Pharmaceuticals

India Dental Fluoride Treatment Market Analysis

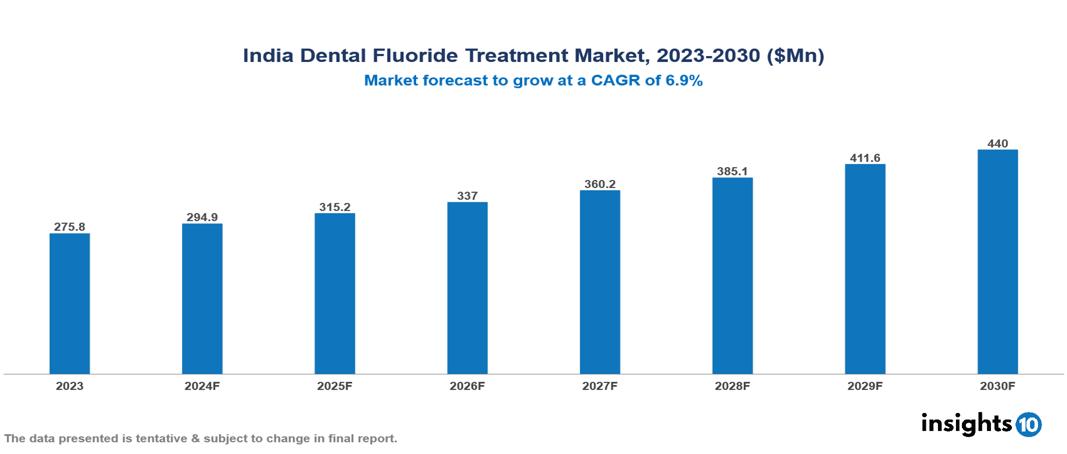

The India Dental Fluoride Treatment Market was valued at $275.8 Mn in 2023 and is projected to grow at a CAGR of 6.9% from 2023 to 2023, to $440 Mn by 2030. The key drivers of this industry are growing prevalence of dental caries coupled with increasing awareness regarding oral health and hygiene, increasing the intake of sugary drinks and food, projected to drive the market. Furthermore, increasing support from the government to improve access to person-cantered treatment and to advance a holistic method of oral health equity has contributed to market growth. The industry is primarily dominated by players such as Colgate, Clove Dental, Himalayas, Dabur and Hindustan Unilever Limited among others.

Buy Now

India Dental Fluoride Treatment Market Executive Summary

The India Dental Fluoride Treatment Market is at around $275.8 Mn in 2023 and is projected to reach $440 Mn in 2030, exhibiting a CAGR of 6.9% during the forecast period 2023-2030.

Dental fluoride treatments are professional applications of high-concentration fluoride products by dentists or hygienists to prevent tooth decay and strengthen enamel. They are typically applied as a gel, foam, varnish or solution during routine visits. Fluoride enhances mineral absorption, integrates into tooth structure, and inhibits cavity-causing bacteria. These treatments provide numerous benefits, including 25% reduced cavity risk, inhibiting cavity growth, delaying dental work, prolonging baby teeth, and preventing gum disease. The ADA recommends treatments every 3-12 months based on cavity risk. Children under 3 should use a small smear of fluoride toothpaste, while those 3-6 can use a pea-sized amount.

Potential side effects include temporary discoloration, irritation, and in rare cases allergic reactions. Excessive intake, especially in young children, can lead to fluorosis. However, dangerous levels are difficult to reach due to low concentrations in over-the-counter products. Acute toxicity from supplements can cause nausea, diarrhea, and even death in severe cases.

According to the National Oral Health Survey 2021, the prevalence of dental caries in India is around 60% among adults and 70% among children. This high burden of dental diseases, with over 300 million Indians affected by dental caries. The market therefore is driven by significant factors like growing prevalence of dental caries coupled with increasing awareness regarding oral health and hygiene, increasing the intake of sugary drinks and food, cosmetic dentistry boom, technological advancements etc.

Some of the major players operating in the market are Colgate, Clove Dental, Himalayas, Dabur and Hindustan Unilever Limited among others.

Market Dynamics

Market Drivers

Rising incidence of dental disorders: According to the National Oral Health Survey 2021, the prevalence of dental caries in India is around 60% among adults and 70% among children. This high burden of dental diseases, with over 300 million Indians affected by dental caries, is driving the demand for effective preventive treatments like fluoride applications.

Increasing awareness about oral health: The Government of India has launched the National Oral Health Programme to raise awareness about oral hygiene, with a target to cover 50% of the population by 2025. As per a survey by the Indian Dental Association, around 80% of Indians are now aware of the importance of oral health, up from 60% in 2018.

Expanding middle-class and rising disposable incomes: India's middle-class population is expected to reach 547 million by 2025, up from 394 million in 2020. The average annual household income in India is projected to grow at a CAGR of 7.5% between 2020 and 2025, enabling more people to afford quality dental care.

Market Restraints

Access to dental care disparities: As per the National Oral Health Survey 2021, only 36% of Indians have access to dental services. There is a significant urban-rural divide, with 70% of dentists practicing in urban areas serving just 28% of the population. This, decrease the growth of dental fluoride treatment market.

Affordability and insurance coverage issues: Dental care, including fluoride treatments, remains unaffordable for a large section of the Indian population, with over 65% of dental expenses being out-of-pocket. Only about 18% of Indians have health insurance that covers dental treatment.

Regulatory and policy challenges: India lacks a comprehensive national policy on oral healthcare, with the Dental Council of India facing challenges in enforcing standards and regulating the growing number of dental colleges and practitioners. Unclear regulations and lack of enforcement can hinder the market's growth and expansion.

Regulatory Landscape and Reimbursement Scenario

India has a well-established regulatory framework for dental consumables, overseen by the Central Drugs Standard Control Organization (CDSCO) under the Ministry of Health and Family Welfare. Dental consumables, classified as medical devices under the Drugs and Cosmetics Act and Medical Devices Rules, require registration and approval from the CDSCO before being marketed in the country. Manufacturers and importers must comply with relevant quality standards and undergo clinical trials or safety evaluations, depending on the risk classification of the consumable.

However, the reimbursement landscape for dental consumables in India is relatively limited. The public healthcare system primarily focuses on preventive and basic dental treatments, with limited coverage for advanced or cosmetic procedures involving specialized consumables. Some private health insurance plans offer dental coverage, but the extent of reimbursement for consumables varies widely among providers. As a result, a significant portion of dental care expenses, including the cost of consumables, is borne by patients through out-of-pocket payments. While corporate dental insurance and government initiatives aim to improve access to dental care, the reimbursement or coverage for dental consumables under these programs is often limited.

Competitive Landscape

Key Players

Here are some of the major key players in the India Dental Fluoride Treatment Market:

- Clove Dental

- Colgate

- Hindustan Unilever Limited

- Dabur

- Patanjali

- Procter & Gamble

- GlaxoSmithKline

- 3M

- Himalaya

- Cure Up Pharma

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

India Dental Fluoride Treatment Market Segmentation

By Type

- Toothpaste

- Gel

- Mouthwash

- Varnish

- Supplements

- Other

By Age Group

- Children

- Adolescents

- Adults

By Application

- Dental Caries

- White Spot Lesions

- Dental Hypersensitivity

- Others

By Distributional Channel

- Dental Clinics

- Hospitals

- Retail Pharmacies & Drug Stores

- Online Sales

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Singapore Progesterone Market Analysis

Pharmaceuticals

Germany SGLT2 Inhibitor Market Analysis

Pharmaceuticals

Ecuador Liver Disease Drugs Market Analysis

Related reports (by geography)

Healthcare Services

India Clinical Trial Biorepository & Archiving Solutions Market Analysis

Medical Devices