Medical Devices

India Cardiac Surgery Instruments Market Analysis

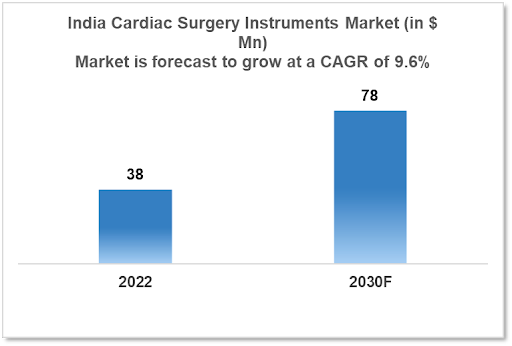

India's Cardiac Surgery Instruments Market is expected to witness growth from $38 Mn in 2022 to $78 Mn in 2030 with a CAGR of 9.60% for the forecasted year 2022-30. India has a significant incidence and prevalence of Cardiovascular Diseases (CVD), including coronary artery disease, heart failure, and hypertension. The demand for cardiac surgery equipment in the Indian healthcare industry is anticipated to rise as CVD prevalence in that country continues to rise. The market is segmented by type, application, and end user. Some key players in this market include Becton Dickinson, GPC Medical, Sahajanand Medical Technologies, LivaNova, B. Braun, Medline Industries, KLS Martin, and STILLE.

Buy Now

India Cardiac Surgery Instruments Healthcare Market Executive Analysis

India's Cardiac Surgery Instruments Market is expected to witness growth from $38 Mn in 2022 to $78 Mn in 2030 with a CAGR of 9.60% for the forecasted year 2022-30.. The staggering $10.75 billion allocated to health costs in India's Union Budget for 2023 represents a rise of $0.28 billion (or 2.71%) from the $10.47 billion allocated in FY23. The Ministry of Health's projected budget for 2022–2023 was originally $10.42 billion but was subsequently lowered to $9.57 billion for the same period. This year, investments total $10.78 billion, according to estimates. In India, spending on healthcare has decreased from 2.2% of the budget to 1.97% this year.

In India, the most prevalent form of heart disease is Coronary Artery Disease (CAD), which is present in over 60 million individuals and is becoming more widespread. Heart failure is a growing public health concern in India, where it affects 1% to 2% of the populace. In India, 1-2% of school-aged toddlers have Rheumatic Heart Disease (RHD), a chronic heart condition brought on by rheumatic fever. To work on the heart and blood vessels, cardiovascular surgeons use specialized equipment referred to as cardiac surgery instruments. For surgeons to effectively perform a range of cardiac surgeries, these tools are crucial. A common cardiac treatment used to improve the blood flow to the heart is called a coronary artery bypass graft (CABG). Using instruments used in heart surgery, such as scissors, forceps, and needle holders, bypass grafts are joined to the coronary arteries during this procedure. A mechanical or biological valve is used during a valve replacement procedure to repair a diseased or damaged heart valve. During this procedure, cardiac surgery instruments like valve retractors, dilators, and sutures are used to remove the old valve and implant the new one.

Market Dynamics

Market Growth Drivers

India has a high rate and prevalence of cardiovascular diseases (CVD), such as coronary artery disease, heart failure, and hypertension. As the prevalence of CVD continues to rise in India, the demand for cardiac surgery tools in the healthcare sector is expected to increase. India is now a top destination for medical tourism due to the large number of patients who travel for treatments, including cardiac surgeries. Due to the growth of the medical tourism industry, healthcare providers in India should experience a rise in demand for cardiac surgery equipment. The Indian government recently increased its spending on healthcare in order to increase citizens' access to high-quality treatment. As a result, more medical centres and hospitals are being built nationally, which broadens the market for businesses that make instruments for cardiac surgery.

Market Restraints

India's market for cardiac surgery instruments is extremely cutthroat, with both local and foreign manufacturers vying for market share. Manufacturers may find it challenging to stand out from competitors and keep their businesses profitable. There is a high demand for reasonably priced healthcare products and services in India, where healthcare providers are frequently price cautious. Because of this, maintaining high-profit margins may be difficult for manufacturers of cardiac surgery instruments.

Competitive Landscape

Key Players

- Becton Dickinson (IN)

- GPC Medical (IN)

- Sahajanand Medical Technologies (IN)

- LivaNova

- B. Braun

- KLS Martin

- Medline Industries

- STILLE

Healthcare Policies and Regulatory Landscape

The manufacture, import, selling, and distribution of medical devices in India are controlled by the Medical Device Rules 2017, which are put into effect by the Central Drugs Standard Control Organization (CDSCO). All medical equipment must comply with the regulations, which also apply to the tools used during cardiac surgery, before being marketed in India. 2017 National Health Policy A policy framework that outlines the government's strategy for healthcare in India is the National Health Policy 2017 (NHP). The policy supports the expansion of the Indian medical device sector and acknowledges the significance of medical devices. A government program called Make in India seeks to promote domestic manufacturing and draw in international capital. The plan includes a number of regulations and rewards aimed at fostering the expansion of the medical device sector, which includes cardiac surgery equipment. A government program called Make in India seeks to promote domestic manufacturing and draw in international capital. The plan consists of a number of regulations and rewards aimed at fostering the development of cardiac surgery equipment. Instruments used in cardiac surgery must meet guidelines established by the Bureau of Indian guidelines. To guarantee the security and calibre of their products, manufacturers are required to adhere to BIS standards.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiac Surgery Instruments Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into segments in this study based on the goods, applications, end users, and geographical areas. The market is divided into forceps, scissors, needle holders, clamps, and other cardiac surgery instruments based on the product. In 2017 the forceps category led the market, and it is anticipated that it will increase at the fastest rate going forward. The rise in heart surgeries and the frequent usage of forceps in most cardiac procedures are credited with the segment's strong growth.

- Forceps

- Vascular Forceps

- Grasping Forceps

- Other Forceps

- Needle Holders

- Scissors

- Clamps

- Other Cardiac Surgical Instruments

By Application (Revenue, USD Billion):

The market is further segmented by application into paediatric cardiac surgery, heart valve surgery, coronary artery bypass graft (CABG), and other applications. The India market's largest and fastest-growing application segment is CABG. This is mostly explained by the increased prevalence of heart illnesses and the consequent rise in surgical treatments. The second-largest category is heart valve surgery.

- Coronary Artery Bypass Graft (CABG)

- Heart Valve Surgery

- Pediatric Cardiac Surgery

- Other Applications

By End User (Revenue, USD Billion):

Based on the end user, the market is segmented into hospitals and cardiac centers, and ambulatory surgery centers. The hospitals and cardiac centers segment is expected to dominate the market for cardiac surgery instruments. Growth in this end-user segment can be attributed to the increasing incidence of cardiac and heart valve diseases and the subsequent increase in the number of cardiac surgery procedures.

- Hospitals and Cardiac Centers

- Ambulatory Surgery Centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Malaysia Hemodialysis Vascular Grafts Market Analysis

Medical Devices

Nigeria Cardiac Surgery Instruments Market Analysis

Medical Devices

Kenya CT Scan Market Analysis

Related reports (by geography)

Rare Diseases

India Hereditary Angioedema Drugs Market Analysis

Pharmaceuticals

India Anti-Aging Drugs Market Analysis

Rare Diseases

India Rare Hemophilia Factors Market Analysis

Pharmaceuticals