Pharmaceuticals

Germany Clinical Nutrition for Chronic Kidney Diseases Market Analysis

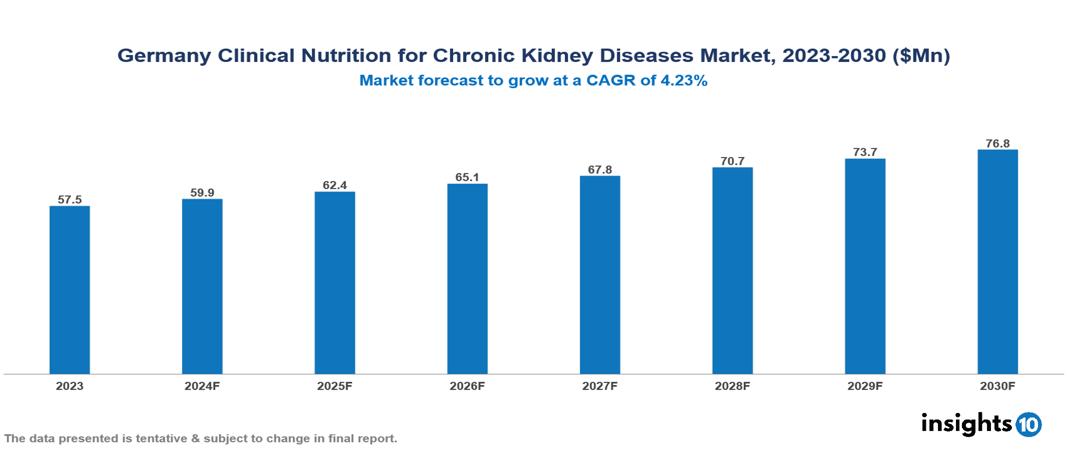

Germany Clinical Nutrition for Chronic Kidney Diseases Market was valued at $57.50 Mn in 2023 and is predicted to grow at a CAGR of 4.23% from 2023 to 2030, to $76.80 Mn by 2030. The key drivers of this industry include the high prevalence of CKD, increasing awareness and education, and technological advancements. The industry is primarily dominated by Abbott Nutrition, Pfizer Inc., Bayer AG, and Nestlé Health Science among others.

Buy Now

Germany Clinical Nutrition for Chronic Kidney Diseases Market Executive Summary

Germany Clinical Nutrition for Chronic Kidney Diseases Market was valued at $57.50 Mn in 2023 and is predicted to grow at a CAGR of 4.23% from 2023 to 2030, to $76.80 Mn by 2030.

Chronic kidney disease (CKD) is a gradual loss of kidney function over at least three months, often progressing silently due to the absence of early symptoms. The main causes include diabetes and high blood pressure, though family history and other conditions also contribute. As CKD advances through stages, it may necessitate dialysis or a kidney transplant and is associated with increased risks of heart disease, stroke, and bone issues. Management focuses on slowing disease progression, symptom management, and preventing complications through dietary changes, medications, and blood pressure control. Key dietary adjustments include moderating protein intake, managing fluid levels, controlling electrolytes like sodium, potassium, and phosphorus, and ensuring sufficient calorie intake to avoid malnutrition. Early detection and screening are crucial for those at risk.

In Germany, Approximately 10% of individuals aged 40 and older have CKD Stages 3–5, highlighting its comparable prevalence to other major chronic conditions like coronary heart disease and diabetes. The incidence of end-stage kidney disease (ESKD) is approximately 950 cases per Mn population, indicating a substantial burden on healthcare resources.

The market therefore is driven by significant factors like the high prevalence of CKD, increasing awareness and education, and technological advancements. However, the scarcity of qualified dietitians, the high cost of treatment, and limited reimbursement restrict the growth and potential of the market.

Prominent players in this field are Abbott Nutrition, Pfizer Inc., Bayer AG, and Nestlé Health Science among others.

Market Dynamics

Market Growth Drivers

High Prevalence of CKD: Studies estimate CKD prevalence in Germany at 2% to 7% among adults aged 18 years and older. The country faces a significant burden of chronic kidney disease, influenced by an aging population, diabetes, hypertension, and lifestyle factors. This high prevalence underscores the need for clinical nutrition solutions specifically designed to manage CKD, addressing the healthcare demands of affected individuals effectively.

Increasing Awareness and Education: There is growing awareness among healthcare professionals and patients about the importance of nutrition in managing CKD. Education initiatives and awareness campaigns contribute to greater adoption of clinical nutrition therapies, enhancing market growth.

Technological Advancements: Ongoing advancements in medical technology and nutrition science lead to the development of innovative products and solutions for CKD management. These advancements improve efficacy and patient compliance with clinical nutrition interventions.

Market Restraints

Scarcity of Qualified Dietitians: Germany faces challenges in the availability of qualified dietitians with specialized expertise in CKD nutrition. This scarcity limits the accessibility of tailored nutritional guidance for CKD patients, hindering their ability to receive personalized care and dietary management.

High Cost of Treatment: The high cost associated with clinical nutrition products and specialized dietary supplements for CKD management may limit affordability, particularly for patients without adequate insurance coverage. This can restrict market penetration and patient access to essential nutritional interventions.

Limited Reimbursement: While Germany has a comprehensive healthcare system, reimbursement policies for clinical nutrition specifically targeted at CKD management may be limited. Inconsistent coverage by health insurance providers could hinder the widespread adoption of these products among CKD patients.

Regulatory Landscape and Reimbursement Scenario

Germany's regulatory framework for CKD-specific clinical nutrition is robust and overseen by key institutions such as the Bundesinstitut für Arzneimittel und Medizinprodukte (BfArM) and the Bundesministerium für Ernährung und Landwirtschaft (BMEL). BfArM regulates medical devices used in CKD management, ensuring their safety and efficacy. Meanwhile, BMEL oversees the safety and quality of food products formulated for special dietary needs, including those aimed at managing CKD. Both bodies adhere to stringent EU regulations that maintain consistency and high standards across member states. Key regulatory considerations include the classification of CKD nutritional products, which dictates the regulatory pathway for approval, stringent labeling requirements to ensure clear information for consumers, and, in some cases, the necessity for clinical trials to validate product safety and efficacy.

In terms of reimbursement, Germany's social health insurance system, comprising Statutory Health Insurance Funds (Krankenkassen), plays a pivotal role. These funds typically reimburse costs associated with CKD treatment, including consultations with dietitians and certain types of medically prescribed nutritional products. Reimbursement criteria hinge on a physician's prescription and documented medical necessity, with cost-effectiveness, also factored into coverage decisions. Additionally, private health insurance plans offer supplementary coverage, which may extend to consultations with dietitians and a broader range of specialized nutritional products beyond what is covered by statutory health insurance. This dual reimbursement approach helps ensure broader access to essential CKD management tools, enhancing overall healthcare outcomes for affected individuals in Germany.

Competitive Landscape

Key Players

Here are some of the major key players in the Germany Clinical Nutrition for Chronic Kidney Diseases Market

- Abbott Nutrition

- Pfizer Inc.

- Bayer AG

- Nestlé Health Science

- Otsuka Pharmaceutical

- Mead Johnson & Company, LLC

- Danone S.A.

- Victus, Inc.

- B. Braun Melsungen AG

- Fresenius Kabi AG

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Germany Clinical Nutrition for Chronic Kidney Diseases Market Segmentation

Product

- Oral Nutrition

- Parenteral Nutrition

- Enteral Feeding Formulas

Stages

- Adult

- Paediatric

Sales Channel

- Online

- Retail

- Institutional Sales

End-User

- Hospitals

- Homecare

- Specialty Clinics

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Philippines End-stage Renal Disease(ESRD) Market Analysis

Pharmaceuticals

Africa Retail Pharmacy Market Analysis

Pharmaceuticals

Indonesia Diabetic Retinopathy Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

Germany Parkinson Disease Market Analysis

Medical Devices

Germany Bariatric Surgery Devices Market Analysis

Digital Health

Germany ePharmacy Market Analysis

Pharmaceuticals