Healthcare Services

Germany Connected Healthcare Market Analysis

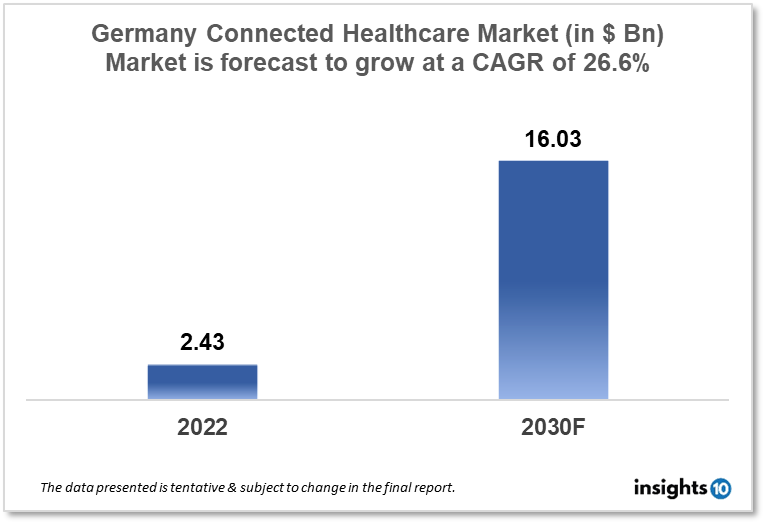

The Germany-connected healthcare market is projected to grow from $2.43 Bn in 2022 to $16.03 Bn by 2030, registering a CAGR of 26.6% during the forecast period of 2022 - 2030. The main factors driving the growth would be the ageing population, strong healthcare infrastructure, research and development infrastructure and government support. The market is segmented by type, function and by application. Some of the major players include Siemens Healthineers, Fresenius Medical Care, CompuGroup Medical, Telekom Healthcare Solutions, Philips Healthcare, IBM, Medtronic, Apple and Honeywell.

Buy Now

Germany Connected Healthcare Market Executive Summary

The Germany-connected healthcare market is projected to grow from $2.43 Bn in 2022 to $16.03 Bn by 2030, registering a CAGR of 26.6% during the forecast period of 2022 - 2030. Germany spent $4874.39 on healthcare per person in 2019, which was 28% more than the EU average of $3812. Germany also spends the greatest percentage of its GDP (11.7%) on healthcare when compared to other EU nations. Just 12.7% of people in the country pay for their own healthcare, which is significantly less than the majority of other EU countries. This is due to the fact that the majority of health spending in the EU is funded by public sources.

Connected healthcare technology is being utilised to enhance patient outcomes and lower healthcare costs by enabling remote monitoring, telemedicine, and patient self-management. The industry offers a wide variety of goods and services, such as software programs, digital health platforms, and medical devices.

Within Europe, Germany offers the biggest market for medical and life science products. Several multinational corporations planning to increase their footprint favour it due to both market demand and geographic considerations. The connected healthcare market in Germany is a fast-expanding industry with a broad variety of products and services. The market features products made by both established businesses and start-ups, including medical devices, software solutions, and digital health platforms.

Market Dynamics

Market Growth Drivers

The Germany-connected healthcare market is expected to be driven by factors such as:

- Ageing population- The country's ageing population is raising the expense of healthcare and driving demand for healthcare services. By enabling telemedicine, remote monitoring, and patient self-management, connected healthcare technologies can aid in lowering these expenses

- Strong healthcare infrastructure- The introduction of connected healthcare technology is ideally suited to Germany's highly developed healthcare infrastructure

- Research and development ecosystem- Germany offers a robust environment for research and development, with several universities and research organisations devoted to creating cutting-edge healthcare solutions

- Government support- The German government has established various measures to encourage the adoption of digital health technologies, notably the Digital Healthcare Act (DVG), which establishes a legal framework for health insurance companies to reimburse for digital health services

Market Restraints

The following factors are expected to limit the growth of the connected healthcare market in Germany:

- Complex regulatory landscape- Although the regulatory system in Germany is intended to safeguard patient safety and encourage innovation, it can be challenging for businesses to understand and can impede the pace of progress

- Data privacy concerns- In Germany, patients may be hesitant to use connected healthcare services due to concerns about data privacy and security

- Financial Challenges- The adoption of connected healthcare technologies in Germany has financial obstacles because many healthcare organisations and providers are likely to lack the funds to make such investments

Competitive Landscape

Key Players

- Siemens Healthineers (DEU)- It is a medical technology firm that focuses on diagnostics, imaging, and laboratory equipment

- Fresenius Medical Care (DEU)- It is a provider of connected healthcare solutions for the dialysis industry

- CompuGroup Medical (DEU)- It offers electronic health records and telemedicine services, among other healthcare IT solutions

- Telekom Healthcare Solutions (DEU)- It is a subsidiary of Deutsche Telekom and a provider of connected care services and IT solutions for the healthcare industry

- Philips Healthcare- Philips healthcare is a multinational corporation that offers a range of healthcare solutions, including connected care technologies

- IBM- IBM Watson Health is a technology firm based in the US that provides a variety of healthcare solutions, including data analytics and artificial intelligence for connected care

- Medtronic- A variety of devices for connected healthcare are provided by the Irish medical device manufacturer Medtronic, including remote monitoring and diagnostic equipment

- Apple- A range of health and fitness features are accessible on Apple's Health app and Apple Watch, and the company is increasingly cooperating with healthcare groups to incorporate its technologies into patient care

- Honeywell- Honeywell is a multinational conglomerate that primarily engages in four business sectors: aerospace, building technologies, performance materials and technologies, and safety and productivity solutions

Notable Deals

March 2022: CompuGroup Medical (CGM), a global leader in e-health, has announced the purchase of Insight Health Group, a major provider of healthcare data services. The acquisition enhances CGM's position as a provider of cutting-edge data solutions.

Healthcare Policies and Regulatory Landscape

Several national and EU-level policies and regulations have an impact on the regulatory environment for connected healthcare in Germany. The Medical Devices Regulation (MDR), the General Data Protection Regulation (GDPR), and the Digital Healthcare Act (DVG) are the main laws and regulations that affect the connected healthcare sector in Germany. The MDR establishes standards for medical equipment, including connected healthcare devices, in terms of their performance and safety. The GDPR governs how personal data is processed, which has consequences for how health data is gathered and used in linked healthcare. A legislative framework for the reimbursement of digital health services by health insurance companies is provided by the DVG, which was created in 2020 to encourage the adoption of digital health technology in Germany. These laws and regulations must be carried out and enforced by the German Federal Ministry of Health.

Reimbursement Scenario

The Digital Healthcare Act (DVG), which was introduced in 2020, governs Germany's linked healthcare reimbursement practices. The DVG offers a legislative framework for health insurance providers to pay for digital health services, including connected healthcare devices. Health insurance providers must pay for digital health applications that have been approved by the BfArM, and the Federal Institute for Drugs and Medical Devices, and are considered to be medically necessary under the DVG. Health insurance carriers and service providers negotiate the rates of compensation for related healthcare services. The DVG also outlines plans for the building of a national digital health infrastructure, which would include a platform for safe digital health data sharing and a directory of digital health applications.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Connected Healthcare Market Segmentation

By Type (Revenue, USD Billion):

Based on the Type the market is segmented into mHealth services, mHealth Devices, and E- Prescription

- MHealth services

- mHealth Devices

- E- Prescription

By FunctionType (Revenue, USD Billion):

- Remote patient monitoring

- Clinical monitoring

- Telemedicine

- Others (Assisted Living)

By Application Type (Revenue, USD Billion):

- Diagnosis and Treatment

- Monitoring Application

- Wellness and Prevention

- Healthcare management

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

The Germany-connected healthcare market is projected to grow from $2.43 Bn in 2022 to $16.03 Bn by 2030, registering a CAGR of 26.6% during the forecast period of 2022 - 2030.

The Germany-connected healthcare market is segmented by type (m-health services, m-health devices and e-prescription), by function (remote patient monitoring, clinical monitoring, telemedicine and others), and by application type (diagnosis and treatment, monitoring application, wellness and prevention, healthcare management and others).

Some of the major players in the Germany connected healthcare market are Siemens Healthineers, Fresenius Medical Care, CompuGroup Medical, Telekom Healthcare Solutions, Philips Healthcare, IBM, Medtronic, Apple and Honeywell.

Related reports (by category)

Healthcare Services

Romania In Vitro Fertilisation (IVF) Service Market Analysis

Healthcare Services

Tanzania Healthcare Insurance Market Analysis

Healthcare Services

UAE Financial Assistance Programs Market Analysis

Related reports (by geography)

Pharmaceuticals

Germany Pneumococcal Vaccines Market Analysis

Rare Diseases

Germany Soft Tissue Sarcoma Market Analysis

Pharmaceuticals