Pharmaceuticals

Germany Oral Care Market Analysis

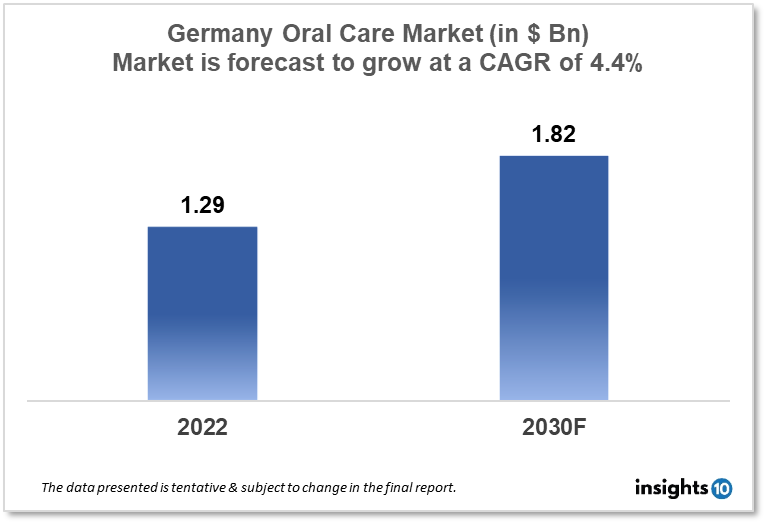

Germany's oral care market was valued at $1.29 Bn in 2022 and is estimated to expand at a CAGR of 4.4% from 2022 to 2030 and will reach $1.82 Bn in 2030. One of the main reasons propelling the growth of this market is the introduction of newer technologies, Increasing prevalence of dental diseases. The market is segmented by type, drug, and distribution channel. Some key players in this market are Elmex, Meridol, Dr. Best, Dontodent, blend-a-dent Biorepair, Odol-med3, Listerine, and Kukident.

Buy Now

Germany Oral Care Market Executive Summary

Germany's oral care market was valued at $1.29 Bn in 2022 and is estimated to expand at a CAGR of 4.4% from 2022 to 2030 and will reach $1.82 Bn in 2030. The oral care market in Germany is a significant and growing sector within the country's healthcare industry. Oral care includes a broad range of products and services, including dental services, oral hygiene products, and orthodontic products.

The dental services sector in Germany is highly developed and well-regulated. There are approximately 80,000 licensed dentists in Germany, and dental care is covered by both public and private health insurance plans. The country's public health insurance system covers basic dental care, including regular check-ups, fillings, and tooth extractions. However, more advanced procedures, such as orthodontics, may not be covered or may only be partially covered. Private health insurance plans typically provide more comprehensive coverage for dental care, including orthodontic treatment.

Market Dynamics

Market Growth Drivers

There is a growing trend in Germany towards cosmetic dentistry, which includes procedures such as teeth whitening, veneers, and dental implants. This is being driven by factors such as increasing disposable income, a desire for better oral aesthetics, and the influence of social media. The cosmetic dentistry market in Germany is expected to grow at a CAGR of 6.6% from 2020 to 2027. Dental diseases, such as cavities, gum disease, and oral cancer, are becoming increasingly common in Germany. This is due to factors such as an aging population, changing dietary habits, and poor oral hygiene. As a result, there is a growing demand for dental services and oral care products. The dental equipment and consumables market in Germany is expected to reach USD 3.3 billion by 2025, growing at a CAGR of 5.9% from 2019 to 2025. Technological advancements in dental care, such as digital dentistry, 3D printing, and CAD/CAM systems, are driving growth in the oral care market in Germany. These advancements are leading to more precise and efficient dental procedures, which are often less invasive and more comfortable for patients. There is a growing awareness of the importance of oral health in Germany, which is driving demand for oral care products and services. This is being fueled by factors such as government initiatives to promote oral health, increasing education about the link between oral health and overall health, and the influence of social media. According to a report, the oral care market in Germany is expected to reach $3.1 Bn by 2026, growing at a CAGR of 4.4% from 2020 to 2026.

Market Restraints

There is a lack of standardization in the way that data is collected and reported in the oral care market in Germany. This makes it difficult to compare data across different products and services, as well as different regions within the country. There is limited access to data on the oral care market in Germany, particularly for smaller companies and new entrants. This can make it difficult for these companies to make informed decisions about product development and marketing. There is a lack of consumer data on oral care habits and preferences in Germany. This can make it difficult for companies to develop products that meet the specific needs and preferences of German consumers. Germany has strict data protection laws, which can make it difficult for companies to collect and analyze data on consumers. This can limit the amount of data available for analysis and may make it difficult for companies to develop targeted marketing campaigns. German is the primary language spoken in Germany, which can create language barriers for companies looking to collect and analyze data in the country. This can limit the amount of data available to companies, particularly those that do not have a strong presence in the country.

Competitive Landscape

Key Players

- Elmex

- Meridol

- Dr. Best

- Dontodent

- Blend-a-dent

- Biorepair

- Odol-med3

- Listerine

- Kukident

Healthcare Policies and Regulatory Landscape

The healthcare policy and regulatory framework of the oral care market in Germany is overseen by several government bodies, including the Federal Ministry of Health, the Federal Institute for Drugs and Medical Devices (BfArM), and the Federal Joint Committee (G-BA). The German healthcare system is based on statutory health insurance (SHI), which covers around 85% of the population. SHI is funded by contributions from employers and employees and covers a range of services, including dental care. Private health insurance (PHI) is also available, primarily for individuals with higher incomes.

In terms of regulation, dental products, and devices are subject to the European Union's Medical Device Regulation (MDR) and In-vitro Diagnostic Medical Device Regulation (IVDR). The BfArM is responsible for overseeing the approval and monitoring of medical devices, including dental products and devices. The G-BA is responsible for making decisions about which medical services and products will be covered by SHI. In 2019, the G-BA announced that it would expand coverage of preventive dental care services for children and adolescents, including fluoride varnish treatments and dental sealants.

In addition to these bodies, there are also several professional organizations and associations that play a role in shaping the healthcare policy and regulatory framework of the oral care market in Germany. These include the German Dental Association (BZÄK), the Association of Statutory Health Insurance Dentists (KZBV), and the German Society of Dental, Oral, and Craniomandibular Sciences (DGZMK).

Reimbursement Scenario

In Germany, dental care is covered by both statutory health insurance (SHI) and private health insurance (PHI) plans. The reimbursement scenario for dental care services and products can vary depending on the type of insurance plan. Under SHI, basic dental care services are covered, including check-ups, fillings, and extractions. However, more advanced dental procedures, such as implants and orthodontic treatment, may require additional out-of-pocket payments. Some dental products, such as dental prosthetics, are also covered by SHI.

Private health insurance plans typically offer more extensive coverage for dental care services and products, including advanced procedures like implants and orthodontics. However, the exact coverage and reimbursement rates can vary depending on the specific plan. In addition to SHI and PHI, there are also several supplementary insurance policies available for dental care coverage in Germany. These policies can provide additional coverage for more extensive dental procedures and products, as well as a higher reimbursement rate.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Germany Oral Care Market Segmentation

By Product Type (Revenue, USD Billion):

- Toothpaste

- Toothbrush

- Mouthwash

- Dental Accessories

- Denture Products

- Others

By Distribution Channel (Revenue, USD Billion):

- Retail Pharmacies

- Online Channels

- Supermarkets

- Dental Dispensaries

By Demographics

- Age (children, adults, and geriatric population)

- Gender

- Income

- Education

- Occupation

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Canada Retail Pharmacy Market Analysis

Pharmaceuticals

South Africa Type 2 Diabetes Mellitus Drugs Market Analysis

Pharmaceuticals

Latin America Sleep Disorders Market Analysis

Related reports (by geography)

Pharmaceuticals

Germany Antithrombotic Drugs Market Analysis

Healthcare Services

Germany Prenatal Testing & Newborn Screening Market Analysis

Pharmaceuticals

Germany Interferons Market Analysis

Healthcare Services