Healthcare Services

Global Home Healthcare Market Analysis

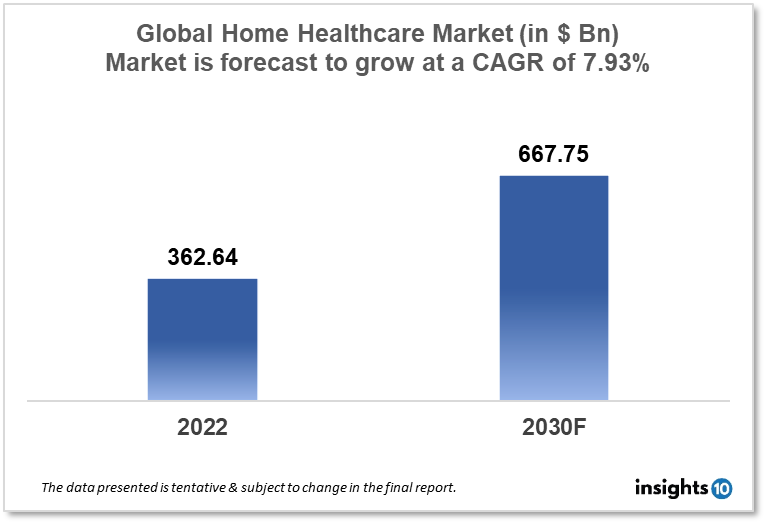

The Global home healthcare market was valued at $362.64 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 7.93% from 2022 to 2030 and will reach $667.75 Bn in 2030. One of the main reasons propelling the growth of this market is the introduction of newer technologies, and the aging population. The market is segmented by component and indication. Some key players in this market are Koninklijke Philips N.V, F. Hoffmann-La Roche AG, A&D Company, Fresenius SE & Co KGaA, Abbott, GE Healthcare, McKesson Corporation, and others

Buy Now

Global Home Healthcare Market Executive Summary

The Global home healthcare market was valued at $362.64 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 7.93% from 2022 to 2030 and will reach $667.75 Bn in 2030. Home healthcare refers to a number of medical services that can be delivered to a patient in the comfort of their own home to treat a sickness or accident. The alternatives for receiving home health care services for a patient are nearly limitless. Depending on the circumstances of the specific patient, care might range from nursing to specialized medical treatments such as laboratory workups. The doctor will establish the treatment strategy and any home treatments that the patient may require. Depending on the patient's health, the duration of home healthcare might range from brief to long.

The doctor may or may not order home healthcare. These services are often covered by insurance companies when ordered by a doctor. Home healthcare also includes gadgets such as blood pressure monitors, glucose monitors, and other therapeutic and diagnostic devices.

Market Dynamics

Market Growth Drivers

Market Growth Drivers

The ageing population, rising rates of target diseases including dementia and Alzheimer's, as well as orthopaedic ailments, are all predicted to fuel market growth. Governments and health organisations are trying very hard to lower healthcare expenses because one of their top concerns is rising treatment costs. The WHO predicts that the percentage of people over 60 in the world will triple, from 12% to 22%, between 2015 and 2050. Each older patient had at least two serious chronic conditions, according to the survey, which fuels the market's expansion. A hospital visit can be less expensively replaced with home healthcare. In addition, people are becoming increasingly aware of the technology and home care options available for such illnesses. The effectiveness of home care for lifestyle diseases has grown thanks to the accessibility of portable devices like blood glucose monitors, breathing machines, and heart rate monitors. Value-based healthcare is a key market contribution as well. The central government offers either partial or full coverage for in-home services in the majority of industrialised and developing nations.

Market Restraints

The home healthcare has a significant need for workers. The top 10 home healthcare jobs include personal care aides and home health aides, according to the US Bureau of Labor Statistics' employment forecasts for the years 2014 through 2024. In addition, 924,000 personal care and home health aides are anticipated to be in need between 2021 and 2031. As a result, in order to fulfil the rising demand, home healthcare agencies must find 924,000 additional clients (source: US Bureau of Labor Statistics). There are difficulties with data privacy and security, as well as the price of technology and its implementation, when it comes to home healthcare services. The home healthcare industry is fragmented, with a large number of small providers and little interprofessional cooperation. Patients may find it challenging to use the system and get the care they require as a result.

Competitive Landscape

Key Players

- Koninklijke Philips N.V.

- F. Hoffmann-La Roche AG

- A&D Company

- Fresenius SE & Co KGaA

- Abbott

- GE Healthcare

- McKesson Corporation

- B. Braun Melsungen AG

- Becton Dickinson Company

- Omron Corporation

- Medtronic PLC

- LG Electronics

- Kinnser Software

- Apple

- 3M

Notable Deals

- Recently Home Care Pulse, one of the leading researches and training firms in the home care market, has acquired Activated Insights and Pinnacle Quality Insight in separate transactions

- Teladoc Health, a virtual healthcare provider, announced its acquisition of Livongo, a digital health company that provides a range of services for chronic conditions, for approximately $18.5 billion. The deal expands Teladoc's reach into the home healthcare market and enhances its ability to offer virtual care services

- Humana Inc. announced the acquisition of practically all of Inclusa, Inc.'s assets on August 12, 2022. Inclusa is a Wisconsin-based managed care organization (MCO) that provides long-term care services to 16,600 older persons and adults with disabilities under Wisconsin's Family Care program

Healthcare Policies and Regulatory Landscape

The Centers for Medicare & Medicaid Services (CMS) in the United States: CMS is a federal agency that administers Medicare, Medicaid, and the Children's Health Insurance Program (CHIP). CMS sets policies and regulations for home healthcare services that are covered by these programs.

The National Health Service (NHS) in the United Kingdom: The NHS is the national healthcare system in the UK and is responsible for setting policies and regulations for home healthcare services. The NHS also provides reimbursement for home healthcare services.

The Ministry of Health in various countries: The Ministry of Health is a government agency that sets policies and regulations for the healthcare sector in many countries. In some countries, the Ministry of Health is responsible for overseeing the home healthcare market.

International regulatory bodies: There are also international regulatory bodies that play a role in the home healthcare market, including the World Health Organization (WHO) and the International Association for Home Care (IAHC). These organizations set standards and provide guidance for home healthcare services and advocate for the rights of patients receiving home healthcare.

Reimbursement Scenario

The reimbursement scenario of the global home healthcare market varies depending on the country, type of care, and the healthcare system. In general, reimbursement for home healthcare services is becoming increasingly common as the demand for these services grows.

In the United States, reimbursement for home healthcare services is primarily provided through Medicare and Medicaid programs, as well as private insurance. Medicare covers a range of home healthcare services for beneficiaries who are eligible, including skilled nursing care, physical therapy, speech therapy, and occupational therapy. Medicaid programs also provide reimbursement for home healthcare services for eligible individuals, including those with low income or disabilities.

In Europe, reimbursement for home healthcare services is provided through national healthcare systems, with some countries offering private insurance options. In the UK, the National Health Service (NHS) provides reimbursement for a range of home healthcare services, including nursing care and rehabilitation.

In many countries, the reimbursement system for home healthcare services is still developing, and coverage can vary greatly. For example, in some countries, reimbursement for home healthcare services is limited to certain types of care, such as palliative care, while in others, it is more comprehensive.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Home Healthcare Market Segmentation

By Device Type (Revenue, USD Billion):

Based on the Device Type the market is segmented into Testing, Screening, Monitoring Devices, Therapeutic Home Healthcare Devices, and Mobility Assist.

- Testing, Screening, and Monitoring Device

- Blood Glucose Monitors

- Blood Glucose Monitors

- Blood Pressure Monitors

- Heart Rate Monitors

- Temperature Monitors

- Sleep Apnea Monitors

- Coagulation Monitors

- Ovulation and Pregnancy Test Kits

- Pulse Oximeters

- Home Hemoglobin A1C Test Kit

- Therapeutic Home Healthcare Devices

- Oxygen Delivery Systems

- Nebulizers

- Ventilators

- Sleep Apnea Therapeutic Devices

- Wound Care Products

- IV Equipment

- Dialysis Equipment

- Insulin Delivery Devices

- Inhalers

- ?Other Therapeutic Products (ostomy devices, automated external defibrillators (AEDs)

- Mobility Assist

- Walkers and Rollators

- Wheelchairs

- Canes

- Crutches

- Mobility Scooters

By Service Type (Revenue, USD Billion):

- Skilled Nursing Services

- Rehabilitation Therapy Services

- Hospice and Palliative Care Services

- Unskilled Care Services

- Respiratory Therapy Services

- Infusion Therapy Services

- Pregnancy Care Services?

By Indication Type (Revenue, USD Billion):

- Cardiovascular Disorders & Hypertension

- Diabetes

- Respiratory Diseases

- Pregnancy

- Mobility Disorders

- Hearing Disorders

- Cancer

- Wound Care

- Other Indications (sleep disorders, kidney disorders, neurovascular diseases, and HIV)

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Switzerland Robotic Surgery Services Market Analysis

Healthcare Services

US Dermatology Diagnostic Market Analysis

Healthcare Services

China Gene Editing Market Analysis

Related reports (by geography)

Digital Health

Global Digital Medical Simulation Market for Cadavers

Medical Devices

Global Neurology Devices Market Analysis

Pharmaceuticals

Global Alexipharmic Drugs Market Analysis

Pharmaceuticals