Pharmaceuticals

Egypt Cholesterol Therapeutics Market Analysis

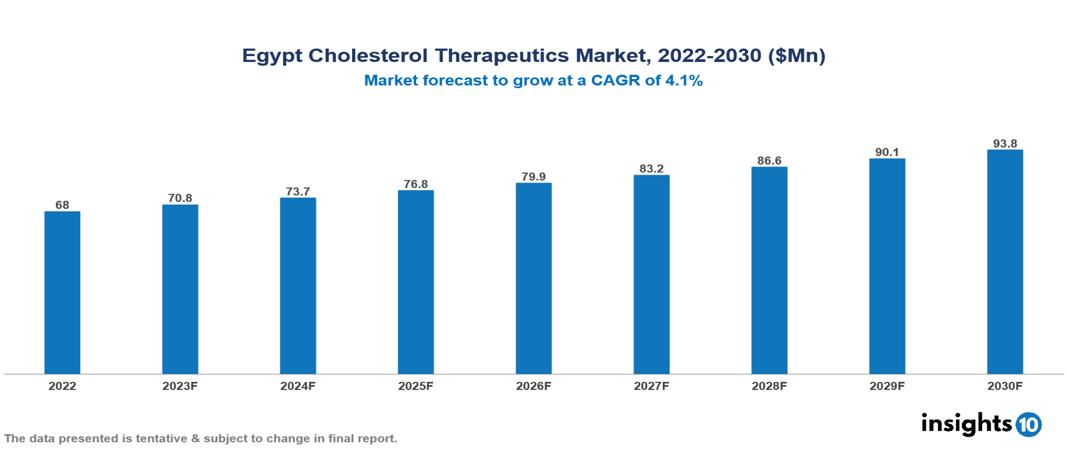

The Egypt Cholesterol Therapeutics Market is anticipated to experience a growth from $68 Mn in 2022 to $94 Mn by 2030, with a CAGR of 4.1 % during the forecast period of 2022-2030. The market is being driven by the confluence of innovative drug classes in the treatment of cholesterol-induced diseases, the escalating prevalence of cardiovascular diseases, and the collaborative efforts between public and private entities. The Egypt Cholesterol Therapeutics Market encompasses various players across different segments such as Pfizer, Sanofi, Bayer, AstraZeneca, Novartis, MinaPharm, Nile Pharma, EIPICO, Pharco Pharmaceuticals, EVA Pharma, etc., among various others.

Buy Now

Egypt Cholesterol Therapeutics Market Analysis Executive Summary

The Egypt Cholesterol Therapeutics Market is anticipated to experience a growth from $68 Mn in 2022 to $94 Mn by 2030, with a CAGR of 4.1 % during the forecast period of 2022-2030.

Cholesterol, a lipid-like substance found in all cells, plays a vital role in the synthesis of hormones, vitamin D, and bile acids. It exists in two main types: low-density lipoprotein (LDL) and high-density lipoprotein (HDL). While HDL is advantageous, assisting in the elimination of LDL, elevated levels of LDL can lead to atherosclerosis, causing the narrowing of arteries and contributing to cardiovascular issues such as heart attacks and strokes. Addressing high cholesterol traditionally involves lifestyle modifications, including dietary changes, regular physical activity, and smoking cessation. Medications like statins, which inhibit cholesterol production, are commonly prescribed for managing cholesterol levels. Innovative treatments, such as PCSK9 inhibitors that enhance LDL removal, and emerging drugs targeting specific cholesterol metabolism pathways, offer alternatives for individuals with suboptimal responses to conventional methods or those experiencing side effects from medications. These advanced therapies aim to provide options for managing cholesterol effectively, particularly for individuals who may not respond optimally to standard approaches or face challenges with medication side effects. In essence, the comprehensive management of cholesterol involves a combination of personalized medical interventions and lifestyle adjustments, playing a crucial role in minimizing the risk of cardiovascular complications.

Premature acute coronary syndrome (ACS) is common in Egyptians, affecting 46% of men under 55 and 67% of women under 65. The incidence of hypercholesterolemia in Egypt is reported to be between 17% and 19.4% in the general population, with a greater prevalence among individuals with ACS of 58.7% to 75%.

The market is being driven by the confluence of innovative drug classes in the treatment of cholesterol-induced diseases, the escalating prevalence of cardiovascular diseases, and the collaborative efforts between public and private entities.

Egypt Cholesterol Therapeutics Market thrives on a mix of local giants like EVA Pharma and Pharco offering generics, while multinationals like Novartis bring premium brands. There are certain innovative players like Amoun focusing on the R&D of novel drugs. Price sensitivity drives generics' popularity, while innovation in novel therapies promises future growth.

Market Dynamics

Market Growth Drivers

Increased innovation in treatment: The cholesterol therapeutics market is witnessing significant momentum driven by several key factors that shape its evolving landscape. One prominent driver is the advent of innovative drug classes, exemplified by the growing popularity of PCSK9 inhibitors. These novel medications are gaining substantial traction, particularly among high-risk patients and those showing suboptimal responses to traditional statin therapy.

Higher prevalence of diseases: The prevalence of CVDs serves as another pivotal driver propelling the cholesterol therapeutics market forward. Countries, such as Egypt, are grappling with a notable burden of CVD, exacerbated by escalating rates of obesity, diabetes, and unhealthy lifestyles. The resultant surge in cholesterol levels is fueling a heightened demand for effective cholesterol-lowering medications. This demographic trend underscores the urgency of robust strategies to manage cardiovascular risk factors comprehensively.

Increased Public-Private Partnerships (PPPs): Furthermore, the evolving landscape is shaped by the dynamic interplay of PPPs. Collaborations between governmental bodies and private healthcare providers are instrumental in enhancing access to crucial cholesterol-lowering medications. These partnerships not only improve medication accessibility but also facilitate a more extensive treatment coverage. By synergizing efforts, these collaborations contribute to the development and implementation of strategies that cater to a broader segment of the population, ultimately fostering a more resilient and responsive cholesterol therapeutics market.

Market Restraints

Restricted access to healthcare facilities: Restricted access and a scarcity of qualified medical professionals act as a challenge in the growth of this market. This limitation poses a hindrance to timely diagnosis and adherence to treatment regimens. Residents in these regions often face formidable obstacles in accessing essential healthcare services, thereby exacerbating health disparities and impeding the effective management of various medical conditions.

Affordability: Despite the existence of cost-effective alternatives, some patients, particularly those lacking insurance coverage or facing inadequate financial support, grapple with the financial burden of obtaining essential medications. Affordability challenges create barriers to optimal healthcare, underscoring the need for comprehensive strategies to address economic disparities and ensure that individuals can access and afford the medications crucial for their well-being.

Lack of awareness and prevailing misconceptions: Limited health literacy, coupled with cultural beliefs, can foster resistance towards adopting preventive measures and adhering to prescribed medications. Addressing these issues necessitates targeted educational initiatives that promote health literacy and dispel misconceptions.

Healthcare Policies and Regulatory Landscape

The Egyptian Drug Authority (EDA) plays a pivotal role in safeguarding public health standards by overseeing the regulation of pharmaceuticals and healthcare products in Egypt. Operating under the Ministry of Health and Population, the EDA ensures that drugs available in the country adhere to stringent criteria regarding safety, efficacy, and quality. Its responsibilities encompass the entire lifecycle of pharmaceutical products, including approval, registration, and continuous post-market surveillance. One of its primary functions is to evaluate and grant marketing authorization to drugs, subjecting them to a thorough assessment of scientific and clinical data to establish their safety and effectiveness before being allowed into the Egyptian market. Post-approval, the EDA remains vigilant in monitoring drug safety through pharmacovigilance activities, involving the continuous collection, evaluation, and response to information regarding adverse effects or any issues related to drugs. The EDA actively collaborates with healthcare professionals, manufacturers, and the public to maintain a comprehensive and timely reporting system

Competitive Landscape

Key Players:

- Pfizer

- Sanofi

- Bayer

- AstraZeneca

- Novartis

- MinaPharm

- Nile Pharma

- EIPICO

- Pharco Pharmaceuticals

- EVA Pharma

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Cholesterol Therapeutics Market Segmentation

By Indication

- Hypercholesterolemia

- Hyperlipidaemia

- Cardiovascular Diseases

- Others

By Drug Class

- Statins

- Bile Acid Sequestrants

- Lipoprotein Lipase Activators

- Fibrates

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End User

- Hospitals

- Speciality Clinics

- Homecare

- Academics & Research Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Japan Oral Thin Films Market Analysis

Pharmaceuticals

US Contraceptives Drugs Market Analysis

Pharmaceuticals

UAE Alopecia Drugs (Hair Loss) Market Analysis

Related reports (by geography)

Medical Devices