Healthcare Services

Germany Medication Access Programs Market Analysis

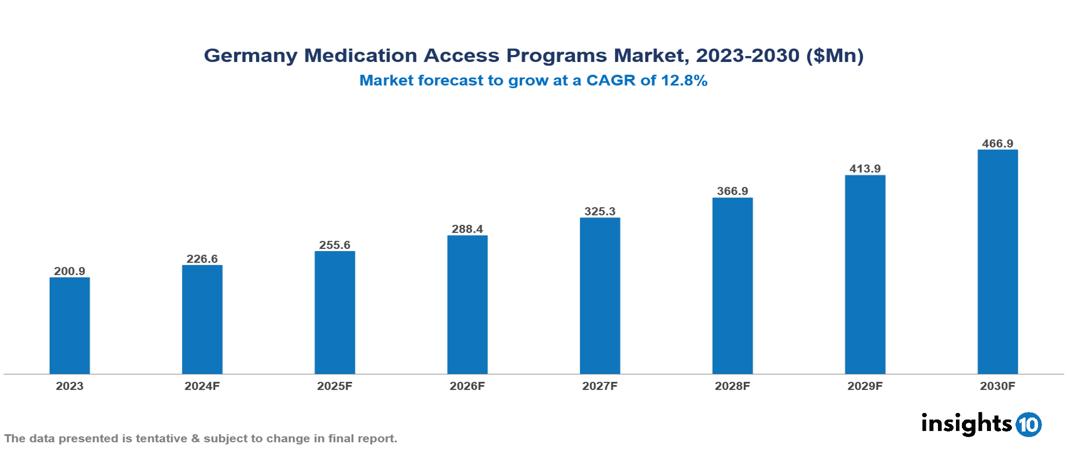

The Germany Medication Access Programs Market was valued at $200.9 Mn in 2023 and is predicted to grow at a CAGR of 12.8% from 2023 to 2030, to $466.9 Mn by 2030. The key drivers of this industry include healthcare expenditure, the aging population, and pharmaceutical support. The industry is primarily dominated by players such as Gilead Sciences, Takeda Pharmaceuticals, Pfizer, and Novartis among others.

Buy Now

Germany Medication Access Programs Market Executive Summary

The Germany Medication Access Programs Market was valued at $200.9 Mn in 2023 and is predicted to grow at a CAGR of 12.8% from 2023 to 2030, to $466.9 Mn by 2030.

Patient Support Programs (PSPs) are initiatives organized by pharmaceutical companies to enhance access, usage, and adherence to prescription drugs. These programs encompass financial assistance, clinical support, educational efforts, or a blend of these elements. A Medication Access Program (MAP) is a part of PSP which is a crucial connection between patients and their needed medications. Managed Access Programs are initiatives that enable patients with serious or life-threatening illnesses to obtain investigational medicines or treatments not yet commercially available. These programs aim to provide early access to therapies for patients who have exhausted all other options and are ineligible for clinical trials. Offered by pharmaceutical companies, MAPs help patients overcome financial barriers to access essential medications. A centralized, pharmacy-driven MAP can enhance patient outcomes, reduce unnecessary healthcare costs, improve patient and provider satisfaction, streamline patient flow, and boost revenue through increased prescription capture.

As of 2022, Germany has 18,068 community pharmacies supplying pharmaceuticals to the population, with these pharmacies handling 1 Bn patient interactions annually and serving 3 Mn patients daily. A significant 88% of patients who regularly take three or more medications consistently visit the same pharmacy. The market is driven by significant factors like healthcare expenditure, aging population, and pharmaceutical support. However, lack of awareness, distribution challenges, and administrative burdens restrict the growth and potential of the market.

Prominent players in this field include Gilead Sciences and Takeda Pharmaceuticals which provide Medication Access or Access to Medicine Program. Pfizer, Novartis, Merck, and AstraZeneca among others are some of the pharmaceutical companies providing patient support programs and are potential players for the Medication Access Program in Germany.

Market Dynamics

Market Growth Drivers

Healthcare Expenditure: In 2021, Germany allocated 12.9% of its gross domestic product (GDP) to healthcare, the largest proportion among the 27 European Union Member States. This substantial investment in healthcare serves as a key market driver for medication access programs in Germany. High healthcare expenditure reflects the government's commitment to ensuring comprehensive medical services, which includes the development and support of programs that enhance patient access to medications.

Aging Population: Germany's population aged 65 and older is projected to rise by 41%, reaching 24 Mn by 2050, which will constitute about one-third of the total population. This significant demographic shift is a crucial market driver for medication access programs, as an aging population typically has higher healthcare needs and requires more medications for chronic conditions and age-related diseases.

Pharmaceutical Support: Pharmaceutical companies are increasingly offering Medication Access Programs (MAPs) to boost medication adherence, enhance patient outcomes, and cultivate brand loyalty. This trend is a significant market driver for medication access programs in Germany, as it not only helps patients manage their treatment plans more effectively but also strengthens the relationship between patients and pharmaceutical brands, leading to better overall healthcare and sustained market growth.

Market Restraints

Lack of Awareness: Patients and healthcare providers might not be fully informed about the available medication access programs, resulting in their underutilization. This lack of awareness serves as a significant market restraint for the medication access program market in Germany, as it prevents these programs from reaching their full potential and assisting the maximum number of patients who could benefit from them.

Distribution Challenges: Efficiently distributing medications through access programs can be logistically difficult, particularly in rural or underserved areas. This logistical challenge is a significant market restraint for the medication access program market in Germany, as it can hinder the consistent and timely delivery of essential medications to all patients, thereby limiting the effectiveness and reach of these programs.

Administrative Burden: The administrative tasks involved in overseeing medication access programs can impose significant burdens on both healthcare providers and pharmaceutical companies. This administrative complexity acts as a notable restraint in the medication access program market in Germany, potentially diverting resources away from patient care and program expansion efforts, thus impacting overall efficiency and effectiveness.

Regulatory Landscape and Reimbursement Scenario

Under the authority of the Federal Ministry of Health, the Federal Institute for Drugs and Medical Devices (BfArM) operates as an independent federal agency. Its responsibilities include issuing licenses, enhancing drug safety, and assessing risks related to medical devices. Introduced in 2010 under the German Medicinal Product Act (AMG), Compassionate Use programs are governed by the Ordinance on Medicinal Products for Compassionate Use (AMHV). These programs enable patients with serious or life-threatening conditions, who cannot be adequately treated with approved drugs, to access unapproved medications. The AMHV established a notification process where companies must inform the BfArM or the Paul Ehrlich Institute before initiating a new Compassionate Use program, which is subsequently confirmed by these authorities.

Germany operates under a compulsory health insurance system, encompassing both statutory (gesetzliche Krankenversicherung, or GKV) and private (Private Krankenversicherung, or PKV) health insurers. Statutory health insurance funds cover the majority of the population and contribute significantly to healthcare spending.

Competitive Landscape

Key Players

Here are some of the major key players in the Germany Medication Access Programs Market:

- Gilead Sciences

- Takeda Pharmaceuticals

- Pfizer

- Novartis

- Merck

- AstraZeneca

- Bristol-Myers Squibb

- Sanofi

- Eli Lilly

- AbbVie

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Germany Medication Access Programs Market Segmentation

By Disease Type

- Chronic

- Acute

By Therapeutic Areas

- Oncology

- Cardiology

- Rheumatology

- Others

By Patient Type

- Geriatric

- Pediatric

- Adult

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Hong Kong Patient Support Programs (PSP) Market Analysis

Healthcare Services

Spain Oxygen Flow Meters Market Analysis

Healthcare Services

Singapore In Vitro Fertilisation (IVF) Service Market Analysis

Related reports (by geography)

Healthcare Services

Germany Healthcare Insurance Market Analysis

Pharmaceuticals

Germany Cartilage Repair/Regeneration Market Analysis

Healthcare Services