Pharmaceuticals

India Head and Neck Cancer Therapeutics Market Analysis

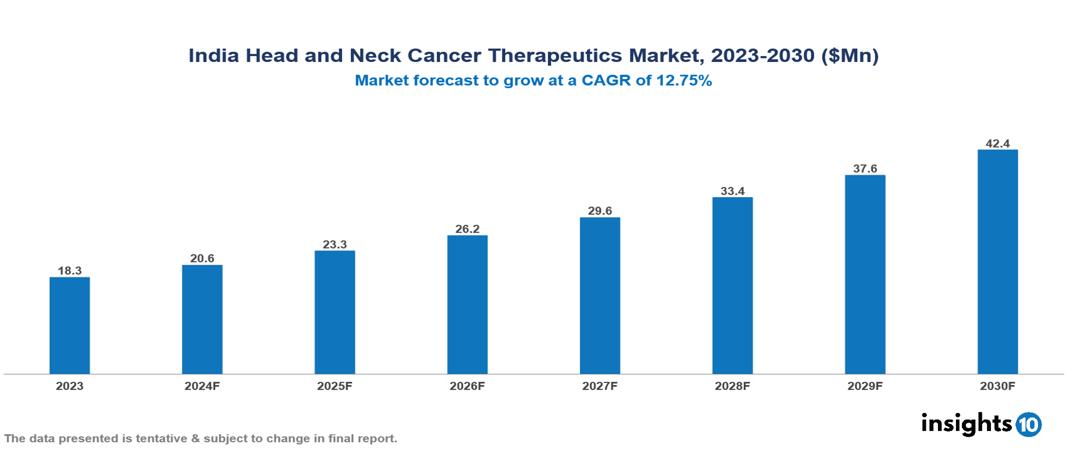

The India Head and Neck Cancer Therapeutics Market was valued at $18.30 Mn in 2023 and is predicted to grow at a CAGR of 12.75% from 2023 to 2030, to $42.39 Mn by 2030. The key drivers of this industry include rising incidence, increasing medical tourism, and advancement in treatment. The industry is primarily dominated by players such as Bristol Myers Squibb, Merck, Roche, and Pfizer among others.

Buy Now

India Head and Neck Cancer Therapeutics Market Executive Summary

The India Head and Neck Cancer Therapeutics Market was valued at $18.30 Mn in 2023 and is predicted to grow at a CAGR of 12.75% from 2023 to 2030, to $42.39 Mn by 2030.

Head and neck cancers can start in the thin lining cells (squamous cells) of the mouth, throat, and voice box, or even in the salivary glands, sinuses, muscles, or nerves in these areas. Smoking, tobacco use, and HPV infection increase the risk, and symptoms like a painful lump in the neck, a sore that won't heal in the mouth or throat, trouble swallowing, or a hoarse voice could be warning signs.

In India, the number of cancer cases is rising. According to GLOBOCAN 2020, there will be 2.1 Mn new cancer cases in India by 2040, an increase of 57.5% from 2020. The all-site cancer incidence rate was 103.7 and 102.4 per 100,000 population for males and females, respectively. The market is driven by significant factors like rising incidence, increasing medical tourism, and advancement in treatment. However, limited access, healthcare disparity, and limited awareness restrict the growth and potential of the market.

Prominent players in this field include Bristol Myers Squibb, Merck, Roche, and Pfizer among others.

Market Dynamics

Market Growth Drivers

Rising Incidence: According to GLOBOCAN 2020, India is projected to see 2.1 Mn new cancer cases by 2040, marking a 57.5% increase from 2020. Head and neck cancers, driven by high rates of tobacco consumption, alcohol use, and HPV infections, are particularly prevalent. The necessity for effective therapeutic choices is essential given the notable increase in cancer incidence. This has led to a surge in demand for advanced head and neck cancer therapeutics in the Indian market.

Increasing Medical Tourism: The projected increase in medical tourists to India, rising from an estimated 6.1 Mn in 2023 to around 7.3 Mn in 2024, significantly drives the head and neck cancer therapeutics market. This rush of foreign patients looking for advanced yet affordable treatments drive up demand for innovative cancer treatments, strengthening India's standing as a major global medical center and promoting expansion in the healthcare industry.

Advancement in Treatment: The accuracy of head and neck cancer diagnoses and the effectiveness of therapy are greatly enhanced by technological advancements in medicine, including precision medicine, molecular diagnostics, and improved imaging techniques. These developments improve patient outcomes by enabling healthcare practitioners in India to provide more individualized and focused therapies. Thus, by improving the standard of care and drawing in patients looking for cutting-edge treatment alternatives, the implementation of such innovative technology serves as a major market driver.

Market Restraints

Limited Access: Access to advanced diagnostic equipment, radiation therapy centers, and oncologists are among the specialized healthcare facilities that are lacking in many sections of India, particularly in rural areas. The provision of comprehensive and timely treatment for patients with head and neck cancer is hindered by this restricted access.

Healthcare Disparity: For many patients in India, access to modern cancer treatments and specialized care is restricted due to differences in healthcare access between urban and rural locations. Because of this access gap, people living in rural areas frequently lack access to prompt, all-encompassing care, which makes it more difficult to diagnose and treat head and neck cancers early on. Consequently, these differences limit the market's potential growth by diminishing the comprehensive scope and influence of therapeutic measures.

Limited awareness: Inadequate awareness of Head and Neck cancer risk factors and symptoms among the general population and medical professionals may result in a delay in diagnosis and treatment initiation. Inadequate early detection screening initiatives may also result in missed opportunities for timely intervention, which could hinder the market's potential to expand and increase demand for head and neck cancer therapies.

Regulatory Landscape and Reimbursement Scenario

The Ministry of Health and Family Welfare (MoHFW) is the central legislative body in charge of framing India's health policies. The Central Drugs Standard Control Organization (CDSCO), under the Ministry of Health and Family Welfare, is India's pharmaceutical regulating authority. It is the national organization in charge of ensuring the efficacy, safety, and quality of medications and cosmetics produced, imported, and distributed in India. On the reimbursement side, a government-sponsored health insurance program called the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) aims to cover low-income families. It covers a defined set of medical procedures, including some cancer treatments. On the other hand, the amount of cancer treatment coverage provided by the various private health insurance policies available can differ greatly.

Competitive Landscape

Key Players

Here are some of the major key players in the India Head and Neck Cancer Therapeutic Market:

- Bristol Myers Squibb

- Merck

- AstraZeneca

- Pfizer

- Eli Lilly and Company

- Novartis

- Roche

- Amgen

- GlaxoSmithKline

- Sanofi

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

India Head and Neck Cancer Therapeutics Market Segmentation

By Treatment

- Targeted Therapy

- Immunotherapy

- Radiation Therapy

- Surgeries

By End Users

- Hospitals

- Specialty Centers

- Ambulatory Surgical Centers

By Distribution Channel

- Hospital-based pharmacies

- Retail pharmacies

- Online pharmacies

By Route of administration

- Injectable

- Oral

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

China Endometriosis Drugs Market Analysis

Pharmaceuticals

US Respiratory Drugs Market Analysis

Pharmaceuticals

UK Cough Hypersensitivity Syndrome Therapeutics Market Analysis

Related reports (by geography)

Medical Devices

India Biosensors Market Analysis

Rare Diseases

India Hyperhidrosis Therapeutics Market Analysis

Pharmaceuticals

India Brugada Syndrome Market Analysis

Healthcare Services