Digital Health

Germany Artificial Intelligence (AI) in Medical Imaging Market Analysis

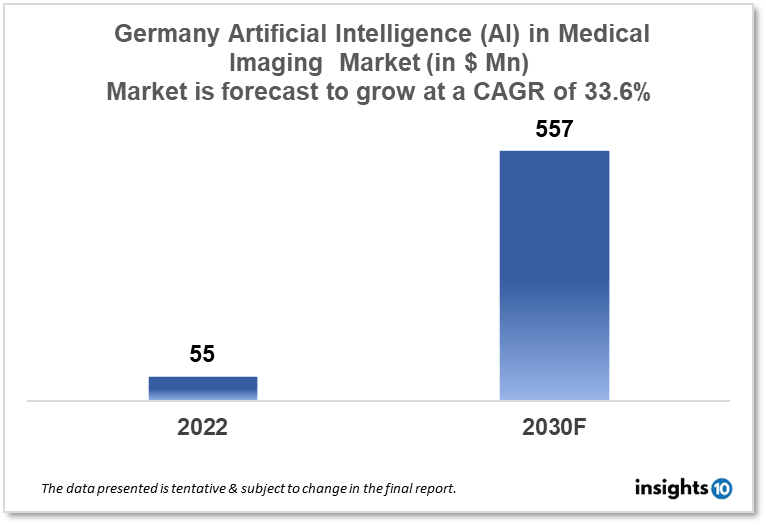

The Germany Artificial Intelligence (AI) in Medical Imaging market size was valued at $55 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 33.6% from 2022 to 2030 and will reach $557 Mn. The market is segmented by AI technology, solution, modality, application, and end User. The Germany Artificial Intelligence (AI) in the Medical Imaging market will grow due to advances in AI and machine learning algorithms that are making it possible to develop more accurate and efficient medical imaging software. Some of the key players in this market are Siemens Healthineers, Philips Healthcare, Agfa-Gevaert Group, Canon Medical Systems, Fujifilm, and others.

Buy Now

Germany Artificial Intelligence (AI) in Medical Imaging

Market Executive Summary

The Germany Artificial Intelligence (AI) in Medical Imaging market size was valued at $55 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 33.6% from 2022 to 2030 and will reach $ 557. Germany is one of the leading countries in Europe when it comes to investing in AI technology for healthcare. The German government has recognized the potential of AI in healthcare and has allocated significant resources to promote its development and use. According to a report by the German Federal Ministry of Education and Research, the German government invested approximately $685.92 Mn in AI research and development in 2019. A significant portion of this investment was dedicated to healthcare-related projects, including the development of AI-powered medical imaging technologies. In addition to government investment, private sector investment in AI in healthcare is also growing in Germany. In 2020, healthcare AI startups in Germany raised over $738.68 Mn in funding, according to a report by McKinsey & Company.

One of the most promising areas of health and medical innovation is the use of artificial intelligence (AI) in medical imaging. Medical imaging uses AI in a variety of ways, including image acquisition, processing for assisted reporting, planning for follow-up visits, data storage, data mining, and more. AI has demonstrated impressive sensitivity and precision in the classification of imaging abnormalities in recent years, and it guarantees to enhance tissue-based detection and characterization. A branch of artificial intelligence called machine learning (ML) uses computational models and algorithms that mimic the structure of the brain's biological neural networks. Layers of interconnected nodes make up the architecture of neural networks. The adoption of AI in healthcare and medical imaging altered the diagnostic process, which fueled the expansion of the market for AI in medical imaging across the nation.

Artificial Intelligence (AI) in Medical Imaging is being used in various regions of Germany to improve healthcare outcomes and increase efficiency. In Berlin, the Charité – Universitätsmedizin Berlin, one of the largest university hospitals in Europe, is using AI-powered medical imaging to improve the accuracy of diagnoses and reduce the time needed for image interpretation. The hospital is also developing an AI-powered tool to detect lung cancer in CT scans. Moreover, the Technical University of Munich is working on developing AI-powered algorithms for medical image analysis, including identifying tumors and detecting brain injuries.

The German Cancer Research Center in Heidelberg is using AI-powered medical imaging to improve cancer detection and diagnosis. The center has developed an AI-powered system that can detect breast cancer in mammograms with high accuracy. Furthermore, the University Hospital of Tübingen in Stuttgart is using AI-powered medical imaging to improve the accuracy of diagnoses and reduce the time needed for image interpretation. The hospital is also developing an AI-powered tool to detect lung cancer in CT scans.

Overall, Germany's investment in AI technology for healthcare is significant and is expected to continue to grow in the coming years. With a strong focus on research and development, as well as public and private investment, Germany is well-positioned to be a leader in the use of AI in healthcare.

Market Dynamics

Market Growth Drivers

Medical imaging is in greater demand as a result of the ageing population, which is also boosting demand for healthcare services. AI-based medical imaging has the potential to increase medical imaging's effectiveness and accuracy, which could help to meet this expanding demand.

Developments in AI and machine learning algorithms are making it possible to produce more accurate and efficient medical imaging software. This is encouraging Germany to use AI-based medical imaging technologies.

Possible financial savings by increasing effectiveness and lowering the need for expensive procedures, AI-based medical imaging offers the potential to save healthcare costs. Furthermore, A faster and more accurate diagnosis is one way that AI-based medical imaging has the potential to improve patient outcomes.

Market restraints:

Germany has stringent regulations governing AI-based medical imaging software. Smaller businesses may find it difficult to enter the market because they lack the resources to meet these requirements.

The creation and application of AI-based medical imaging technologies currently lack standards. This might make it challenging to evaluate the efficacy of various treatments and can raise doubts over their application. Moreover, the application of AI in medical imaging poses issues with data security and privacy. People could be reluctant to submit their medical information due to worries about data breaches or patient information misuse.

Competitive Landscape

Key Players

- Siemens Healthineers (Germany)

- IBM Watson Health (USA/Germany)

- Brainlab (Germany)

- Arterys (USA/Germany)

- ContextVision (Sweden/Germany)

- Fujifilm (Japan/Germany)

- Esaote (Italy/Germany)

- Sectra (Sweden/Germany)

- Agfa HealthCare (Belgium/Germany)

- Aidence (Netherlands/Germany)

Recent Developments

In 2021, Siemens Healthineers launched the Cios Flow, a mobile C-arm system that incorporates AI-based algorithms to enhance surgical imaging capabilities.

In 2020, Siemens Healthineers acquired Varian Medical Systems, a leader in cancer care solutions, with the goal of integrating AI and machine learning technologies to improve patient outcomes.

Healthcare Policies and Regulatory Landscape

In Germany, the use of Artificial Intelligence (AI) in Medical Imaging is regulated by the Medical Devices Act (MPG) and the Medical Devices Operator Ordinance (MPBetreibV). These regulations require that all AI-based medical devices used in Germany meet certain safety, efficacy, and quality standards. Additionally, the German Federal Ministry of Health and the German Federal Ministry for Economic Affairs and Energy have jointly published a national AI strategy that includes specific measures for the development and deployment of AI in healthcare, including medical imaging. The strategy emphasizes the importance of ensuring data protection, patient safety, and ethical considerations in the use of AI-based technologies in healthcare. In addition, the strategy highlights the need for collaboration between stakeholders, including industry, academia, and government, to promote innovation and drive the adoption of AI-based solutions in healthcare.

1. Executive Summary

1.1 Digital Health Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Digital Health Policy in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Artificial Intelligence (AI) in Medical Imaging Market Segmentation

By AI Technology

- Deep Learning

- Natural Language Processing (NLP)

- Others

By Solution

- Software Tools/ Platform

- Services

- Integration

- Deployment

By Modality

When compared to CT scans, magnetic resonance imaging can produce pictures that are free of imperfections. Due to its efficiency in obtaining details and better-quality pictures of soft tissues, the MRI is frequently seen as a superior alternative to X-rays. Utilizing optical coherence tomography, three-dimensional interactions between the retina and membranes are made possible in order to control the vitreoretinal disease.

- CT Scan

- MRI

- X-rays

- Ultrasound Imaging

- Nuclear Imaging

By Application

The market is dominated by the digital pathology segment, which can be linked to pathologists' rising productivity. A validation tool for image analytics is provided by digital pathology, helping pathologists process more slides in less time. This facilitates early illness identification and quicker therapy initiation. AI and digital pathology also assist doctors in making patient-centered decisions. The oncology market is also expected to grow in popularity as more individuals become aware of cancer and its increased incidence in the public. Personalized therapy is made possible by artificial intelligence algorithms that identify and comprehend the nature of malignancies. The second section focUses on AI-driven diagnostic imaging for the heart, brain, breast, and mouth.

- Digital Pathology

- Oncology

- Cardiovascular

- Neurology

- Lung (Respiratory System)

- Breast (Mammography)

- Liver (GI)

- Oral Diagnostics

- Other

By End Use

The market is dominated by the healthcare sector. This is becaUse hospitals are widely dispersed and accessible; hence, many patients like hospitals. The market for medical imaging AI is also anticipated to benefit from favorable reimbursement regulations. During the anticipated time, diagnostic centers are anticipated to grow in popularity. This may be attributable to elements including rising patient awareness and a desire for diagnostic procedures and tests, all of which are fueling the market's expansion. Due to its ease in providing high-quality medical facilities in remote places, particularly rural ones, the ambulatory category is expected to develop at a quicker CAGR throughout the projection period. The availability of qualified surgeons and a surplAustralia of the necessary equipment are contributing to the expansion of the hospital market. Government assistance in emerging nations is likely to boost hospital infrastructure and technologies throughout the forecast period, which is anticipated to caUse the hospital segment to see growth.

- Hospital and Healthcare Providers

- Patients

- Pharmaceuticals and Biotechnology Companies

- Healthcare Payers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Digital Health

Switzerland ePharmacy Market Analysis

Digital Health

Morocco Digital Therapeutics Market Analysis

Related reports (by geography)

Rare Diseases

Germany Hodgkins Lymphoma Drugs Market Analysis

Pharmaceuticals

Germany Precision Medicine Market Analysis

Healthcare Services