized market, and they now have the strongest brand recognition and traction in terms of service sales across several regions. India has multiple home healthcare players providing healthcare across preventive, promotive, chronic, acute rehabilitative, and palliative care in the comfort of the patient’s home. Traditionally, 60–80 percent of demand for home care has been driven by senior citizens seeking supportive long-term care at home.

Market Dynamics

Market Growth Drivers

Technological advancements have made healthcare devices portable, user-friendly, and more convenient for patients at home or traveling. The introduction of newer technologies in this market has greatly boosted the current communication flow between patients and healthcare providers, enabling better, faster, and more effective care. Developments in technology coupled with increasing demand are likely to drive market growth in India. Several companies have ventured into the delivery of medicines, further contributing to the patient-centric advantages of in-home care. Federation of Indian Chambers of Commerce & Industry (FICCI), 54% of people preferred laboratory tests, delivery of medicines, and nursing care at home.

The increased prevalence of chronic ailments such as hypertension, diabetes, arthritis, cancer, and cardiovascular diseases are aiding the growth of the market. Approximately 50% of all home healthcare patients have at least one chronic illness, and this number is expected to keep increasing in the future. Chronic illness is a long-lasting condition that can be controlled but not cured. Treating and managing chronic illnesses has become a major concern.

The need for better primary and postoperative care is likely to drive market growth in the country. Companies are expanding their service offerings to maintain and increase market share. Portea Medical offers geriatric care inclusive of physiotherapy, palliative care, primary care, and postoperative care.

The growth of this population segment will boost the demand for healthcare and greatly increase the burden on governments and health systems as the aging population is more prone to chronic diseases. Home healthcare reduces unnecessary hospital admissions & readmissions and the time and costs involved in traveling to meet healthcare professionals.

Market Restraints

The lack of skilled nursing personnel with a compassionate attitude is anticipated to slow the rate of expansion of the India home healthcare market. A study highlighted that the density of the active health workforce in India is a little over one-fourth of the WHO recommended threshold of 44.5 skilled health workers per 10,000 persons. In home care, the nurse-physician association involves lesser face-to-face contact, and the nurse is responsible for making assessments and communicating findings. In India, home healthcare treatments are covered by insurance only if they are post-hospitalization treatments; in-home treatments for geriatric and chronic ailments are not covered by insurance companies.

Competitive Landscape

Key Players

Due to the existence of numerous local and national companies, the Indian market is very fragmented. Some of the well-known businesses in this sector are Portea Medical, Apollo Homecare, Nightingales Home Health Services, and India Home Health Care (IHHC). In response to an increase in demand, businesses are expanding their operations. For instance, Nightingales Home Health Services has only recently started operating in Chennai. By offering at-home COVID-19 testing, Portea Medical is broadening the scope of its service offerings. In addition, the market's lack of regulation could lead to unfair competition and hostile takeovers.

- Apollo Homecare

- Portea Medical

- India Home Health Care

- Healthcare atHome

- Care24

- Nightingales Home Health Services

- Bharat Home Medicare

- Grand World Elder Care

- Medfind

- Swarg Community Care

- Suburban Diagnostics

Healthcare Policies and Regulatory Landscape

In order to boost home healthcare in India, the Indian government has unveiled new programs. For example, the Healthcare Federation of India produced Home Healthcare 2.0 in January 2022, which included government suggestions and viewpoints from industry stakeholders for generating major growth potential for home healthcare services in India.

The widely popular NABH (National Accreditation Board for Hospitals & Healthcare Providers) has also not framed any healthcare regulatory framework for the private home healthcare segment. The entire market of Home Healthcare is worth above Rs 12,000 crore and so far not even one percent of the market has been captured by all the players combined. The National Health Policy, 2017, which was approved by the Union Cabinet on March 15, envisages the setting up of a National Digital Health Authority (NDHA) to regulate, develop and deploy digital health across the continuum of care.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

India Home Healthcare Market Segmentation

By Equipment

- Therapeutic

- Home Respiratory Therapy

- Insulin Delivery

- Home Intravenous Pumps

- Home Dialysis Equipment

- Other Therapeutic Equipment

- Diagnostic

- Diabetic Care Unit

- Blood Pressure Monitors

- Multi-Parameter Diagnostic Monitors

- Home Pregnancy and Fertility Kits

- Other Self-Monitoring Equipment

- Apnea and Sleep Monitors

- Holter Monitors

- Heart Rate Meters

- Other Diagnostic Equipment

- Mobility Assist Equipment

- Wheelchair

- Home Medical Furniture

- Walking Assist Devices

- By Services

- Skilled Home Care

- Physician/Primary Care

- Nursing Care

- Physical, Occupational, and/or Speech Therapy

- Nutritional Support

- Hospice & Palliative Care

- Other Skilled Home Care Services

- Unskilled Home Care

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Switzerland Women Health Diagnostic Market Analysis

Healthcare Services

Turkey Clinical Diagnostics Market Analysis

Healthcare Services

Denmark Dental Care Market Analysis

Related reports (by geography)

Rare Diseases

India Basal Cell Carcinoma Therapeutics Market Analysis

Pharmaceuticals

India Sleep Disorders Market Analysis

Pharmaceuticals