Pharmaceuticals

Egypt Age-Related Macular Degeneration Therapeutics Market Analysis

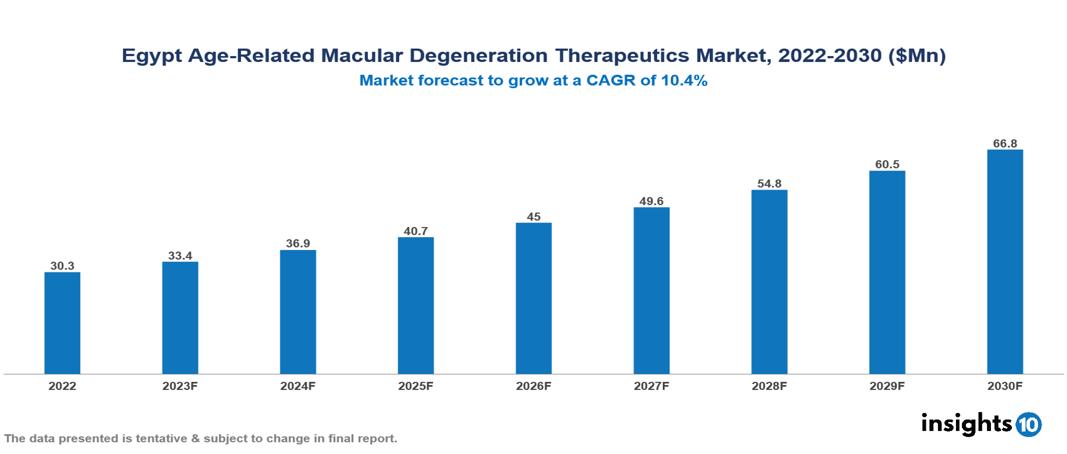

The Egypt Age-Related Macular Degeneration (AMD) Therapeutics Market was valued at US $30 Mn in 2022 and is predicted to grow at a CAGR of 10.40% from 2023 to 2030, to US $67 Mn by 2030. The key drivers of this industry include the upward trend in the prevalence of age-related macular degeneration, a strong product pipeline, and other factors. The industry is primarily dominated by players such as Novartis, Bayer, Roche, Regeneron Pharmaceuticals, and Genetech, among others

Buy Now

Egypt Age-Related Macular Degeneration Therapeutics Market Analysis: Executive Summary

The Egypt Age-Related Macular Degeneration (AMD) Therapeutics Market is at around US $30 Mn in 2022 and is projected to reach US $67 Mn in 2030, exhibiting a CAGR of 10.40% during the forecast period.

Age-related macular degeneration (AMD) is a degenerative eye disease that primarily affects older people and can result in considerable vision loss. It has an effect on the macula, which is in control of central vision. Diabetes, smoking, lifestyle changes, and other variables are non-modifiable risk factors for AMD. AMD is classified into two types: dry AMD and wet AMD. Distorted vision, difficulties seeing clearly, and a gradual loss in eyesight are common symptoms. Dry AMD is more frequent but progresses more slowly, whereas wet AMD is less common but more severe, with aberrant blood vessel formation beneath the macula. Anti-VEGF therapy, such as Lucentis, Vabysmo, Avastin from Genentech, and Eylea from Regeneron Pharmaceuticals, are some of the approved treatment options. Other treatments include laser therapy and the use of nutritional supplements like zinc and copper as preventive measures.

The overall prevalence of AMD in Egypt is estimated to be around 6.5% in the age group of 50–80 years. The estimated prevalence of early and late AMD is about 5.3% and 2.4%, respectively. The prevalence is considered to be directly correlated with age. The market is influenced by driving factors such as an increasing older population and the resulting increase in prevalence, the emergence of new products in the pipeline, and increased government spending in the therapeutics industry. However, high treatment costs, limited healthcare infrastructure, and a competitive market are a few factors that limit the market's potential.

Market Dynamics

Market Growth Drivers

Surge in the prevalence of AMD: It is estimated that the overall prevalence of AMD is about 6.5% in Egypt. The prevalence of early AMD is approximately 5.3%, whereas that of late AMD is about 2.4%. The aging population in the country is consistently growing, leading to a larger group of patients requiring regular treatments and facilitating market expansion. Moreover, the escalating prevalence of diabetes and obesity, recognized as notable risk factors for AMD, adds to these estimates. The rising incidence of these health conditions in Egypt heightens their potential influence on the market.

Strong product pipeline: The introduction of novel products for AMD treatment is expected to significantly propel the market forward. Pharmaceutical firms are dedicating resources to research and development to introduce enhanced and innovative drugs, foreseeing substantial market growth. The robust product pipeline for AMD treatments, encompassing emerging therapeutic approaches, gene therapy, and sustained-release drug delivery systems, is anticipated to be a driving force for market growth in Egypt.

Increased government spending: There is a steep increase in investments by the Egyptian government and external agencies towards managing chronic conditions, including AMD. Government funding is used to increase health insurance coverage to include AMD treatments, such as anti-VEGF medications, which are inaccessible to many Egyptians due to their expensive cost.

Market Restraints

High costs of treatment: Anti-VEGF therapies such as Eylea and Beovu come at a considerable expense, frequently reaching tens of thousands of Egyptian pounds per injection, which poses a significant financial strain for the majority. This leaves many individuals dependent on restricted health insurance coverage or unable to afford the treatment altogether.

Limited healthcare infrastructure: The presence and accessibility of advanced healthcare facilities and specialized treatment centres for AMD in Egypt is restricted, potentially influencing the acceptance of new therapeutic approaches. The availability of advanced diagnostic instruments and specialized professionals such as ophthalmologists is constrained in specific areas, affecting the possibilities for diagnosis and treatment and restricting market growth.

Competitive market: The existence of a competitive market with established players and current treatment alternatives presents obstacles for the introduction and acceptance of new therapies for AMD.

Healthcare Policies and Regulatory Landscape

Egypt's healthcare policies and regulatory framework are overseen by the Ministry of Health and Population (MoHP) and primarily governed through the Egyptian Medical Facilities Law, the Egyptian Drug Authority (EDA), and the Egyptian Diagnostics Clinical Laboratories Law. The healthcare system in Egypt traditionally integrates both the public and private sectors, with ongoing initiatives focused on improving medical facilities, enhancing service provision, and extending healthcare access to underserved regions. The country has implemented health policies and collaborated with the private sector to diversify its service offerings.

Significant transformations are underway in the Egyptian Health System, prompting stakeholders to gain a deeper understanding of the current framework and anticipate future developments. The recent approval of the Social Health Insurance Law serves as a driving force aiming to reduce out-of-pocket expenses and broaden coverage. Although Egypt's healthcare market heavily relies on out-of-pocket payments, there is an anticipated shift towards increased public expenditure.

Egypt's healthcare system faces numerous challenges in improving and safeguarding the health and well-being of its citizens. The government has placed emphasis on expanding social health insurance coverage and delivering an economical and efficient set of essential health services aligned with the population's most critical health needs.

Competitive Landscape

Key Players

- Regeneron Pharmaceuticals

- Novartis AG

- F. Hoffman-La-Roche Ltd

- Apellis Pharmaceuticals

- AbbVie

- Bayer

- Pfizer Inc

- Regenxbio Inc

- Kanghong Pharma

- Bausch Health Companies, Inc

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Age-Related Macular Degeneration Therapeutics Market Segmentation

By Disease Type

- Dry AMD

- Wet AMD

By Drug

- Lucentis

- Eylea

- Beovu

By Age Group

- Less than 60

- Between 60-80

- More than 80

By Stage

- Early AMD

- Intermediate AMD

- Advanced AMD

- No AMD

By Distribution Channel

- Hospital Pharmacy

- Specialty Pharmacy

Online Pharmacy

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Spain Congestive Heart Failure Therapeutics Market Analysis

Pharmaceuticals

North America Antifungal Drugs Market Analysis

Pharmaceuticals

Japan Axial Spondyloarthritis (axSpA) Market Analysis

Related reports (by geography)

Pharmaceuticals

Egypt Oral Contraceptives Market Analysis

Healthcare Services

Egypt Clinical Trial Kits Market Analysis

Healthcare Services

Egypt Diagnostic Ultrasound Market Analysis

Rare Diseases