Medical Devices

Germany Cardiac Surgery Instruments Market Analysis

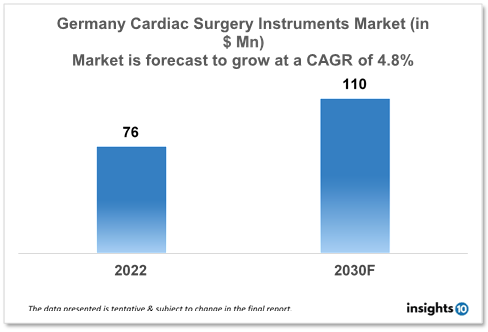

The Germany Cardiac Surgery Instruments Market is expected to witness growth from $76 Mn in 2022 to $110 Mn in 2030 with a CAGR of 4.80% for the forecasted year 2022-2030. In Germany, coronary heart disease, heart failure, and atrial fibrillation are among the leading causes of morbidity and death. The demand for cardiac surgery equipment is anticipated to increase as these illnesses become more common in the German healthcare market. The market is segmented by type, application and by end user. Some key players in this market include KLS Martin, Aesculap AG, RZ Medizintechnik GmbH, LivaNova, B. Braun, Medline Industries and STILLE.

Buy Now

Germany Cardiac Surgery Instruments Healthcare Market Executive Analysis

The Germany Cardiac Surgery Instruments Market size is at around $76 Mn in 2022 and is projected to reach $110 Mn in 2030, exhibiting a CAGR of 4.80% during the forecast period. Recent health spending in Germany will account for 13% of GDP in 2023. The government provided transfers and assistance totalling $72,05 Bn in 2021 to fund all of Germany's healthcare costs. This was a $17.30 Bn, or 31.5%, rise from 2020. Thus, of the $4,581 Bn in current health expenses, or 15.7% of them, were made up of government transfers and subsidies, an increase of 3% from the year before.

In Germany, cardiovascular illnesses account for a significant portion of morbidity and mortality. The most prevalent form of heart illness in Germany is coronary heart disease (CHD). CHD affects 3.8 million individuals in Germany. In Germany, there are about 220 cases of CHD for every 100,000 individuals. When the heart cannot pump enough blood to satisfy the body's demands, it results in heart failure, a serious condition. In Germany, 1.8 million individuals suffer from heart failure. About 320 out of 100,000 individuals in Germany experience heart failure each year. Atrial fibrillation is an irregular heartbeat that raises the risk of blood blockages, strokes, and other problems. In Germany, atrial fibrillation affects an estimated 1.8 million individuals. About 240 per 100,000 individuals in Germany experience atrial fibrillation each year.

In Germany, the use of specialist cardiac surgery equipment has enhanced patient outcomes, resulting in lower mortality rates, fewer complications, and shorter hospital stays. Due to this, cardiac surgery is now both better and more successful than ever before. German cardiac doctors also use minimally invasive procedures, which allow for smaller incisions and cause patients to experience less pain, scarring, and recuperation time. These procedures require the use of specialist equipment like endoscopes, laparoscopes, and robot-assisted surgical tools. Instruments for cardiac surgery are specialized tools that cardiac surgeons use to carry out difficult operations on the heart and blood vessels. These tools are vital to the success of cardiac surgeries because they are made to be precise, reliable, and simple to use. In open heart surgery, cardiac surgery tools are used to replace or repair heart valves, open blocked or congested coronary arteries, or treat congenital heart defects. Surgery is precise, effective, and secure thanks to the use of specialized equipment.

Market Dynamics

Market Growth Drivers

In Germany, atrial fibrillation is one of the leading causes of morbidity and death, followed by heart failure and coronary heart disease. The need for cardiac surgery equipment is expected to increase as these diseases spread. The use of robotic surgery, and computer-assisted guidance systems, among other highly advanced cardiac surgery instruments, has increased the safety, efficacy, and efficiency of heart operations. The implementation of these cutting-edge technologies will likely increase demand for cardiac surgery equipment. Germany's populace is ageing, with a sizable portion of the population being over 65. The demand for cardiac surgery equipment is expected to increase because older people are more prone to develop cardiovascular diseases. In Germany, people are becoming more and more conscious of the value of preventive healthcare and early detection of cardiac diseases. The demand for cardiac surgery equipment is anticipated to increase as more people look for prompt medical attention.

Market Restraints

In Germany, the expense of cardiac surgeries is typically high, which may reduce the demand for cardiac surgery instruments among patients and healthcare professionals. Alternative therapies, such as prescription medication or dietary modifications, can be used to address some cardiac conditions. The existence of these substitutes could reduce the demand for instruments used in cardiac surgery.

Competitive Landscape

Key Players

- KLS Martin (DE)

- Aesculap AG (DE)

- RZ Medizintechnik GmbH (DE)

- LivaNova

- B. Braun

- Medline Industries

- STILLE

Recent Notable Deals

2022: The German business Pulsion Medical Systems SE, which creates and manufactures medical equipment used in cardiac surgery and cardiovascular monitoring, was acquired by Getinge. It was anticipated that the deal would improve Getinge's standing in the global cardiovascular monitoring industry.

Healthcare Policies and Regulatory Landscape

The new Medical Device Regulation (MDR) in Germany took effect on May 26, 2021, replacing the Medical Device Directive (MDD). The instruments used in cardiac surgery aim to ensure a high level of performance and safety. Before their products can be marketed in Germany, manufacturers must abide by the MDR and obtain certification from notified organizations. In Germany, the statutory health insurance scheme (SHI) covers about 85% of the population, with private health insurance (PHI) covering the remaining 15%. Based on a list of positively accepted products, the SHI system reimburses medical devices and is heavily controlled. These surgical instruments for the heart are compliant with high requirements for quality and safety. Germany is moving toward a healthcare system that grounds payments on patient outcomes and the effectiveness of the provided care rather than the number of services provided. This motivates medical professionals to perform cardiac surgery using top-tier, cutting-edge equipment that improves patient outcomes and reduces immediate costs. Recent initiatives in the nation to promote digital health include the Digital Healthcare Act (DHG) and the Digital Health Applications (DiGA) program. These efforts encourage the use of digital technologies and cutting-edge medical gear, such as instruments for cardiac surgery, in order to improve patient care and outcomes.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiac Surgery Instruments Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into segments in this study based on the goods, applications, end users, and geographical areas. The market is divided into forceps, scissors, needle holders, clamps, and other cardiac surgery instruments based on the product. In 2017 the forceps category led the market, and it is anticipated that it will increase at the fastest rate going forward. The rise in heart surgeries and the frequent usage of forceps in most cardiac procedures are credited with the segment's strong growth.

- Forceps

- Vascular Forceps

- Grasping Forceps

- Other Forceps

- Needle Holders

- Scissors

- Clamps

- Other Cardiac Surgical Instruments

By Application (Revenue, USD Billion):

The market is further segmented by application into paediatric cardiac surgery, heart valve surgery, coronary artery bypass graft (CABG), and other applications. The Germany market's largest and fastest-growing application segment is CABG. This is mostly explained by the increased prevalence of heart illnesses and the consequent rise in surgical treatments. The second-largest category is heart valve surgery.

- Coronary Artery Bypass Graft (CABG)

- Heart Valve Surgery

- Pediatric Cardiac Surgery

- Other Applications

By End User (Revenue, USD Billion):

Based on the end user, the market is segmented into hospitals and cardiac centers, and ambulatory surgery centers. The hospitals and cardiac centers segment is expected to dominate the market for cardiac surgery instruments. Growth in this end-user segment can be attributed to the increasing incidence of cardiac and heart valve diseases and the subsequent increase in the number of cardiac surgery procedures.

- Hospitals and Cardiac Centers

- Ambulatory Surgery Centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Middle East Biomaterials in Healthcare Market Analysis

Medical Devices

Nigeria Pain Management Devices Market Analysis

Medical Devices

Hong Kong Cardiac Surgery Instruments Market Analysis

Related reports (by geography)

Pharmaceuticals

Germany Diabetic Retinopathy Therapeutic Market Analysis

Medical Devices

Germany Pharmacy Automation Device Market Analysis

Pharmaceuticals