Egypt Teleradiology Market Analysis

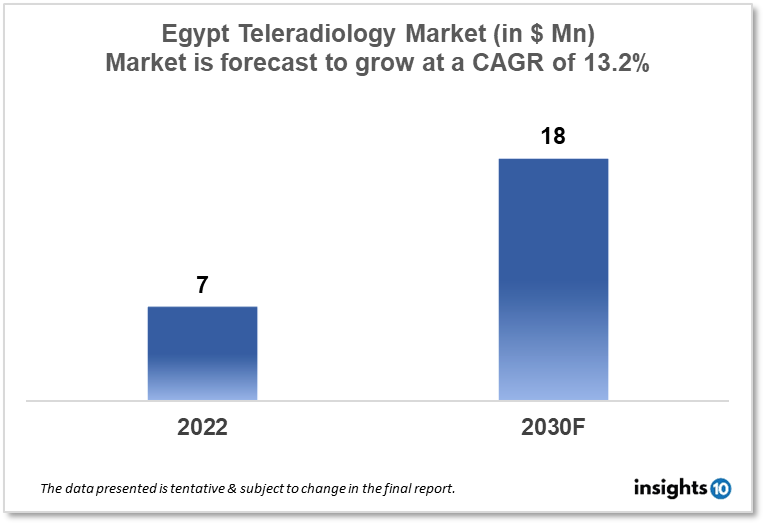

The Egypt Teleradiology market size was valued at $7 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 13.2% from 2022 to 2030 and will reach $ 18 Mn in 2030. The market is segmented by application, modality, technology solutions, and end user. The Egypt teleradiology market will grow due to advancements in technology, such as electronic medical records (EMRs) and picture archiving and communication systems (PACS), have made it easier to transmit and store medical images securely. The key market players are Alborg Laboratories & Radiology Services, Alfa Labs, Cairo Scan Radiology & Labs, Egypt Radiology Group, Ebtisama Radiology, MedMark Teleradiology, Mena Medical Solutions, Radiology Group, Telemedica Egypt and others.

Buy Now

Egypt Teleradiology Market Executive Summary

The Egypt Teleradiology market size was valued at $7 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 13.2% from 2022 to 2030 and will reach $ 18 Mn in 2030. Egypt's healthcare expenditure has been increasing steadily in recent years. According to the World Bank, healthcare expenditure in Egypt was 4.7% of the country's GDP in 2018. The government has also been investing in digital health initiatives to improve healthcare delivery and access.

Teleradiology is a branch of telemedicine that involves the transmission of radiological images and patient data from one location to another for the purpose of remote interpretation or consultation. In Egypt, teleradiology is becoming more popular as a way to improve access to radiology services in remote or underserved areas, as well as to reduce waiting times and improve the accuracy and speed of diagnoses.

Trends in teleradiology in Egypt include the use of artificial intelligence (AI) and machine learning algorithms to assist radiologists in interpreting images, as well as the use of mobile teleradiology units to provide services in areas without access to traditional radiology facilities. Additionally, teleradiology is being used to support medical tourism in Egypt by providing remote interpretation services for foreign patients. Teleradiology is expected to continue to grow in Egypt as the country continues to invest in digital health technologies and infrastructure. This will help to improve healthcare access and quality, particularly in remote or underserved areas.

Market Dynamics

Market Growth Drivers

- Improved access to radiology services: Teleradiology allows patients in remote or underserved areas to access radiology services without the need to travel to a radiology facility, which can be particularly beneficial in a country like Egypt with a large rural population.

- Reduction in waiting times: Teleradiology can help to reduce waiting times for radiology services by enabling faster image interpretation and diagnosis.

- Improved accuracy and speed of diagnoses: Teleradiology can facilitate remote consultation and collaboration among radiologists, which can lead to more accurate and faster diagnoses.

- Growing demand for healthcare services: The demand for healthcare services in Egypt is growing rapidly due to the country's increasing population and aging demographic, which is driving demand for teleradiology services.

Market Restraints:

- Limited internet infrastructure: The availability and quality of internet infrastructure in Egypt can be a challenge, particularly in remote areas, which can impact the ability to transmit and interpret radiology images remotely.

- Lack of regulatory framework: The lack of a clear regulatory framework for teleradiology in Egypt can lead to issues around data privacy and security, as well as quality assurance.

- Cost: The cost of teleradiology services can be a barrier to adoption for some patients and healthcare providers, particularly those in rural or underserved areas.

Competitive Landscape

Key Players

- Alborg Laboratories & Radiology Services

- Alfa Labs

- Cairo Scan Radiology & Labs

- Egypt Radiology Group

- Ebtisama Radiology

- MedMark Teleradiology

- Mena Medical Solutions

- RADSpa TeleRadiology Solutions

- Radiology Group

- Telemedica Egypt

Healthcare Policies and Regulatory Landscape

Teleradiology in Egypt is subject to regulatory oversight by the Ministry of Health and Population. There are currently no specific laws or regulations governing teleradiology in Egypt, although existing laws and regulations related to medical practice and data privacy are generally applicable.

In practice, teleradiology providers are expected to comply with relevant standards and guidelines related to medical practice, including those related to quality assurance, data privacy, and security. This may include following standards established by the International Organization for Standardization (ISO) or other relevant bodies.

Additionally, healthcare providers and teleradiology companies may need to obtain appropriate licenses or permits from relevant authorities in order to operate in Egypt. For example, healthcare facilities may need to obtain a license from the Ministry of Health and Population, while teleradiology providers may need to obtain a permit from the Egyptian Radio and Television Union.

Teleradiology Market Segmentation

By Application

- Picture Archiving and Communication System (PACS)

- Radiology Information System (RIS)

By Modality:

The market is divided into X-ray, computed tomography (CT), ultrasound, magnetic resonance imaging (MRI), nuclear imaging, fluoroscopy, and mammography segments based on Modality. The computed tomography market category held the biggest market share in 2020. Several medical specialties employ computed tomography, including cardiology, cancer, neurology, abdominal and pelvic imaging, as well as spine and musculoskeletal imaging. The teleradiology market is expanding in this sector due to factors including the rising demand for early and accurate diagnosis, technical improvements, and digitalization in this industry. Around 100 million CT scans are performed annually worldwide, according to the WHO. The demand for CT scans over other imaging modalities has increased due to the desire to avoid exploratory procedures and advancements in cancer diagnosis and therapy.

- X-Ray

- Magnetic Resonance Imaging

- Computed Tomography

- Ultrasound Systems

- Nuclear Imaging

By Technology Solutions

- Web-Based Teleradiology Solutions

- Cloud-Based Teleradiology Solutions

By End User

The market is divided into four categories based on the end users: long-term care facilities, nursing homes, and assisted living facilities; hospitals and clinics; diagnostic imaging centres and laboratories; and other end users. In 2019, the hospitals and clinics segment's revenue contribution was the highest. This segment's significant market share can be ascribed to the increase in diagnostic imaging operations carried out in hospitals, the hospitals' growing propensity to automate and digitise patient data, and the growing demand to raise the standard of patient care. In addition, the COVID-19 pandemic shortage of radiologists and the growing usage of new imaging modalities to boost hospital workflow efficiency are anticipated to enhance the development of this end-user segment.

- Hospitals and Clinics

- Diagnostic Imaging Center and Laboratories

- Long-term Care Centres, Nursing Homes, Assisted Living Facilities

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Related reports (by geography)

India Breast Pump Market Report