Pharmaceuticals

France Cold Pain Therapy Market Analysis

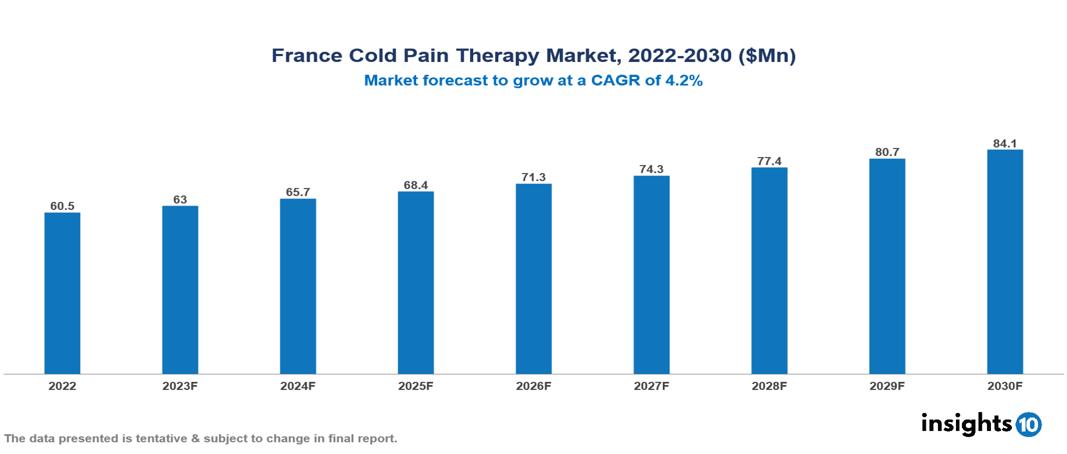

The France Cold Pain Therapy Market was valued at $61 Mn in 2022 and is predicted to grow at a CAGR of 4.2% from 2023 to 2030, to $84 Mn by 2030. The key drivers of this industry include the increasing prevalence of pain disorders, technological advances in the industry, and supportive government initiatives. The industry is primarily dominated by players such as DJO Global, Hisamitsu, Custom Ice, Ossur, Medline, Pfizer, and Performance Health among others.

Buy Now

France Cold Pain Therapy Market Analysis Executive Summary

The France Cold Pain Therapy Market is at around $61 Mn in 2022 and is projected to reach $84 Mn in 2030, exhibiting a CAGR of 4.2% during the forecast period.

Cryotherapy, commonly known as cold pain therapy, is the application of cold substances to alleviate pain by triggering the body's natural anti-inflammatory response and the release of endorphins. This leads to reduced inflammation, swelling, and discomfort, with the primary goal of diminishing neural activity for pain relief. Among the various methods, ice packs stand out as the most widely used form of cold pain therapy due to their affordability, convenience, and drug-free nature. They effectively address pain associated with conditions such as sprains, fractures, strains, tendinitis, and superficial tissue damage. This versatile therapeutic approach applies to acute injuries like sprains and chronic conditions like arthritis and musculoskeletal disorders. Available in various forms, including ice packs, cooling towels, compresses, wraps, pads, and prescription-based motorized and non-motorized devices, cryotherapy is supported by key companies in the market, including Beiersdorf AG, DJO Global, Inc., Hisamitsu Pharmaceutical Co., Inc., Romsons Group of Industries, Polar Products, and Rapid Aid, among others.

The estimated prevalence of chronic pain diseases is about 27% in France. The market is being propelled by factors such as the surge in pain disease prevalence due to the aging population and increased sports activities, technological advances in the industry, and supportive government initiatives. However, conditions such as strong consumer preference for traditional pain relief medications, affordability challenges, and limited accessibility restrict the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increase in prevalence of pain disorders: France is experiencing an increase in its aging population, making it more prone to chronic pain issues such as arthritis, muscle pain, and sports injuries. More than 27% of the French population is affected by chronic pain disorders creating a huge patient pool requiring treatment. Other factors such as sports and active lifestyle result in a greater prevalence of sports-related injuries requiring effective pain management strategies driving up the demand for cold pain therapy for recovery and rehabilitation.

Technological advances: Manufacturers continue to innovate by introducing new cold therapy equipment with greater features, mobility, and user-friendliness. These technologies include wearable cold therapy wraps, accurate cold compression systems, and cryotherapy chambers. The emphasis is on providing targeted and localized pain relief, with evolving technology allowing for more precise and focused cold treatment delivery, hence increasing effectiveness and reducing potential adverse effects.

Supportive government policies: The French government prioritizes healthcare innovation, including research focused on pain management. This assistance results in increased funding for the study and development of new cold therapy technologies. Government initiatives to promote non-pharmaceutical pain management approaches can encourage medical providers to adopt cold therapy solutions, resulting in rapid market growth.

Market Restraints

Strong consumer preference for pharmaceutical pain relief: OTC analgesics such as paracetamol, aspirin, and ibuprofen are cost-effective alternatives that enjoy consumer preference. The financial barrier and limited awareness regarding the benefits of cold pain therapy can impede market growth.

Affordability challenges: Cold pain therapy is an expensive option compared to cheaper and quick-relief OTC medications which can create a financial barrier for a certain section of the population. No insurance coverage for these therapies also limits their widespread adoption in patients seeking long-term treatment for chronic pain.

Limited accessibility: Particularly in rural areas, patients have limited access to specialized providers or physiotherapists adept with cold pain therapy. This results in discrepancies in available treatment alternatives. Cold therapy procedures can be difficult to employ in smaller healthcare facilities that raise infrastructural challenges.

Notable Updates

June 2022, Axomove, a France-based startup, raised $1.7 Mn for its digital health platform. The company assists in remote patient tracking and compliance with self-rehabilitation exercises in physiotherapy.

Healthcare Policies and Regulatory Landscape

The main regulatory body overseeing drugs and pharmaceuticals in France is the Agence Nationale de Sécurité du Médicament et des Produits de Santé (ANSM), translated as the National Agency for the Safety of Medicines and Health Products. ANSM plays a crucial role in ensuring the safety, efficacy, and quality of medicinal products in the country. The agency collaborates with other European regulatory bodies to maintain consistency with European Medicines Agency (EMA) standards, facilitating the integration of French pharmaceuticals into the broader European market.

The process of obtaining licensure for drugs in France typically involves the submission of a comprehensive application dossier by pharmaceutical companies to ANSM. ANSM reviews the submission, and if the product meets regulatory requirements, it grants marketing authorization.

For new entrants, navigating the regulatory environment involves understanding and complying with ANSM's guidelines, adhering to European Union regulations, and conducting thorough and rigorous testing and documentation to demonstrate the safety and efficacy of their pharmaceutical products. The regulatory landscape aims to ensure public health and maintain high standards within the pharmaceutical industry in France.

Competitive Landscape

Key Players

- Beiersdorf AG

- Breg

- Custom Ice

- DJO Global Inc

- Hisamitsu Pharmaceutical

- Johnson & Johnson

- Medline Industries

- Ossur

- Pfizer

- Performance Health

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cold Pain Therapy Market Segmentation

By Therapy Type

- Icepack

- Chamber

- Cryosurgery

By Product Type

- OTC Products

- Prescription Drugs

By Application

- Dermatology

- Oncology

- Musculoskeletal disorders

- Pain management

- Sports medicine

- Ophthalmology

- Others

By End Users

- Hospitals and clinics

- Sports person

- Adults

- Others

By Distribution channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Mexico Tetanus Toxoid Vaccine Market Analysis

Pharmaceuticals

Saudi Arabia Type 2 Diabetes Mellitus Drugs Market Analysis

Pharmaceuticals

Indonesia Endometriosis Drugs Market Analysis

Related reports (by geography)

Healthcare Services

France Radiology Service Market Analysis

Pharmaceuticals

France Type 2 Diabetes Mellitus Drugs Market Analysis

Pharmaceuticals

France Brain Cancer Therapeutics Market

Pharmaceuticals