Pharmaceuticals

Egypt Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

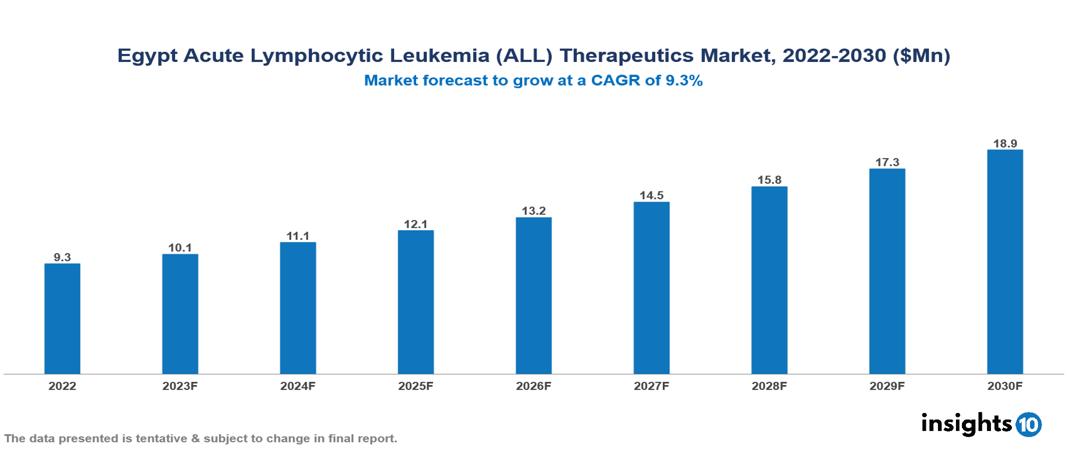

The Egypt Acute Lymphocytic Leukemia (ALL) Therapeutics Market was valued at US $9 Mn in 2022, and is predicted to grow at (CAGR) of 9.3% from 2023 to 2030, to US $19 Mn by 2030. The key drivers of this industry include a surge in the incidence of acute lymphocytic Leukemia cases, expanding healthcare infrastructure by continuous investment, increased government funding initiatives and other factors. The industry is primarily dominated by players such as Pharco, EIPICO, Amoun, Novartis, among other players.

Buy Now

Egypt Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

The Egypt Acute Lymphocytic Leukemia (ALL) Therapeutics Market is at around US $9 Mn in 2022 and is projected to reach US $19 Mn in 2030, exhibiting a CAGR of 9.3% during the forecast period.

Acute Lymphocytic Leukemia (ALL) is characterized by the rapid multiplication of immature white blood cells, called lymphoblasts, within the bone marrow. This condition usually stems from a genetic mutation impacting developing lymphocytes, leading to the accumulation of undifferentiated lymphoid cells. Symptoms include frequent infections, enlarged lymph nodes, weight loss, bone pain, and other manifestations. Managing ALL requires an extensive treatment plan spanning months or even years, involving various therapies like chemotherapy, targeted treatments, CAR-T cell immunotherapy, and, in severe cases, stem cell transplantation. These advancements in treatment significantly improve the chances of a cure, with success rates reaching up to 80%.

Childhood ALL has an estimated incidence of 3.4/1,000,000 in Egypt and is anticipated to rise. The market is therefore driven by major factors like the surge in incidence of ALL, expanding healthcare infrastructure through ongoing investments, and increased government funding in the therapeutics industry. However, conditions such as high costs of treatment, limited access to targeted therapeutics, and other factors hinder the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increased cases of ALL: According to the National Cancer Registry Program, the approximate incidence of childhood ALL is 3.4/1,00,000 and is anticipated to rise further. Thus, the market is driven by a huge pool of patients.

Expanding healthcare infrastructure: The government, along with external funding agencies, has invested heavily to establishing specialized care facilities for hematology and oncology, especially in urban regions, which enhances patients' accessibility to treatment options. There are 11 dedicated oncology centers, including the National Cancer Institute. Such developments further fuel market growth.

Increased government initiatives: The Egyptian government had made efforts to support cost and clinically effective treatment to paediatric and adult ALL patients. Programs such as the Universal Health Insurance (UHI) scheme and the National Cancer Control Plan emphasize providing access to crucial cancer treatments, including those for ALL.

Market Restraints

Limited access: There's a need for focused care for underprivileged population, addressing sociodemographic and socioeconomic gaps. The public health insurance system remains insufficiently developed. There exist disparities between access of care in rural and urban areas where novel treatment options remain inaccessible to majority of Egyptian population

Affordability: Finding a middle ground between embracing innovative, potentially curative treatments such as CAR-T and ensuring affordability for all patients poses a challenge for healthcare policymakers. Vital strategies, like negotiating with pharmaceutical firms for reduced prices, exploring different funding approaches, and broadening insurance coverage, are lacking and restraint growth.

High cost: There are challenges concerning the accessibility and affordability of laboratory tests. Numerous families face difficulties affording the required laboratory studies necessary for optimal risk-oriented therapy potentially surpassing the financial means of many patients and the limits of their healthcare coverage.

Healthcare Policies and Regulatory Landscape

Egypt's healthcare policy and regulatory framework are managed by the Ministry of Health and Population (MoHP) and chiefly regulated through the Egyptian Medical Facilities Law, Egyptian Drug Authority (EDA), and the Egyptian Diagnostics Clinical Laboratories Law. The healthcare system in Egypt historically integrates both public and private sectors, with ongoing efforts focused on enhancing medical facilities, enhancing service provision, and expanding healthcare access to underserved regions. The nation has introduced health policies and collaborated with the private sector to broaden service offerings.

The Egyptian Health System is undergoing substantial transformations, necessitating stakeholders to gain a deeper comprehension of the current framework and future developments. The recent endorsement of the Social Health Insurance Law is a driving force aiming to diminish out-of-pocket expenditure and broaden coverage. Egypt's healthcare market primarily relies on out-of-pocket payments, but there's an expected transition towards increased public expenditure.

Egypt's healthcare system encounters numerous hurdles in enhancing and securing the health and welfare of its citizens. The government has placed emphasis on broadening social health insurance coverage and delivering an economical and efficient set of fundamental health services aligned with the population's most crucial health requirements.

Competitive Landscape

Key Players

- Pharco Pharmaceuticals

- EIPICO

- Amoun Pharmaceutical

- Pfizer

- Novartis

- GlaxoSmithKline

- Sanofi

- AstraZeneca

- Boehringer Ingelheim International

- AbbVie Inc

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Egypt Acute Lymphocytic Leukemia (ALL) Therapeutics Market Segmentation

By Type

- Paediatrics

- Adults

By Drug

- Hyper CVAD regimen

- Linker Regimen

- Nucleoside Metabolic Inhibitors

- Targeted drugs and Immunotherapy

- CALGB 811 Regimen

By Cell

- B Cell ALL

- T Cell ALL

- Philadelphia Chromosome

By Therapy

- Chemotherapy

- Targeted therapy

- Radiation therapy

- Stem Cell Transplantation

By Distribution channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Italy Antibacterial (Antibiotics) Drugs Market Analysis

Pharmaceuticals

UK Bone Marrow Aspirate Concentrates Market Analysis

Pharmaceuticals

Germany Cannabis Market Analysis

Related reports (by geography)

Rare Diseases

Egypt Hunter Syndrome Therapeutics Market Analysis

Rare Diseases

Egypt Rare Hemophilia Factors Market Analysis

Healthcare Services

Egypt Women Health Diagnostic Market Analysis

Pharmaceuticals