Pharmaceuticals

Germany Lymphoma Therapeutics Market Analysis

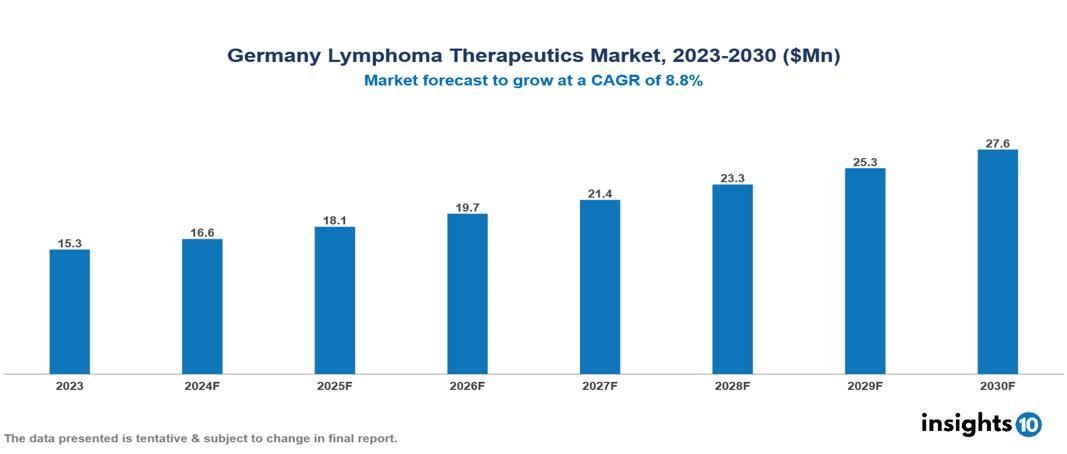

Germany's Lymphoma Therapeutics Market was valued at $15.27 Mn in 2023 and is predicted to grow at a CAGR of 8.80% from 2023 to 2030, to $27.55 Mn by 2030. The key drivers of this industry include high lymphoma incidence, awareness campaigns, and the geriatric population. The industry is primarily dominated by Bristol Myers Squibb Company, Novartis AG, Kyowa Kirin Co., and Merck & Co. among others.

Buy Now

Germany Lymphoma Therapeutic Market Executive Summary

Germany's Lymphoma Therapeutics Market was valued at $15.27 Mn in 2023 and is predicted to grow at a CAGR of 8.80% from 2023 to 2030, to $27.55 Mn by 2030.

Lymphoma comprises two primary forms: Hodgkin lymphoma (HL) and non-Hodgkin lymphoma (NHL), both impacting the lymphatic system. HL is characterized by the presence of Reed-Sternberg cells, while NHL encompasses a variety of subtypes originating from lymphocytes. Symptoms commonly associated with these conditions include the swelling of lymph nodes, fever, weight loss, fatigue, and itching. Treatment modalities range from chemotherapy, radiation therapy, immunotherapy, and targeted therapy, to stem cell transplant.

In Germany, non-Hodgkin lymphoma is most common among older individuals, with approximately 18,320 new cases in 2020. Diagnosis typically occurs at an average age of 73 for women and 71 for men. Changes in diagnostic criteria, such as the reclassification of chronic lymphocytic leukemias, have led to higher incidence rates. However, the average prognosis remains favorable, with 5-year survival rates of 72% for women and 71% for men, although these rates decline with disease progression. Risk factors include immunodeficiency, viral exposure, radiation, chemotherapy, and autoimmune diseases. The key drivers of this industry include high lymphoma incidence, awareness campaigns, and the geriatric population. Restraints include drug resistance, financial barriers, adverse effects, etc.

The industry is primarily dominated by Bristol Myers Squibb Company, Novartis AG, Kyowa Kirin Co., and Merck & Co. among others.

Market Dynamics

Market Growth Drivers

Rising Incidence: Similar to global trends, Germany witnesses an uptick in lymphoma cases, propelling the demand for effective treatments to address the growing patient population's needs. This surge emphasizes the necessity for innovative therapies catering to the diverse stages and requirements of lymphoma.

Awareness Campaigns: Public and private entities actively engaged in promoting awareness initiatives regarding lymphoma across Germany. These campaigns aim to educate individuals about the symptoms, signs, and importance of early detection, thereby fostering proactive healthcare-seeking behavior. Such efforts not only enhance patient outcomes but also stimulate market growth for lymphoma treatments.

Geriatric Population: The growing geriatric population in Germany contributes to the increasing incidence of lymphoma. As individuals age, they become more susceptible to developing lymphoma, thereby fuelling the demand for therapies tailored to the unique healthcare needs of older adults.

Advancements in Therapies: Ongoing advancements in T-cell lymphoma-specific treatments represent a significant driver for market growth. With continuous progress in therapeutic innovations, there is greater potential to improve patient outcomes and expand treatment options for lymphoma.

Market Restraints

Drug Resistance: Over time, lymphoma cells can develop resistance to existing treatment options, particularly for some types of Hodgkin's lymphoma. This resistance poses a significant challenge. The market is driven by the need for new treatment options that can overcome drug resistance and remain effective for longer periods.

Financial Barriers: While advanced therapies, including immune checkpoint inhibitors, hold promise for lymphoma patients, their steep costs pose substantial financial burdens in Germany. Accessibility to such treatments may be restricted by healthcare system reimbursement policies and affordability concerns, potentially impacting treatment choices and patient outcomes. Mitigating these cost barriers through innovative pricing mechanisms and reimbursement strategies is imperative to ensure equitable access to state-of-the-art lymphoma treatments for all patients across Germany.

Adverse Effects: Safety concerns associated with lymphoma drugs serve as a significant restraint for market growth. Adverse effects and potential risks associated with certain therapies may deter patients from seeking treatment or impact treatment adherence, thereby influencing market dynamics.

Regulatory Landscape and Reimbursement Scenario

In Germany, The Federal Ministry of Health (BMG) serves as the primary authority governing health policies, including pharmaceutical regulations. Working in conjunction with the BMG, the Federal Institute for Pharmaceuticals and Medical Devices (BfArM) holds responsibility for approving marketing authorization for drugs, including those aimed at treating lymphoma. This regulatory framework ensures that therapies undergo rigorous evaluation before entering the market, safeguarding patient safety and efficacy standards.

German Lymphoma Alliance (GLA): The GLA is a registered society focused on improving treatment outcomes for patients with malignant lymphomas in Germany. They coordinate expertise in research, diagnostics, and treatment, with a particular emphasis on non-Hodgkin lymphoma. The GLA brings together the activities of various study groups and networks, creating a platform for translational and clinical lymphoma research. Moreover, reimbursement decisions for lymphoma treatments are determined by the Joint Federal Committee (G-BA), comprising representatives from medical professionals, hospitals, and health insurance companies. This committee evaluates the cost-effectiveness and clinical efficacy of medical interventions, including those targeting lymphoma.

Competitive Landscape

Key Players

Here are some of the major key players in the Germany Lymphoma Therapeutic Market:

- Bristol Myers Squibb Company

- Novartis AG

- Kyowa Kirin Co

- Merck & Co

- Seattle Genetics

- Spectrum Pharmaceuticals

- Takeda Pharmaceutical Company Limited

- Eisai

- Epizyme

- BeiGene

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Germany Lymphoma Therapeutic Market Segmentation

Type of Lymphoma

- B-Cell Lymphomas

- T-Cell Lymphomas

Treatment Type

- Radiation

- Chemotherapy

- Light Therapy

- Surgery

- Medication

- Others

Diagnosis

- Blood Cell Counts

- Tissue Biopsy

- Computed Tomography (CT) Scan

- Positron Emission Tomography (PET) Scan

- Magnetic Resonance Imaging (MRI) Scan

- Other

End-Users

- Hospitals

- Homecare

- Speciality Centres

Distribution Channel

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

UK Insulin Market Analysis

Pharmaceuticals

Japan Diabetes Management Market Analysis

Pharmaceuticals

Indonesia Interferons Market Analysis

Related reports (by geography)

Pharmaceuticals

Germany Diabetes Management Market Analysis

Pharmaceuticals

Germany Cardiac Arrhythmia Therapeutics Market Analysis

Pharmaceuticals

Germany Influenza Vaccine Market Analysis

Medical Devices