Medical Devices

France Biomaterials in Healthcare Market Analysis

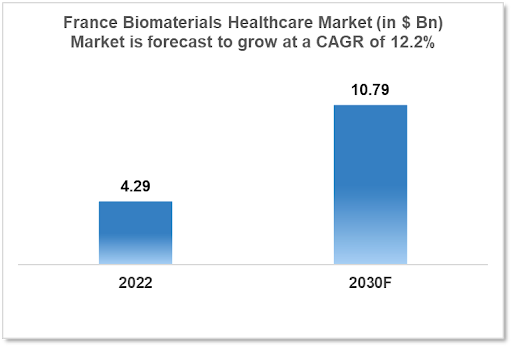

The France Biomaterials Healthcare Market is expected to witness growth from $4.29 Bn in 2022 to $10.79 Bn in 2030 with a CAGR of 12.20% for the forecasted year 2022-2030. In France, there is a rising demand for minimally invasive procedures that use speciality biomaterials. Manufacturers who can create products that work with minimally invasive procedures have an edge over rivals in the market. The demand for biomaterials used in orthopaedics, cardiology, and other medical uses is rising in France as a result of the country's ageing population. The market is segmented by type and by application. Some key players in this market include Sofradim Production, Arthrex France, Carthera, BASF SE, Evonik Industries and Medtronic.

Buy Now

France Biomaterials in Healthcare Market Executive Analysis

The France Biomaterials Healthcare Market size is at around $4.29 Bn in 2022 and is projected to reach $10.79 Bn in 2030, exhibiting a CAGR of 12.20% during the forecast period. In France, healthcare costs were 12.3% of GDP or $5,370 per person. In 2023, a rise in France's population of 0.36% is predicted. Men can anticipate living 79.53 years in Germany, while women can anticipate 85.79 years. In France, healthcare spending in 2022 was $5,370, which was a fall of 3.56% from 2020. Out-of-pocket costs account for 9.26% of total health expenditures.

In France, Numerous facets of therapeutic and preventive healthcare are being transformed by biomaterials. They already have a significant impact on the creation of novel medical devices, prostheses, tissue repair and replacement technologies, drug transport systems, and diagnostic methods. Biomaterials are the subject of significant study efforts in France because they have enormous potential to improve the quality of life for everyone. A multidisciplinary strategy is necessary for this field's advancement, involving interactions between scientists (including chemists, biologists, and medical professionals) and material suppliers, and manufacturers. The STREP 3G-SCAFF is investigating the potential of engineering both materials and cells to create the third generation of designed biomaterials in addition to developing techniques for the creation of functional biomaterials for tissues derived from either human or animal tissue. One of these is an extracellular matrix (ECM)/bioresorbable intelligent polymer composite with a bioactive structure that can trigger particular cells.

Market Dynamics

Market Growth Drivers

In France, there is a rising demand for minimally invasive procedures that use speciality biomaterials. Manufacturers who can create products that work with minimally invasive procedures have an edge over rivals in the market. The demand for biomaterials used in orthopaedics, cardiology, and other medical uses is rising in France as a result of the country's ageing population. Older people who want to keep their mobility and quality of life are in high demand for biomaterials like bone substitutes and joint replacements. Significant advances in biocompatibility, durability, and functionality have been made in the creation of biomaterials. Manufacturers with a competitive edge in the France healthcare market are those who can innovate and create new materials and uses. The French government has put in place several laws and programmes, such as tax breaks and funding for R&D, to encourage the use of biomaterials in healthcare. The healthcare industry for biomaterials in France is expanding as a result of these policies.

Market Restraints

The French biomaterials healthcare market is extremely competitive, with both domestic and foreign producers vying for market share. By creating top-notch goods, giving creative solutions, and offering top-notch customer support, manufacturers can set themselves apart from the competition. The French healthcare system is under pressure to cut expenses, which may prevent the acceptance of novel and cutting-edge biomaterials. Manufacturers must strike a compromise between the need to create economical solutions and the need to uphold strict quality and safety standards. It might be challenging for manufacturers to innovate and create new goods in France due to the country's limited funding for biomaterials research and development. To support their R&D efforts, manufacturers must look into joint ventures with research institutions and look for financing from other sources.

Competitive Landscape

Key Players

- Sofradim Production (FR)

- Arthrex France (FR)

- Carthera (FR)

- BASF SE

- Celanese

- Covestro AG

- Medtronic

Notable Recent Deals

2021: In 2021, Pancakes Partners led a $9.62 Mn funding round for the French biomaterials startup Carthera. For the purpose of enhancing the treatment of cancer and other diseases, the business is creating a new class of ultrasound-based medical devices.

Healthcare Policies and Regulatory Landscape

The safety and effectiveness of Biomaterials, are governed by the French National Agency for Medicines and Health Products Safety. The clinical trial clearance procedure, post-market monitoring, and adherence to safety and quality standards are all under the control of the French National Agency for Medicines and Health Products Safety. All medical devices sold in the EU, including biomaterials, must comply with the Medical Devices Regulation (MDR), which went into force in May 2021. A stricter standard for clinical evidence, product labelling, and post-market surveillance is introduced by the Medical Devices Directive (MDR), which replaces the earlier Medical Devices Directive (MDD). The national health insurance programme that covers the expense of healthcare services and supplies for patients is the main source of funding for the French healthcare system. The pricing and reimbursement of goods made from biomaterials may be impacted by the French government's price negotiations with pharmaceutical and medical device firms.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Biomaterials in Healthcare Market Segmentation

By Type (Revenue, USD Billion):

Based on type, the market is segmented into Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, and Natural Biomaterials. The Metallic Biomaterials segment accounted for the largest share of the France market in 2019. The growing geriatric population Francely is expected to drive growth for this segment.

- Metallic Biomaterials

- Stainless Steel

- Titanium & Titanium Alloys

- Cobalt-Chrome Alloys

- Gold

- Silver

- Magnesium

- Polymeric Biomaterials

- Polymethylmethacrylate

- Polyethylene

- Polyester

- Silicone Rubber

- Nylon

- Polyetheretherketone

- Other Polymeric Biomaterials

- Ceramics

- Calcium Phosphate

- Zirconia

- Aluminum Oxide

- Calcium Sulfate

- Carbon

- Glass

- Natural Biomaterials

- Hyaluronic Acid

- Collagen

- Gelatin

- Fibrin

- Cellulose

- Chitin

- Alginates

- Silk

By Application (Revenue, USD Billion):

The cardiovascular, orthopaedic, dental, plastic surgery, wound healing, tissue engineering, ophthalmology, neurological/CNS, and other applications segments are made up of the biomaterials market. The market category for wound healing is anticipated to have the highest CAGR in 2019. The market will increase as a result of factors including expanding healthcare infrastructure, a large population pool, a rising diabetic population, and rising healthcare spending. Surgical Guides

- Cardiovascular

- Catheters

- Stents

- Implantable Cardiac Defibrillators

- Pacemakers

- Sensors

- Heart Valves

- Vascular Grafts

- Guidewires

- Others

- Orthopedic

- Joint Replacement

- Knee Replacement

- Hip Replacement

- Shoulder Replacement

- Others

- Viscosupplementation

- Bioresorbable Tissue Fixation

- Spine?

- Spinal Fusion Surgeries

- Minimally Invasive Fusion Surgeries

- Motion Preservation & Dynamic Stabilization Surgeries

- Pedicle-Based Rod Systems

- Interspinous Spacers

- Artificial Discs

- Fracture Fixation Devices

- Bone Plates

- Screws

- Pins

- Rods

- Wires

- Synthetics Bone Grafts

- Joint Replacement

- Ophthalmology

- Contact Lenses

- Intraocular Lenses

- Functional Replacement of Ocular Tissues

- Synthetic Corneas

- Others

- Contact Lenses

- Dental

- Dental Implants

- Dental Bone Grafts & Substitutes

- Dental Membranes

- Tissue Regeneration

- Plastic Surgery

- Soft-Tissue Fillers

- Craniofacial Surgery

- Wound Healing

- Wound Closure Devices

- Sutures

- Staples

- Surgical Hemostats

- Internal Tissue Sealants

- Adhesion Barriers

- Hernia Meshes

- Wound Closure Devices

- Tissue Engineering

- Scaffolds for Regenerative Medicine

- Nanomaterials for Biosensing

- Tailoring of Inorganic Nanoparticles

?

- Neurological/Central Nervous System Applications

- Shunting Systems

- Cortical Neural Prosthetics

- Hydrogel Scaffolds for CNS Repair

- Neural Stem Cell Encapsulation

?

- Other Applications

- Drug Delivery Systems

- Gastrointestinal Applications

- Bariatric Surgery

- Urinary Applications

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Russia Pain Management Devices Market Analysis

Medical Devices

Mexico ENT Devices Market Analysis

Medical Devices

Brazil Biomaterials in Healthcare Market Analysis

Related reports (by geography)

Rare Diseases

France Hunter Syndrome Therapeutics Market Analysis

Pharmaceuticals

France Antibacterial (Antibiotics) Drugs Market Analysis

Pharmaceuticals

France Compounding Pharmacies Market Analysis

Pharmaceuticals