Medical Devices

Egypt Bio-Implant Market Analysis

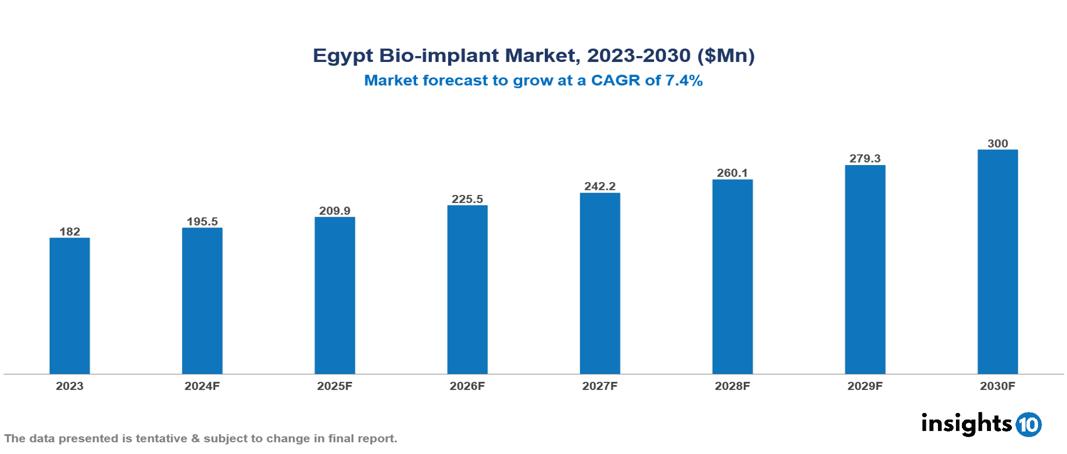

The Egypt Bio-implant Market was valued at $182 Mn in 2023 and is predicted to grow at a CAGR of 7.4/% from 2023 to 2030, to $300 Mn by 2030. The Egypt Bio-implant Market is growing due to like Increasing Chronic Disease Prevalence, Rising Disposable Income and Healthcare Spending, and Technological Innovations in Implant Materials. The market is primarily dominated by players such as Alexandria Advanced Technologies, Medica Egypt, Misr Medicare, Zimmer Biomet, Boston Scientific Corporation, Otto Bock Holding GmbH & Co. KG, and Medtronic plc.

Buy Now

Egypt Bio-implant Market Executive Summary

The Egypt Bio-implant Market is at around $182 Mn in 2023 and is projected to reach $300 Mn in 2030, exhibiting a CAGR of 7.4% during the forecast period.

Bioimplants are cutting-edge medical devices designed to be implanted in the body, aiming to support or replace biological structures or functions. They vary from simple dental implants to intricate devices like pacemakers, prosthetic joints, and neurological implants. The primary purpose is to improve the quality of life for individuals by restoring functions lost or damaged by disease or injury. Composed of biocompatible materials, bioimplants minimize the likelihood of rejection. Innovations like wireless connectivity and sensors, which enable real-time monitoring and remote modifications, are driving the market's growth.

In Egypt, chronic diseases like diabetes and cardiovascular ailments affect a significant portion of the population, with diabetes prevalence at approximately 17.8%. The aging population, projected to increase by 2% annually, underscores rising demand for bioimplants, especially orthopedic implants. Demographic shifts towards urbanization, with over 43% of the population residing in urban areas, influence healthcare access and bioimplant adoption. These factors highlight both the growing need for and challenges in the bioimplant market in Egypt, where improving healthcare infrastructure and addressing economic disparities are critical for market expansion. Therefore, the market is driven by significant factors like Increasing Chronic Disease Prevalence, Rising Disposable Income and Healthcare Spending, and Technological Innovations in Implant Materials. However, Limited Healthcare Infrastructure, Metal Allergies and Bio-implants, Regulatory restrict the growth and potential of the market.

Zimmer Biomet has launched new knee and hip implant systems designed to cater to the specific anatomical needs of Egyptian patients, thereby addressing local market demands more effectively.

Market Dynamics

Market Growth Drivers

Increasing Chronic Disease Prevalence: Egypt faces rising incidences of chronic diseases such as diabetes and cardiovascular diseases, which often necessitate bioimplants like cardiac stents and joint replacements. The prevalence of diabetes alone was estimated at 17.7% among adults in 2021, according to the International Diabetes Federation.

Rising Disposable Income and Healthcare Spending: Increasing disposable incomes and healthcare spending per capita in Egypt support the affordability and adoption of advanced medical treatments, including bioimplants. The GDP per capita growth from $2,549 in 2019 to $3,208 in 2023 (World Bank, 2023) indicates a rising capacity to afford expensive medical procedures, driving the bioimplant market forward.

Technological Innovations in Implant Materials: Technological advancements in biomaterials and implant design improve the durability, biocompatibility, and functionality of implants. Innovations such as 3D printing of implants and the development of bioresorbable materials are gaining traction, enhancing treatment outcomes and patient satisfaction.

Market Restraints

Limited Healthcare Infrastructure: Outside major urban centers like Cairo and Alexandria, healthcare infrastructure in Egypt is often underdeveloped, lacking adequate facilities and skilled healthcare professionals. This limits the accessibility and distribution of bioimplants, particularly in rural areas where healthcare services are sparse.

Metal Allergies and Bio-implants: The primary immunological response to implants is often metal sensitivity. Titanium, cobalt, chromium, and stainless steel (including nickel) are commonly used in orthopedic and dental implants. Nitinol, an alloy of titanium and nickel, is employed in cardiac stents and patches. Medical implants frequently utilize metal alloys like titanium, nickel, cobalt, chromium, molybdenum, and zirconium.

Regulatory Hurdles: The regulatory environment in Egypt can be complex and bureaucratic, leading to delays in approvals for new medical devices, including bioimplants. Stringent regulatory requirements may also increase the time and cost associated with bringing new products to market, discouraging investment and innovation in the bioimplant sector.

Regulatory Landscape and Reimbursement Scenario

Egyptian Drug Authority (EDA), oversees the registration, importation, and distribution of medical devices, including bioimplants. Regulatory requirements involve stringent assessments of safety, efficacy, and quality standards, often aligning with international norms to ensure patient safety. Manufacturers must obtain EDA approval before marketing their products in Egypt, which includes submission of clinical data, technical documentation, and compliance with Good Manufacturing Practices (GMP). The EDA periodically updates regulations to keep pace with advancements in medical technology and global standards, aiming to foster a competitive yet controlled market environment.

The absence of comprehensive healthcare coverage limits patient access to expensive bioimplant procedures, particularly affecting segments like orthopedic and dental implants. Government initiatives aimed at expanding healthcare coverage are crucial for overcoming this barrier and facilitating greater market penetration. Additionally, partnerships between healthcare providers and insurers could enhance reimbursement options, thereby stimulating growth in this sector and addressing the healthcare needs of Egypt's population.

Competitive Landscape

Key Players

Here are some of the major key players in the Egypt Bio-implant Market:

- Alexandria Advanced Technologies

- Medica Egypt

- Misr Medicare

- Straumann AG

- Zimmer Biommer

- Boston Scientific Corporation

- Otto Bock Holding GmbH & Co. KG

- Medtronic

- Boston Scientific Corporation

- Johnson & Johnson Services, Inc.

- LifeNet Health

- Smith & Nephew

- Arthrex, Inc

- Clinic Lemanic

- DePuy Synthes

- Exactech, Inc.

- Cochlear Ltd

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Bio-implant Market Segmentation

By Material

- Ceramics

- Polymers

- Alloys

- Biomaterials Metals

By Type

- Dental Bio-implants

- Orthopedic Bio-implants

- Spinal Bio-implants

- Ophthalmology Bio-implants

- Cardiovascular Bio-implants

- Others

By Mode of Administration

- Surgical

- Injectable

By End User

- Hospitals

- Speciality Clinics

- Ambulatory surgical centers

By Origin

- Autograft

- Allograft

- Xenograft

- Synthetic

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Mexico Biosensors Market Analysis

Medical Devices

APAC Pain Management Devices Market Analysis

Medical Devices

Singapore Cardiac Monitoring Devices Market Analysis

Related reports (by geography)

Pharmaceuticals

Egypt Lactoferrin Market Analysis

Pharmaceuticals

Egypt Hangover Rehydration Supplements Market Analysis

Pharmaceuticals