Healthcare Services

Global Cancer Pain Management Market Analysis

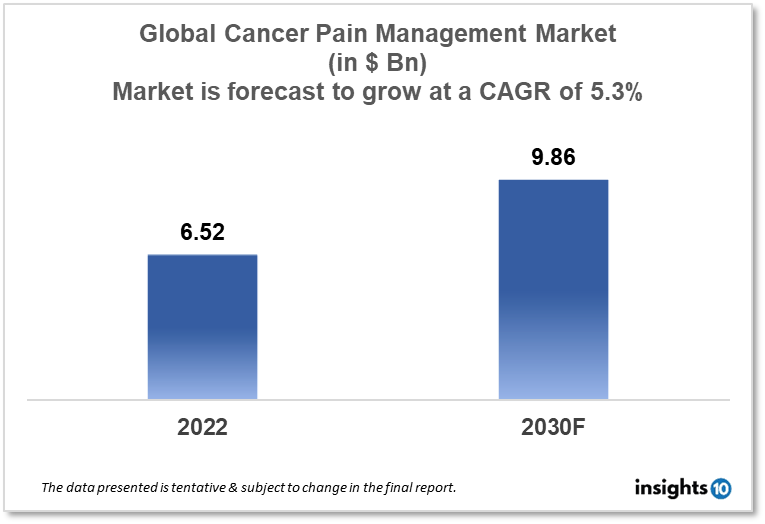

The global Cancer Pain Management market is projected to grow from $6.52 Bn in 2022 to $9.86 Bn by 2030, registering a CAGR of 5.3% during the forecast period of 2022-2030. The main factors driving the growth would be the aging population, rising cancer prevalence, rising healthcare costs, and rising R&D spending by various healthcare businesses. The market is segmented by drug type and by disease. Some of the major players include Aoxing Pharmaceutical, Pfizer, Grunenthal Pharma, Teva Pharmaceutical, Hisamitsu Pharmaceutical, Sanofi, Daiichi Sankyo, Orexo, WEX Pharmaceuticals, and Sorrento Therapeutics.

Buy Now

Global Cancer Pain Management Market Executive Summary

The global Cancer Pain Management market is projected to grow from $6.52 Bn in 2022 to $9.86 Bn by 2030, registering a CAGR of 5.3% during the forecast period of 2022 - 2030. Globally, national healthcare spending as a percentage of GDP amounted to $9.83% in 2021 or $1,115.01 per person.

Many well-known illnesses of acute and chronic pain are related to cancer. Gene alterations brought on by cancer affect essential cell-regulatory proteins. These changes encourage abnormal cell behavior, which then fuels unchecked cell proliferation and the ensuing obliteration of nearby healthy tissues. By pressing on bones, nerves, and other body parts, these tumors put pressure on the body and cause pain. Cancer discomfort can also be felt while undergoing severe cancer therapy, particularly in more advanced stages of the disease.

In 2020, North America accounted for a sizable portion of the global market for cancer pain, and it is anticipated that it will continue to dominate the market throughout the forecast period due to the region's rising cancer prevalence, technological improvements in the healthcare industry, easy access to pain medications, and availability of top-tier chemotherapy treatment choices. However, due to the rapid rise in cancer prevalence, rise in the geriatric population, and increased awareness of early cancer screening, Asia-Pacific and Africa are predicted to post the greatest CAGR during the forecasting period.

Market Dynamics

Market Growth Drivers

The aging population, rising cancer prevalence, rising healthcare costs, and rising R&D spending by various healthcare businesses are all contributing reasons to the growth of the global market for cancer pain management. The American Cancer Society estimated around 1.8 million new cancer cases were diagnosed and 606,520 cancer deaths in the United States in 2020. Due to the aging process and gene mutations, the elderly are more susceptible to developing a number of malignancies, including lung, bladder, kidney, and melanoma.

Market Restraints

During the forecast period, the growth of the cancer pain market is anticipated to be constrained by undesirable effects associated with the usage of medications used to treat cancer pain, such as drug tolerance, drug dependence, urine retention, sleep disorders, cognitive impairment, nausea, and others.

Competitive Landscape

Key Players

- Aoxing Pharmaceutical

- Pfizer

- Grunenthal Pharma

- Teva Pharmaceutical

- Hisamitsu Pharmaceutical

- Sanofi

- Daiichi Sankyo

- Orexo

- WEX Pharmaceuticals

- Sorrento Therapeutics

Notable Recent Deals

June 2021: Sorrento Therapeutics acquired ACEA Therapeutics. The previously licensed anchoring small molecule drug Abivertinib, which is used to treat a number of malignancies and autoimmune illnesses, will be added to the list of NCE therapeutic product candidates with this acquisition.

December 2021: A licensing deal for a brand-new sodium channel blocker was signed by Hisamitsu Pharmaceutical and RaQualia Pharma. Hisamitsu Pharmaceutical, which specializes in producing transdermal medications, will conduct preclinical research on new pain treatment drugs incorporating the chemical before moving to the clinical stage. According to the licensing deal, Hisamitsu Pharmaceutical will be given exclusive worldwide rights to develop, produce, and commercialize the chemical.

Healthcare Policies and Regulatory Landscape

A complex regulatory environment that is shaped by many healthcare policies and regulations affects the global market for cancer pain management. These regulations have an effect on both patient access to these medicines as well as the approval, marketing, and distribution of medications used to treat cancer pain. National and international regulatory organizations, such as the World Health Organization, the European Medicines Agency, and the U.S. Food and Drug Administration, have an impact on the regulatory environment. The World Federation of Societies of Anaesthesiologists (WFSA) and the International Association for the Study of Pain (IASP), two healthcare organizations and professional organizations, also contribute to the development of the regulatory environment. Setting standards and criteria for the cancer pain management industry is also a responsibility of government healthcare organizations like the National Institutes of Health (NIH) in the United States and the National Health Service (NHS) in the United Kingdom.

Reimbursement Scenario

The cancer pain management market's global reimbursement scenario is complicated and differs across nations and regions. Cancer pain management medications and therapies are reimbursed by government-funded healthcare systems in many nations, but private insurance or out-of-pocket costs are more typical in others. There might be a broad range in both the amount of reimbursement offered and the particular requirements for reimbursement. The availability of alternative treatments, the cost-effectiveness of different medications, and the perceived benefits and hazards of various treatments are all factors that affect the reimbursement picture for cancer pain management. The reimbursement situation may also be affected by the regulatory environment for the market for cancer pain treatment as well as by the laws and regulations governing healthcare funding and reimbursement.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Global Cancer Pain Management Market Segmentation

By Drug Type (Revenue, USD Billion):

Non-steroidal anti-inflammatory medicines relieve pain at the site of injury by blocking the cyclooxygenase enzyme, which prevents prostaglandin formation. NSAIDs are a class of medications that includes medications with analgesic, antipyretic, and, at higher doses, anti-inflammatory properties.

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

Based on disease Indication the market is segmented into:

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

By Geography

APAC Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Europe Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

North America Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Middle East Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Africa Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Latin America Cancer Pain Management Market

By Drug Type (Revenue, USD Billion):

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Algeria Bioinformatics Market Analysis

Healthcare Services

Morocco Clinical Diagnostics Market Analysis

Healthcare Services

France Connected Healthcare Market Analysis

Related reports (by geography)

Medical Devices

Global Coronary Stents Market Analysis

Clinical Trials

Global Growth Hormone Deficiency Clinical Trials Market Analysis

Medical Devices

Global Cardiac Monitoring Devices Market Analysis

Pharmaceuticals