Germany Teleradiology Market Analysis

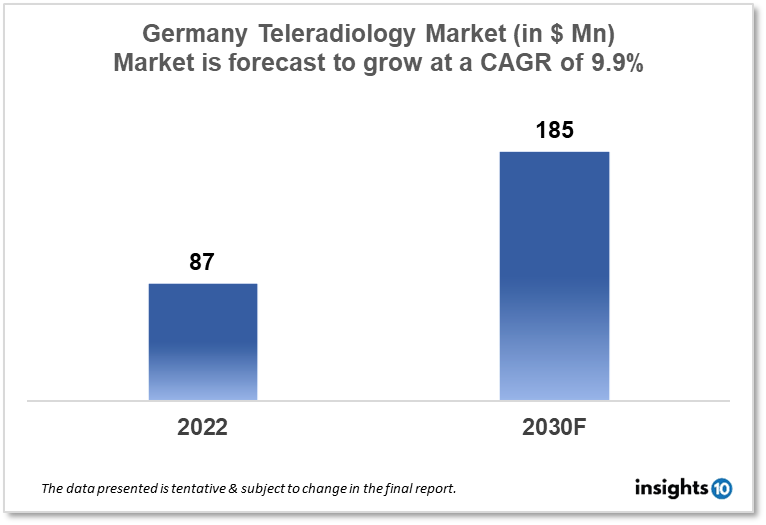

The Germany Teleradiology market size was valued at $87 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 9.9% from 2022 to 2030 and will reach $ 185 Mn in 2030. The market is segmented by application, modality, technology solutions, and end user. The Germany teleradiology market will grow due to Increasing demand for remote radiology services. The key market players are Radiology Consultants Associated (RCA), NightHawk Radiology Services, Calgary Scientific, and others.

Buy Now

Germany Teleradiology Market Executive Summary

The Germany Teleradiology market size was valued at $87 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 9.9% from 2022 to 2030 and will reach $ 185 Mn in 2030. According to recent estimates, total healthcare spending in Germany was approximately 350 Bn euros in 2020. This represents a significant portion of the country's gross domestic product (GDP), and reflects the high value that German citizens place on their health and well-being.

Teleradiology has become an important component of healthcare delivery in Germany, particularly in rural areas where access to radiology services may be limited. Teleradiology enables remote access to radiology services, allowing patients to receive timely and accurate diagnoses and treatment recommendations. It also enables healthcare providers to consult with radiology experts who may be located in other parts of the country or even in other countries.

Artificial intelligence is one of the most promising breakthroughs in the field of teleradiology. In the past 10 years, it is estimated that the number of publications on AI in radiology increased from an average of 100–150 research publications per year to 700–800 per year. Of all the major imaging modalities, the adoption of AI is higher in CT and MRI systems; likewise, based on applications, AI is heavily used in neuroradiology. Several players in this market have increased their offerings in the field of AI. AI can assist in the development of an in-built system that prioritizes cases based on protocol requirements. For example, cases of trauma and stroke can be prioritized and assigned to the radiologist’s work lists, thereby saving many lives.

Teleradiology has become an increasingly important part of the healthcare system in Germany, helping to improve access to radiology services and ensure that patients receive timely and accurate diagnoses and treatment recommendations. Hence, the demand for teleradiology will increase during the forecast period.

Market Dynamics

Market Growth Drivers

- Advancements in technology: Remote transmission and radiological picture interpretation are now simpler and more effective thanks to modern technologies and software. This has caused German healthcare practitioners to use teleradiology services more frequently.

- Increasing demand for remote radiology services: In isolated and rural locations where access to radiologists may be limited, there has been an increase in demand for remote radiological services. No matter where they are, patients can receive rapid and precise diagnoses because to teleradiology.

- Cost-effectiveness: Since teleradiology eliminates the need for on-site radiologists and shortens patient wait times, it can be a financially viable solution for healthcare providers.

- Growing healthcare industry: Germany's healthcare sector is expanding as a result of an ageing population and rising demand for medical services. This is anticipated to fuel market expansion for teleradiology as well.

Market Restraints:

- Concerns about data privacy and security: Sensitive patient data is transmitted and stored during teleradiology, which might lead to questions about data security and privacy. In order to protect patient information, providers must take precautions, which might raise the price and complexity of teleradiology services.

- Technical challenges: To send images and data, teleradiology needs dependable, fast internet connections, which can be difficult in remote and rural regions. Technical problems with hardware or software can also impede the teleradiology procedure and degrade the standard of patient care.

- Lack of standardization: Healthcare providers may find it challenging to compare and assess various teleradiology services due to the lack of established standards and norms, which may have an impact on market acceptance and growth.

Competitive Landscape

Key Players

Teleradiology companies in Germany provide a range of services, including radiology reporting, image transmission, and image analysis. Some of the leading teleradiology companies in Germany include:

- Medneo: Medneo is a leading provider of teleradiology services in Germany, offering radiology reporting and image transmission services to healthcare providers across the country.

- Telepaxx Medical Data GmbH: Telepaxx is a teleradiology company that provides cloud-based image transmission and storage services to healthcare providers in Germany and other countries.

- RIS Healthcare: RIS Healthcare is a teleradiology company that provides radiology reporting and image analysis services to healthcare providers in Germany and other countries.

- RadiologyExperts: RadiologyExperts is a teleradiology company that provides radiology reporting and image analysis services to healthcare providers in Germany and other countries.

Healthcare Policies and Regulatory Landscape

In Germany, teleradiology is subject to several regulatory frameworks to ensure the safety and quality of patient care. Some of the regulations that apply to teleradiology in Germany include:

Medical Devices Act (MPG): The MPG regulates the safety and performance of medical devices, including radiology equipment used for teleradiology. The act requires that medical devices meet certain safety and performance standards and be registered with the appropriate authorities before they can be used in clinical practice.

Radiology Act (RöV): The RöV regulates the use of radiation in medical imaging and sets standards for radiation protection. The act requires that radiology equipment be regularly inspected and calibrated to ensure that it is functioning properly and that radiation exposure to patients and healthcare providers is kept to a minimum.

Data Protection Act (DSGVO): The DSGVO regulates the processing of personal data, including medical images used in teleradiology. The act requires that patient data be treated confidentially and that appropriate measures be taken to protect patient privacy and data security.

Medical Association Guidelines: The German Medical Association has issued guidelines for teleradiology that provide recommendations for the use of teleradiology services, including the qualifications of radiologists and technical requirements for equipment and image transmission.

These regulations aim to ensure that teleradiology services in Germany are safe, effective, and meet high standards of quality and patient care. It is important for healthcare providers and teleradiology companies to comply with these regulations to ensure that patients receive the best possible care.

1. Executive Summary

1.1 Digital Health Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Digital Health Policy in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Teleradiology Market Segmentation

By Application

- Picture Archiving and Communication System (PACS)

- Radiology Information System (RIS)

By Modality:

The market is divided into X-ray, computed tomography (CT), ultrasound, magnetic resonance imaging (MRI), nuclear imaging, fluoroscopy, and mammography segments based on Modality. The computed tomography market category held the biggest market share in 2020. Several medical specialties employ computed tomography, including cardiology, cancer, neurology, abdominal and pelvic imaging, as well as spine and musculoskeletal imaging. The teleradiology market is expanding in this sector due to factors including the rising demand for early and accurate diagnosis, technical improvements, and digitalization in this industry. Around 100 million CT scans are performed annually worldwide, according to the WHO. The demand for CT scans over other imaging modalities has increased due to the desire to avoid exploratory procedures and advancements in cancer diagnosis and therapy.

- X-Ray

- Magnetic Resonance Imaging

- Computed Tomography

- Ultrasound Systems

- Nuclear Imaging

By Technology Solutions

- Web-Based Teleradiology Solutions

- Cloud-Based Teleradiology Solutions

By End User

The market is divided into four categories based on the end users: long-term care facilities, nursing homes, and assisted living facilities; hospitals and clinics; diagnostic imaging centres and laboratories; and other end users. In 2019, the hospitals and clinics segment's revenue contribution was the highest. This segment's significant market share can be ascribed to the increase in diagnostic imaging operations carried out in hospitals, the hospitals' growing propensity to automate and digitise patient data, and the growing demand to raise the standard of patient care. In addition, the COVID-19 pandemic shortage of radiologists and the growing usage of new imaging modalities to boost hospital workflow efficiency are anticipated to enhance the development of this end-user segment.

- Hospitals and Clinics

- Diagnostic Imaging Center and Laboratories

- Long-term Care Centres, Nursing Homes, Assisted Living Facilities

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Japan Digital Biomarkers Market Analysis

Malaysia Blockchain Technology in Healthcare Market Analysis

Related reports (by geography)

Germany Rare Hemophilia Factors Market Analysis

Germany Atherosclerosis Drugs Market Analysis

Germany Fragile-X Syndrome Therapeutics Market Analysis