Healthcare Services

Egypt Genomic Diagnostics Market Analysis

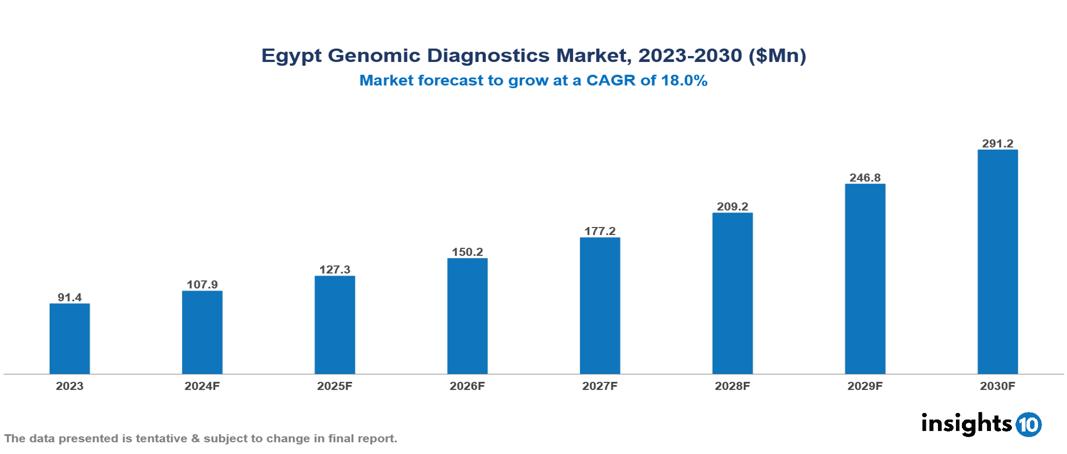

Egypt Genomic Diagnostics Market was valued at $91.42 Mn in 2023 and is predicted to grow at a CAGR of 18% from 2023 to 2030, to $291.22 Mn by 2030. The key drivers of this industry include Growing Healthcare Expenditure, Advancements in Technology, and Government Initiatives. The industry is primarily dominated by Illumina, 23andMe, Myriad Genetics, and Amgen among others.

Buy Now

Egypt Genomic Diagnostics Market Executive Summary

Egypt Genomic Diagnostics Market was valued at $91.42 Mn in 2023 and is predicted to grow at a CAGR of 18% from 2023 to 2030, to $291.22 Mn by 2030.

Genomic diagnostics is a rapidly evolving field that uses an individual's genetic information to diagnose diseases, assess predisposition to future health problems, and guide treatment plans by analyzing DNA or RNA for disease-linked variations. This includes karyotyping to examine chromosome abnormalities, targeted mutation analysis for specific disease-related genes, and next-generation sequencing (NGS) for a comprehensive genetic analysis. Applications encompass disease diagnosis, carrier testing for informed family planning, predictive testing for disease risk assessment, and pharmacogenomics for personalized medication treatments. The benefits of genomic diagnostics include early disease detection, personalized medicine, and improved disease management and prognosis.

Chronic diseases significantly impact Egypt's elderly, with cardiovascular disease, chronic respiratory illness, and diabetes accounting for 82% of global chronic disease-related deaths, many premature in 2022. Non-communicable diseases (NCDs) cause 41% of deaths in Egypt, particularly hypertension, diabetes, and cardiovascular disease among the elderly. The elderly population, projected to rise from 6% in 1996 to 10.9% by 2026, faces healthcare access challenges (96%), high depression rates (89%), and low awareness of healthy lifestyles (65%). Egypt's healthcare system has 141,000 hospital beds, with 3856 for the elderly, and ongoing policy initiatives aim to improve geriatric care and preventive services. Additionally, the AL-SEHA study, launched in 2024, will analyze 20,000 respondents over 50 to better understand healthy aging and climate change impacts.

Market is therefore driven by significant factors like Growing Healthcare Expenditure, Advancements in Technology, and Government Initiatives. However, limited healthcare infrastructure, reimbursement issues, and limited access to healthcare services restrict the growth and potential of the market.

A prominent player in this field is Illumina, which has partnered with AstraZeneca to leverage genomics and AI for faster drug development by identifying new therapeutic targets and biomarkers, 23andMe acquired Lemonaid Health to enhance its personalized healthcare offerings through telehealth and prescription drug delivery services based on genetic information. Other contributors include Myriad Genetics, and Amgen among others.

Market Dynamics

Market Growth Drivers

Growing Healthcare Expenditure: The expected surge in healthcare expenditure in Egypt is likely to drive demand for diagnostic services, including genomics diagnostics. In 2022, Egypt's Governmental Health Expenditure (GHE) accounted for approximately one-third of the Total Health Expenditure (THE), fluctuating between 24.8% and 50%. Increased demand for healthcare services is anticipated as a result.

Advancements in Technology: Technological advancements have led to the development of more complex and accurate diagnostic tests, crucial for effectively diagnosing and managing diseases. These advancements have resulted in better patient outcomes and lower healthcare costs, making advanced diagnostics more accessible and effective.

Government Initiatives: The Universal Health Insurance System (UHIS), launched in 2018, aims to provide comprehensive health coverage to all citizens. This initiative is expected to drive demand for clinical diagnostics services and improve access to healthcare across the country, enhancing overall healthcare quality.

Market Restraints

Limited Healthcare Infrastructure: Despite increasing healthcare expenditure, Egypt's healthcare infrastructure remains limited in many areas. This limitation can hinder the adoption of advanced diagnostic technologies, including genomics diagnostics, especially in underdeveloped regions.

Reimbursement Issues: The majority of diagnostic tests are paid for out-of-pocket by patients, as the reimbursement scenario for clinical diagnostics in Egypt is still developing. This can limit the adoption of advanced diagnostic services, making them less accessible to a broader population.

Limited Access to Healthcare Services: Significant disparities in access to healthcare services exist, particularly in rural areas. These geographical disparities can reduce the effectiveness of diagnostic services, including genomics diagnostics, in reaching the entire population and providing equitable healthcare access.

Regulatory Landscape and Reimbursement Scenario

Egypt's healthcare sector is evolving, particularly in the field of genomics, under the oversight of the Egyptian Drug Authority (EDA). The EDA is responsible for regulating pharmaceuticals, medical devices, and healthcare products, ensuring the safety and efficacy of new genomic tests before approval.

Reimbursement for genomic diagnostics in Egypt involves various factors. The Egyptian Ministry of Health, as the primary healthcare provider, plays a key role in establishing reimbursement policies for genomic tests. The private health insurance sector in Egypt is expanding, offering varying levels of coverage for these tests. However, a significant portion of the population still relies on out-of-pocket payments for healthcare, including genomic diagnostics, posing financial challenges for many patients.

Competitive Landscape

Key Players

Here are some of the major key players in the Egypt Genomic Diagnostics

- Illumina, Inc.

- Myriad Genetics, Inc.

- Amgen, Inc.

- 23andMe

- Agilent Technologies

- Perkin Elmer

- Thermo Fisher Scientific

- Eurofins Scientific

- Bio-Rad Laboratories, Inc.

- Danaher Corporation

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Genomic Diagnostics Market Segmentation

By Technology

- Next Generation Sequencing

- Array Technology

- PCR-based Testing

- FISH

- Others

By Application

- Ancestry & Ethnicity

- Traits Screening

- Genetic Disease Carrier Status

- New Baby Screening

- Health and Wellness-Predisposition/Risk/Tendency

By Product

- Consumables

- Equipment

- Software & Services

By End-user

- Hospitals & Clinics

- Diagnostic Laboratories

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Algeria Healthcare Diagnostics Market Analysis

Healthcare Services

Algeria Clinical Diagnostics Market Analysis

Healthcare Services

Brazil Robotic Surgery Services Market Analysis

Related reports (by geography)

Pharmaceuticals

Egypt Colposcopy Market Analysis

Clinical Trials

Egypt Clinical Trials Support Service Market Analysis

Pharmaceuticals

Egypt Interstitial Cystitis Drugs Market Analysis

Pharmaceuticals