Medical Devices

France Cardiac Surgery Instruments Market Analysis

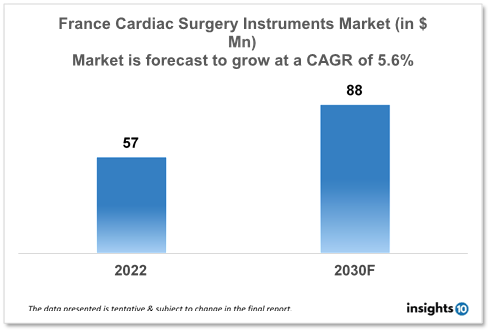

The France Cardiac Surgery Instruments Market is expected to witness growth from $57 Mn in 2022 to $88 Mn in 2030 with a CAGR of 5.60% for the forecasted year 2022-2030. The market for heart surgical devices in France is expanding as less invasive techniques become more popular. Because they are less intrusive, these procedures have quicker recovery periods and fewer complications, which is encouraging both patients and healthcare professionals to use them more frequently. The market is segmented by type, application and by end user. Some key players in this market include Delacroix-Chevalier, Marquat, LivaNova, B. Braun, Medline Industries, KLS Martin, and STILLE.

Buy Now

France Cardiac Surgery Instruments Healthcare Market Executive Analysis

The France Cardiac Surgery Instruments Market size is at around $57 Mn in 2022 and is projected to reach $88 Mn in 2030, exhibiting a CAGR of 5.60 % during the forecast period. In France, healthcare costs amount to 12.3% of GDP, or $5,370 per individual. The population of France is anticipated to increase by 0.36% in 2024. In France, men can anticipate living 79.53 years on average, compared to 85.79 years for women. France spent $5,370 on healthcare in 2022, a decrease of 3.56% from the year before. In France, personal expenditures make up 9.26% of healthcare spending.

Cardiovascular diseases are a serious public health concern in France. With about 150,000 fatalities per year, cardiovascular disease (CVD) is the leading cause of mortality in France. About 3.5 million people in France suffer from heart disease. Heart attacks, also known as acute myocardial infarction (AMI), occur in about 60,000 people in France each year. 18 million people in France, or about 30% of the population, are believed to have hypertension. In the general population, atrial fibrillation, a common arrhythmia, impacts between 600,000 and 1.2 million people. 100,000 new instances of coronary artery disease (CAD), which can result in heart attacks and other cardiovascular problems, are reported each year in France.

In France, cardiac surgical equipment is used in a variety of contexts for the diagnosis, treatment, and management of cardiovascular disorders. The surgical procedure known as coronary artery bypass graft surgery (CABG) is frequently used to treat coronary artery disease because it reroutes blood flow around obstructed or constrained arteries. In the course of the procedure, tools used in cardiac surgery include surgical scissors, forceps, clamps, and sutures. Surgery to replace or repair damaged or dysfunctional heart valves is known as valve repair or replacement surgery. During the process, cardiac surgical tools such as retractors, clamps, scissors, and sutures are employed. Several diagnostic techniques, including cardiac catheterization, angiography, and electrophysiology investigations, also involve devices from cardiac surgery. These methods aid in the diagnosis of cardiovascular disorders, assess their severity, and direct therapy choices.

Market Dynamics

Market Growth Drivers

The market for cardiac surgery devices in France is expanding as less invasive techniques become more popular. Because they are less intrusive, these procedures have quicker recovery periods and fewer complications, which is encouraging both patients and healthcare professionals to use them more frequently. The demand for equipment for cardiac surgery in the French healthcare industry is being driven by the rising prevalence of cardiovascular disorders like heart failure, coronary artery disease, and arrhythmias. The prevalence of these diseases is anticipated to increase as the population ages and lifestyles become more sedentary, which will propel market expansion in the French healthcare sector. The market for cardiac surgery tools in France is expanding as a result of the rising demand for surgical treatments, especially cardiovascular surgeries. Patients are looking for surgical solutions to enhance their health outcomes as they become more aware of the hazards linked to cardiovascular illnesses. It causes the market for cardiac surgery instruments in the French healthcare industry to grow.

Market Restraints

The French healthcare market may offer effective alternatives to heart surgery, such as alternative medicines like pharmacological therapies or non-invasive procedures. The availability of these substitutes may prevent France's healthcare industry from adopting heart surgery tools. In France, the high price of heart surgery equipment may prevent some healthcare facilities from using it. Hospitals could be cautious to spend money on pricey equipment, especially if it isn't something that will be utilised regularly.

Competitive Landscape

Key Players

- Delacroix-Chevalier (FR)

- Marquat (FR)

- LivaNova

- B. Braun

- KLS Martin

- Medline Industries

- STILLE

Recent Notable deals

2021: A French business engaged in cardiac surgery with a business in Spain, Medicrea International, was successfully acquired by Medtronic. The purchase broadens Medtronic's offering of products and services for cardiac surgery.

Healthcare Policies and Regulatory Landscape

The regulatory environment and healthcare policies in France have a significant impact on the market for cardiac surgery tools. All medical devices, including tools used in cardiac surgery, that are sold in the European Union (EU), including France, must comply with the European Medical Devices Regulation (MDR), a new set of laws that went into effect in 2021. Manufacturers must abide by the new rules in order to market their goods in the EU. The MDR seeks to strengthen the safety and performance requirements for the cardiac surgery instruments market. An autonomous public agency called the French National Authority for Health (HAS) is in charge of evaluating the efficacy, cost-effectiveness, and safety of tools used in cardiac surgery. Before putting their goods on the French market, manufacturers must submit their products for HAS review and clearance.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiac Surgery Instruments Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into segments in this study based on the goods, applications, end users, and geographical areas. The market is divided into forceps, scissors, needle holders, clamps, and other cardiac surgery instruments based on the product. In 2017 the forceps category led the market, and it is anticipated that it will increase at the fastest rate going forward. The rise in heart surgeries and the frequent usage of forceps in most cardiac procedures are credited with the segment's strong growth.

- Forceps

- Vascular Forceps

- Grasping Forceps

- Other Forceps

- Needle Holders

- Scissors

- Clamps

- Other Cardiac Surgical Instruments

By Application (Revenue, USD Billion):

The market is further segmented by application into paediatric cardiac surgery, heart valve surgery, coronary artery bypass graft (CABG), and other applications. The France market's largest and fastest-growing application segment is CABG. This is mostly explained by the increased prevalence of heart illnesses and the consequent rise in surgical treatments. The second-largest category is heart valve surgery.

- Coronary Artery Bypass Graft (CABG)

- Heart Valve Surgery

- Pediatric Cardiac Surgery

- Other Applications

By End User (Revenue, USD Billion):

Based on the end user, the market is segmented into hospitals and cardiac centers, and ambulatory surgery centers. The hospitals and cardiac centers segment is expected to dominate the market for cardiac surgery instruments. Growth in this end-user segment can be attributed to the increasing incidence of cardiac and heart valve diseases and the subsequent increase in the number of cardiac surgery procedures.

- Hospitals and Cardiac Centers

- Ambulatory Surgery Centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Kenya ECG Equipments Market Analysis

Medical Devices

Venezuela Neurology Devices Market Analysis

Medical Devices

Kenya Hemodialysis Vascular Grafts Market Analysis

Related reports (by geography)

Pharmaceuticals

France Clinical Nutrition for Cancer Care Market Analysis

Pharmaceuticals

France Enzymatic Wound Debridement Market Analysis

Rare Diseases

France Optic Neuritis Therapeutics Market Analysis

Pharmaceuticals