Pharmaceuticals

France Kyphoplasty Market Analysis

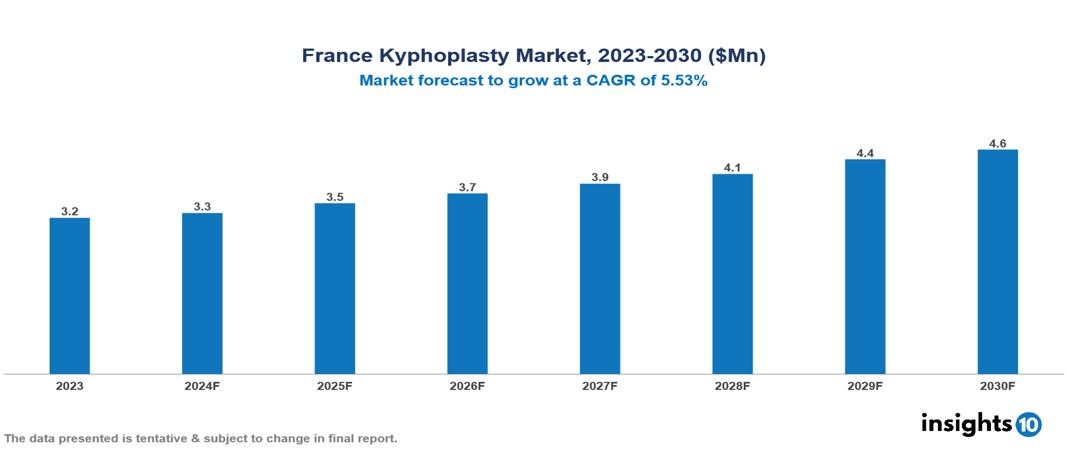

The French kyphoplasty market was valued at $3.2 Mn in 2023 and is predicted to grow at a CAGR of 5.53% from 2023 to 2030, to $4.6 Mn by 2030. The key drivers of the market include the increased prevalence of osteoporosis and spine fractures, continuous technological advancements, kyphoplasty as a superior alternative treatment, and improved patient compliance. The key players of the France kyphoplasty market are IZI Medical, MicroPort Scientific Corporation, Medtronic, Stryker, DePuy Synthes, and Smith & Nephew, among others.

Buy Now

France Kyphoplasty Market Executive Summary

The French kyphoplasty market is at around $3.2 Mn in 2023 and is projected to reach $4.6 Mn in 2030, exhibiting a CAGR of 5.53% during the forecast period.

Kyphoplasty is a minimally invasive surgical procedure that is used to treat painful compression fractures in the spine, resulting from osteoporosis primarily. However, kyphoplasty is also sometimes used to treat fractures caused by spinal tumors or multiple myeloma. In this case, correcting the vertebral deformity and reducing the kyphosis are considered to be the major indications of kyphoplasty. Kyphoplasty is a variant of vertebroplasty that aims to improve its drawbacks. Under local or general anesthesia and with the use of a fluoroscopic guide, polymethylmethacrylate (PMMA) is percutaneously injected into the vertebral body. The distinction from vertebroplasty is that a balloon is inserted percutaneously into the vertebral body and inflated to create space before the PMMA injection in kyphoplasty. The cement hardens, stabilizing the fracture and reducing pain.

The economic burden of both new and old fractures was $7.50 Bn in 2019 (or 2.6% of all national healthcare spending), which increased by $2.29 Bn from $5.21 Bn in 2010. To overcome this economic burden on healthcare, kyphoplasty is being considered as it has proved to be a promising surgical procedure used to treat vertebral compression fractures. The France Kyphoplasty market is therefore driven by significant factors such as prevalence of osteoporosis and spine fractures, continuous technological advancements, kyphoplasty as a superior alternative treatment, and improved patient compliance. However, the high cost of kyphoplasty, the risks and potential complications of kyphoplasty, the restriction of kyphoplasty to certain causes, and the shape of the fracture restrict the growth and potential of the market.

The significant and leading players of the France kyphoplasty market are IZI Medical, MicroPort Scientific Corporation, Medtronic, Stryker, DePuy Synthes, and Smith & Nephew, among others.

Market Dynamics

Market Growth Drivers

Increasing prevalence of Osteoporosis and Spine fractures: Osteoporosis is a major public health challenge globally. According to the International Osteoporosis Foundation (IOF), it is projected that there were 484,000 new fragility fractures in 2019 in France, and that this number will rise to 610,000 fractures in 2034, which is a drastic 26.0% increase. Also, there is a marked difference in the gender-wise prevalence of osteoporosis; women are more prone to risks of osteoporosis. According to IOF the prevalence is among men and women in this country aged 50 and above is 6.9% and 22.7%, respectively. Therefore, these staggering statistics are immensely driving the France kyphoplasty market.

Continuous Technological Advancements: One of the key elements driving market demand is the ongoing technological progress in kyphoplasty modalities. The rate of acceptance of kyphoplasty devices has increased due to the introduction of novel and improved bone tamp designs, cement delivery methods, and navigation technologies. The overall market growth potential has been aided by the increasing integration of advanced imaging technologies, such as fluoroscopy, CT scans, bone densitometers, and intraoperative navigation systems, by healthcare facilities. These technologies improve visualization and guide the placement of instruments, cement injection, and overall surgical accuracy during surgical procedures. As a result, there is an increasing need for kyphoplasty devices, and this is expected to keep the France Kyphoplasty Market growing.

Kyphoplasty as a superior alternative treatment: Kyphoplasty has proved to a better alternative treatment than vertebroplasty by revealing successful outcomes along with a low adverse effect rate. Palliative care has been the conventional therapy for spinal osteoporotic fractures; the patient is advised to rest, provided with analgesics, and assured that the symptoms would ultimately reduce. Thus, the vertebral injury is thought to be relatively irreversible. However, with the discovery of kyphoplasty, these issues have been resolved. Kyphoplasty reduces the risk of cement leakage which is a substantial improvement over vertebroplasty. Moreover, kyphoplasty aims to correct the deformity induced by vertebral fractures in contrast to the current palliative treatments. All in all, kyphoplasty could ideally be used as a curative treatment for vertebral fractures (to prevent kyphosis and its complications and to avoid residual pain), with the end goal being a full recovery without residual vertebral damage. Lastly, kyphoplasty has benefits like increased mobility, better quality of life, and the ability to resume everyday activities in addition to lowering back discomfort. This positive result aids in the market’s expansion.

Improved Patient Compliance: Kyphoplasty provide many benefits over standard surgery, including quicker recovery, shorter hospital stays, less bodily invasion, and better perioperative pain control. Due to these advantages, there is an increasing demand of invasive spine operations over alternative options, which ultimately fuels the expansion of the kyphoplasty market.

Market Restraints

High Cost of Kyphoplasty: The cost of kyphoplasty is a significant restraint which prevents the market from expanding fully. Vertebroplasty is considered an outpatient procedure is usually performed with local anesthesia and conscious sedation, while kyphoplasty is an inpatient procedure which uses general anesthesia and a balloon. Due to this complexity of kyphoplasty accompanied with additional equipment and anesthesia, kyphoplasty is a comparatively expensive treatment than vertebroplasty and could potentially act against the growth of the France Kyphoplasty Market.

Risks and Potential Complications of Kyphoplasty: According to ongoing research, kyphoplasty is a reasonably safe surgical procedure that can help cure kyphosis deformity, relieve compression fracture pain, and restore spinal height. The overall risk of complications from kyphoplasty is less than 1-6% and can include pulmonary embolism, infection, bleeding, and temporary radicular pain. However, from the patient’s perspective even these side effects can be a cause of generating anxiousness and ultimately deter them from obtaining this treatment, which reflects on the overall market.

Restriction of Kyphoplasty to Cause and Shape of fracture: Compared to vertebral fractures caused by cancer, osteoporosis-related vertebral compression fractures usually respond better to kyphoplasty. Often called a wedge fracture, a vertebral compression fracture occurs at the front of the vertebral body and is most usually treated by kyphoplasty. Other fracture types, such crush fractures, in which the entire vertebral body breaks, or biconcave fractures, in which the central part of the vertebral body is compressed but the front and back are intact, are less likely to respond well to kyphoplasty. These two conditions of shape and the cause of fracture thus restrict the scope of kyphoplasty treatment and this eventually leads to a restraint in the Kyphoplasty market.

Regulatory Landscape and Reimbursement Scenario

The main regulatory body for pharmaceuticals in France is the National Agency for the Safety of Medicines and Health Products (ANSM, Agence nationale de sécurité du médicament et des produits de santé in French). The ANSM is a government organization under the Ministry of Health which ensures the security of health products and facilitates access to innovative therapeutics. The ANSM guarantees the safety, efficacy, accessibility, and appropriate usage of health goods that are sold in France through evaluation, knowledge, and monitoring protocols.

The pharmaceutical companies must submit a completed MAA (Marketing Authorization Application) which can be used for drugs meant for the France market (National Procedure) or for the drugs intended for commercialization throughout the European Union (EU) through the EMA (European Medicines Agency). Through the EMA, products can be authorized through the National Procedure, the Centralised Procedure (CP), Decentralised Procedure (DCP) or Mutual Recognition Procedure (MRP). In this case, ANSM acts as a national competent authority (NCA) within the EMA framework. The ANSM then issues a final decision of either approval, conditional approval or refusal after conducting a review and evaluation of the MAA based on safety, efficacy, quality, and risk-benefit ratio.

The National Union of Health Insurance Funds of France (UNCAM, Union Nationale des Caisses d'Assurance Maladie) is the organization which is responsible for France’s public health insurance system. The UNCAM manages the several social security health insurance funds in charge of reimbursing healthcare costs for French nationals and residents. The French Health High Authority evaluates a medicine’s Medical Benefit (Service Médical Rendu, SMR) considering the severity of disease, safety and clinical efficacy, therapeutic innovation. The Committee on Economic Products for Health (CEPS) negotiates with pharmaceutical firms on the cost of medications. Lastly, the Ministry of Health, based on the recommendations of HAS and CEPS, renders the ultimate decision about reimbursement.

Competitive Landscape

Key Players

Here are some of the major key players in the France Kyphoplasty Market:

- IZI Medical

- MicroPort Scientific Corporation

- Medtronic

- Stryker

- DePuy Synthes

- Merit Medical Systems

- Taeyeon Medical Co., Ltd.

- Jiangsu ChangMei Medtech Co., Ltd.

- Smith & Nephew

- Seawon MediTech

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

France Kyphoplasty Market Segmentation

By Product

- Balloon catheters

- Bone access devices

- Cement application products

- Bone cement

- Cement mixing systems

- Instruments

By Indication

- Osteoporosis

- Spinal tumors

- Multiple myeloma

Based on Application

- Spinal fractures

- Kyphosis

- Vertebral alignment restoration

By End-use

- Hospitals and clinics

- Ambulatory surgical centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Egypt Contraceptives Drugs Market Analysis

Pharmaceuticals

US Dialysis Market Analysis

Related reports (by geography)

Rare Diseases

France Ankylosing Spondylitis Drugs Market Analysis

Rare Diseases

France Rett Syndrome Drugs Market Analysis

Pharmaceuticals