Digital Health

France Medical Digital Imaging System Market Analysis

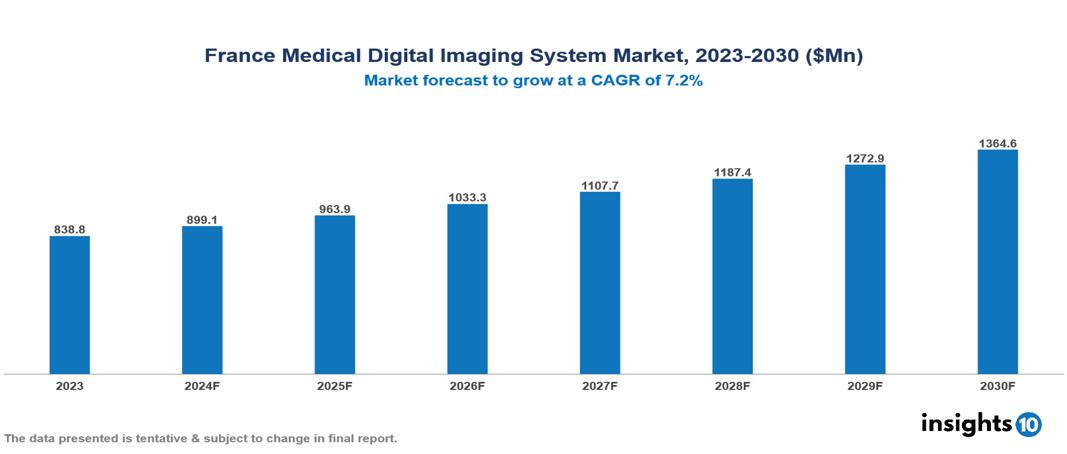

The France Medical Digital Imaging System Market was valued at $838.75 Mn in 2023 and is predicted to grow at a CAGR of 7.2% from 2023 to 2030, to $1364.57 Mn by 2030. The key drivers of this industry include an aging population, technological advancements, and government initiatives. The industry is primarily dominated by players such as Siemens Healthineers, GE Healthcare, Philips Healthcare, and Canon Medical Systems among others.

Buy Now

France Medical Digital Imaging System Market Executive Summary

The France Medical Digital Imaging System Market was valued at $838.75 Mn in 2023 and is predicted to grow at a CAGR of 7.2% from 2023 to 2030, to $1364.57 Mn by 2030.

Medical digital imaging systems comprise various technologies employed in healthcare to create visual representations of the body's internal structures for clinical analysis and medical interventions. These systems have evolved considerably and are crucial in contemporary medicine, assisting in the diagnosis and treatment of diseases. Medical imaging encompasses ultrasound, x-rays, computed tomography (CT scans), Magnetic Resonance Imaging (MRI), and nuclear medicine technologies.

In 2023, for CT scanners, there were 13.4 Mn scans conducted in France. The market is driven by significant factors like an increasing aging population, technological advancements, and supportive government initiatives. However, high cost, regulatory challenges, and, data security and privacy restrict the growth and potential of the market.

Prominent players in this field include Siemens Healthineers, GE Healthcare, Philips Healthcare, and Canon Medical Systems among others.

Market Dynamics

Market Growth Drivers

Rising Aging Population: In France, 26% of the population is over 60 as of 2023, equating to one in four inhabitants, and this is projected to increase to nearly one in three by 2040. This significant growth in the elderly population drives the market for medical digital imaging systems, as older individuals require more frequent and advanced medical imaging for the diagnosis and management of age-related health conditions, thus boosting the demand for such technologies.

Technological Advancements: The use of advanced imaging systems in healthcare facilities is fueled by ongoing advancements in imaging technologies, such as artificial intelligence (AI), 3D imaging, and machine learning, which improve diagnostic capabilities and efficiency.

Government Initiatives: The Innovation Santé 2030 plan, part of the France 2030 initiative, aims to position France as the leading European nation in health innovation and sovereignty. This strategy drives the market for medical digital imaging systems by promoting advancements in healthcare technology, fostering research and development, and supporting the adoption of cutting-edge diagnostic tools, thereby enhancing the country's healthcare infrastructure and capabilities.

Market Restraints

High Cost: The initial cost needed to buy and set up state-of-the-art digital imaging systems for medical purposes is high. Smaller healthcare facilities may find this financially prohibitive, which may prevent widespread adoption across the nation.

Regulatory Challenges: Getting through the strict approval procedures and regulations established by the French health authorities may cause a delay in the release of new imaging technologies. For manufacturers, this may lead to uncertainty and increased expenses.

Data Security and Privacy: It can be difficult to guarantee patient data security and privacy in digital imaging systems. Strict data protection laws like (General Data Protection Regulation) GDPR can be difficult and expensive to comply with, which may discourage the use of new technology.

Regulatory Landscape and Reimbursement Scenario

In France, the regulation of medical digital imaging systems is overseen by the Agence Nationale de Sécurité du Médicament et des Produits de Santé (ANSM), which classifies these systems based on their risk profile to determine the appropriate regulatory pathway for approval. Manufacturers must comply with the EU Medical Devices Regulation (MDR), which sets comprehensive safety and performance standards for medical devices across the European Union. Additionally, they must adhere to specific French national legislation that may apply depending on the particular imaging technology being used.

The reimbursement landscape for medical digital imaging in France is robust, primarily funded through the public healthcare system, Sécurité Sociale. The reimbursement process is governed by the Haute Autorité de Santé (HAS), which assesses the clinical value and cost-effectiveness of medical technologies, including imaging systems. This comprehensive system ensures that clinically valuable and cost-effective imaging technologies are accessible to patients through public healthcare coverage.

Competitive Landscape

Key Players

Here are some of the major key players in the France Medical Digital Imaging System Market:

- Siemens Healthineers

- GE Healthcare

- Philips Healthcare

- Canon Medical Systems

- Hitachi Medical

- Fujifilm

- Samsung Medison

- Konica Minolta

- Shimadzu

- Hologic

1. Executive Summary

1.1 Digital Health Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Digital Health Policy in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

France Medical Digital Imaging System Market Segmentation

By Type

- X-Ray

- MRI

- CT scan

- Ultrasound

- Others

By Technology

- 2D Imaging System

- 3D/4D Imaging System

By Application

- Orthopedics

- Oncology

- Cardiology

- Neurology

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Digital Health

Venezuela 3D Imaging Market Analysis

Digital Health

Hong Kong Telemedicine Market Analysis

Digital Health

Belgium Electronic Health Records Market Analysis

Related reports (by geography)

Healthcare Services

France Bone Cancer Diagnostic Market Analysis

Rare Diseases

France Pyruvate Kinase (PK) Deficiency Market Analysis

Rare Diseases

France Glioma Therapeutics Market Analysis

Pharmaceuticals