Pharmaceuticals

Egypt Clinical Nutrition for Cancer Care Market Analysis

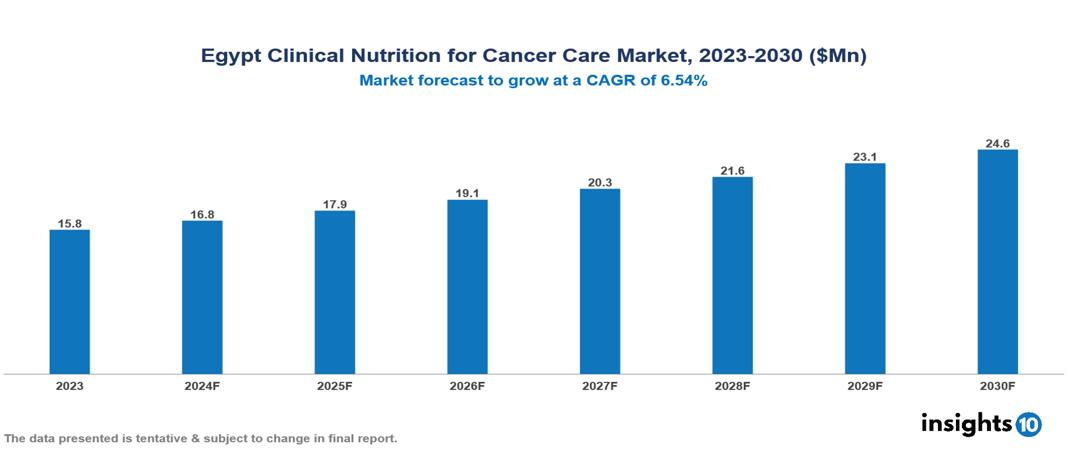

The Egypt Clinical Nutrition for Cancer Care Market was valued at $15.8 Mn in 2023 and is predicted to grow at a CAGR of 6.54% from 2023 to 2030, to $24.6 Mn by 2030. The key drivers of the market include the increasing prevalence of cancer, improved healthcare infrastructure, and rising disposable incomes. The prominent players of the Egypt Clinical Nutrition for Cancer Care Market are Fresenius Kabi, Otsuka, and Egyptian Society of Nutrition and Food Science (ESNFS), among others.

Buy Now

Egypt Clinical Nutrition for Cancer Care Market Executive Summary

The Egypt Clinical Nutrition for Cancer Care Market was valued at $15.8 Mn in 2023 and is predicted to grow at a CAGR of 6.54% from 2023 to 2030, to $24.6 Mn by 2030.

Clinical nutrition for cancer care is a specialized field focusing on providing optimal nutritional support to patients throughout their cancer journey. It goes beyond simply “eating healthy” and involves a personalized approach to address the unique nutritional needs of each patient. A registered dietitian or other qualified healthcare professional usually assess the patient’s nutritional status. Based on the assessment, a personalized plan is created to meet the patient’s individual needs. Nutritional deficiencies are prevalent among cancer patients due to treatment side effects, altered metabolism, and decreased appetite. Clinical nutrition interventions play a crucial role in improving treatment tolerance as adequate nutrition can help patients tolerate chemotherapy and radiation therapy better, potentially reducing side effects and allowing for completion of treatment plans. Also, it maintains strength and immunity as proper nutrition helps patients maintain muscle mass, fight infections, and recover faster from surgery. Lastly, it enhances the quality of life since nutritional support can improve fatigue, appetite, and overall well-being, leading to a better quality of life during cancer treatment.

Advancements in medical nutrition therapy have led to the development of specialized oral nutritional supplements (ONS) and enteral feeding formulas. These products provide concentrated nutrients and can be crucial for patients struggling to meet their nutritional needs through regular diet alone. Parenteral nutrition remains an option for patients unable to tolerate oral or enteral feeding. Overall, clinical nutrition for cancer care plays a vital role in optimizing patient outcomes by ensuring they receive the necessary nutrients to support their body throughout treatment.

The Egypt Clinical Nutrition for Cancer Care Market is driven by significant factors such as the increasing prevalence of cancer, improved healthcare infrastructure, and rising disposable incomes. However, reimbursement policies, limited awareness, and challenges in implementation restrict the growth and potential of the market.

The prominent players of the Egypt Clinical Nutrition for Cancer Care Market are Fresenius Kabi, Abbott Nutrition, Baxter International, Otsuka, and Egyptian Society of Nutrition and Food Science (ESNFS), among others. Otsuka Egypt is a branch of the larger Otsuka Pharmaceutical Company focusing on the Egyptian market. Although Otsuka Egypt has a broader focus on pharmaceutical products and hospital solutions, their "Clinical Nutrition and Hospital Solutions" section encompasses enteral nutrition products used in clinical settings.

Market Dynamics

Market Growth Drivers

Increasing Prevalence of Cancer: A major driver for this market is the increasing global burden of cancer and the high mortality rates associated with it. As the population ages and lifestyle risks like smoking persist, the number of new cancer cases diagnosed each year continues to rise. Cancer as a cause of death has been constantly increasing in Egypt and has become the leading cause of death. According to the Global Cancer Observatory, Egypt had an estimated age-standardized incidence rate (ASR) for cancer of 175.1 and 161.1 for males and females, respectively, in 2022. This translates to a larger patient population requiring specialized nutritional support during treatment, which in turn drives the Clinical Nutrition for Cancer Care Market further.

Improved Healthcare Infrastructure: With the establishment of new hospitals and specialist cancer care clinics, Egypt’s healthcare infrastructure is improving. These facilities have departments or staff specializing in clinical nutrition for cancer patients. These departments can provide comprehensive nutritional assessments, develop personalized nutrition plans, and offer specialized services like enteral and parenteral nutrition support. Improved infrastructure facilitates the adoption of advanced medical technologies for cancer diagnosis and treatment. These advanced treatments, like complex surgeries or radiation therapy, often require specialized nutritional support to manage side effects and optimize patient recovery. Improved health infrastructure plays a vital role in propelling the Egypt Clinical Nutrition for Cancer Care Market by creating a conducive environment for specialized services, fostering advanced treatment approaches, and facilitating collaboration among healthcare professionals.

Rising Disposable Incomes: As disposable incomes rise, households in Egypt have more money to allocate towards healthcare. This translates into a greater willingness to pay for specialized services like clinical nutrition for cancer care. Previously, patients might have relied solely on traditional remedies or basic nutritional support due to financial constraints. Increased disposable income allows them to consider additional services that can improve treatment outcomes and quality of life. Consequently, rising disposable incomes can lead to a growing demand for personalized and comprehensive cancer care plans. Clinical nutrition plays a crucial role in achieving this by tailoring nutritional plans to individual needs and preferences. Patients might be more willing to invest in services that offer a more holistic approach to cancer care, including personalized nutritional support. Thus, rising disposable incomes in Egypt allow patients to invest in specialized services like clinical nutrition for cancer care which ultimately drives the growth of the Egypt Clinical Nutrition for Cancer Care Market.

Market Restraints

Varied reimbursement policies: Reimbursement policies for nutritional support products like oral nutritional supplements (ONS) and enteral feeding formulas differ significantly across regions and even within healthcare systems. This can create access disparities for patients, particularly in areas with limited coverage or complex procedures for reimbursement. Thus, due to cost and reimbursement issues, the Clinical Nutrition for Cancer Care Market might not grow to its full potential.

Limited Awareness: While awareness is increasing, not all healthcare professionals may fully understand the significance of clinical nutrition in cancer care. This can lead to underutilization of nutritional support services and a failure to identify patients who could benefit from them. Some patients might not be fully aware of the benefits of proper nutrition during cancer treatment and the available support options. Therefore, the limited awareness can prevent the Clinical Nutrition for Cancer Care Market from growing.

Challenges in Implementation: The trend towards personalized nutrition plans requires adequate resources and support systems to effectively implement these plans for each patient after consideration of many factors. Also, seamlessly integrating clinical nutrition services into existing healthcare workflows can be challenging. This might require changes in practice patterns and fostering collaboration among different healthcare professionals. These changes in the healthcare structure can be hard to incorporate thus acting as a restraint for the Clinical Nutrition for Cancer Care Market.

Regulatory Landscape and Reimbursement Scenario

The Egyptian Drug Authority (EDA) is Egypt’s pharmaceutical regulatory body, overseen by the Ministry of Health. It plays a vital role in ensuring the efficacy, safety, and quality of medications that are made available in the nation. The comprehensive drug approval procedure that the EDA enforces helps guarantee that only safe and effective pharmaceuticals are supplied to the Egyptian market; innovative medications that have undergone adequate testing are beneficial to patients; and public health is protected by reducing the risks associated with potentially harmful or ineffective medications.

Before new pharmaceuticals are offered in Egypt, the EDA examines applications and authorizes their marketing. It also grants licenses to producers, distributors, and wholesalers of pharmaceuticals and medical equipment. The EDA ensures medications fulfil the criteria of quality necessary for the purposes for which they are intended. This entails conducting quality control procedures, keeping up a national drug control laboratory, and inspecting manufacturing sites. When evaluating novel drugs, the EDA examines and approves clinical trial applications to guarantee participant safety and ethical research procedures. After a drug is placed in the market, the EDA actively monitors its safety by gathering and evaluating information on side effects that patients and medical experts have reported.

Egypt’s health insurance landscape includes the Universal Health Insurance (UHI) program. The UHI Law was passed in 2017 and replaced the previously fragmented insurance system of Egypt. The law aimed to provide comprehensive health insurance coverage to all Egyptian citizens. The goal of the UHI program is to provide a uniform benefits package that includes services for preventive care (checkups, screenings), services for both inpatient and outpatient care, necessary prescription drugs, maternity care, and emergency medical attention

Competitive Landscape

Key Players

Here are some of the major key players in the Egypt Clinical Nutrition for Cancer Care Market:

- Fresenius Kabi

- Otsuka

- Egyptian Society of Nutrition and Food Science (ESNFS)

- Abbott Nutrition

- Danone Nutrica

- Nestlé Health Science

- Baxter International

- Victus Inc.

- Mead Johnson Nutrition

- Aymes

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Clinical Nutrition for Cancer Care Market Segmentation

By Type

- Oral Nutrition

- Parenteral Nutrition

- Enteral Feeding Formulas

By Cancer Type

- Head & Neck Cancer

- Stomach & Gastrointestinal Cancer

- Blood Cancer

- Breast Cancer

- Lung Cancer

- Others

By Age Group

- Adult

- Paediatric

By Sales Channel

- Offline

- Online

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Japan Cardiovascular Diseases Therapeutics Market Analysis

Pharmaceuticals

Japan Tetanus Toxoid Vaccine Market Analysis

Pharmaceuticals

Malaysia Hepatitis A Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Egypt Insulin Market Analysis

Pharmaceuticals

Egypt Contraceptives Drugs Market Analysis

Pharmaceuticals