Pharmaceuticals

China Cardiac Resynchronization Therapy Market

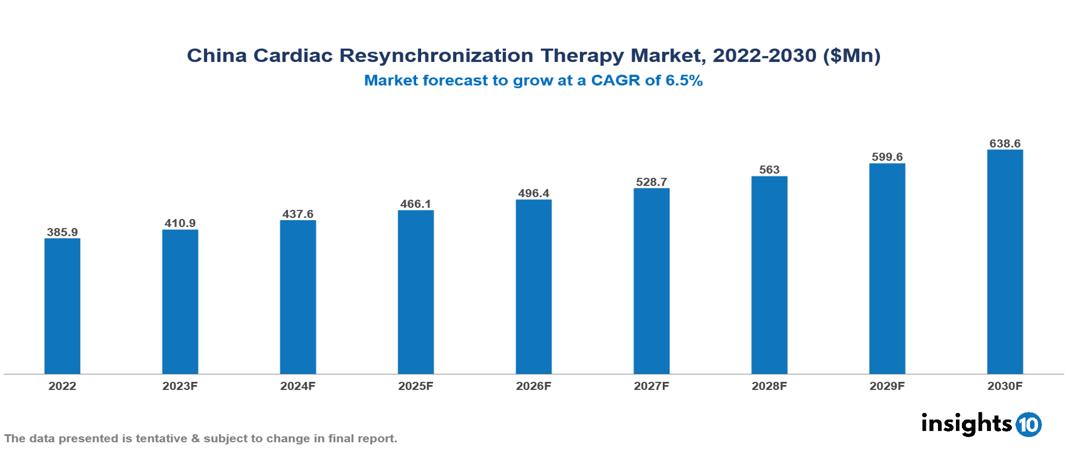

China Cardiac Resynchronization Therapy Market was valued at $386 Mn in 2022 and is estimated to reach $639 Mn in 2030, exhibiting a CAGR of 6.5% during the forecast period. The global surge in heart failure cases, driven by aging populations and lifestyle-related cardiovascular diseases, is a significant catalyst contributing to the expansion of the Cardiac Resynchronization Therapy (CRT) market. Currently, major contributors to this market include companies such as Medtronic, Boston Scientific, Abbott, Siemens Healthineers, MicroPort Apsara, Lepu Medical Technology Co., Beijing Easywell Medical Device Co., Shenzhen Lepu Heart Valve Technology Co., Terumo Corporation, and Osram Health.

Buy Now

China Cardiac Resynchronization Therapy Market Executive Summary

China Cardiac Resynchronization Therapy Market was valued at $386 Mn in 2022 and is estimated to reach $639 Mn in 2030, exhibiting a CAGR of 6.5% during the forecast period.

Cardiac resynchronization therapy (CRT) is a medical procedure involving the utilization of a pacemaker to rectify the heart's rhythm through a minimally invasive surgical procedure. The CRT pacemaker, positioned beneath the skin, harmonizes the timing between the upper and lower heart chambers, ensuring synchronization between the left and right sides of the heart. This therapeutic approach holds particular significance for individuals experiencing heart failure, as it addresses insufficient pumping and fluid accumulation in the lungs and legs resulting from the asynchronous beating of the heart's lower chambers. In instances of severe heart rhythm irregularities, CRT therapy may be complemented by the integration of an implantable cardioverter-defibrillator (ICD). The CRT device connects wires from the pacemaker to both sides of the heart, employing biventricular pacing to guarantee coordinated contractions and optimize overall heart function.

In China, cardiovascular diseases (CVD) pose a significant public health challenge, affecting approximately 330 Mn individuals, with around 11.39 Mn diagnosed with coronary heart disease (CHD), which includes heart attacks. CVD is a leading cause of mortality, accounting for 48.00% and 45.86% of deaths in rural and urban areas, respectively, with nearly two out of every five deaths attributed to cardiovascular issues. The mortality rate for heart diseases among male residents in rural China is notable at 192.09 deaths per 100,000 population. The aging demographic in China contributes to the increasing prevalence of heart attacks and other cardiovascular diseases, highlighting the need for proactive measures and interventions to address this growing health challenge. The prevalence of CVD in China is a major concern, with CVD accounting for a significant proportion of deaths in both rural and urban areas. The number of individuals affected by CVD, including CHD, is substantial, and the impact of CVD on mortality is alarming, particularly among the aging population in China.

China's MicroPort Apsara and the US company Pfizer are working together on developing the first drug-eluting lead that contains dexamethasone and is intended to reduce inflammation surrounding implant sites. This novel technique could lead to better patient outcomes overall and possibly increase pacemaker longevity. Clinical trials are currently being conducted to examine the efficacy of this innovative approach in greater depth. Simultaneously, Beijing-based Lepu Medical Technology Co., Ltd. has received regulatory approval in China for their drug-eluting lead, which also uses dexamethasone. This regulatory achievement represents a major advancement in the field of medical interventions for better patient care and highlights Lepu Medical Technology's dedication to developing cardiac implant technology.

Market Dynamics

Market Growth Drivers

Rising Prevalence of Heart Failure: The escalating prevalence of heart failure poses a significant public health challenge in China, impacting approximately 10.8 Mn individuals as of 2021. Projections indicate a further rise in this number, driven by factors such as shifts in lifestyle, an aging population, and heightened awareness of cardiovascular diseases. As a proven therapeutic intervention, cardiac resynchronization therapy (CRT) stands out in addressing heart failure, effectively enhancing symptoms, improving quality of life, and mitigating hospitalization rates. Hence expanding the market growth of cardiac resynchronization therapy.

Technological Advancements in CRT: Recent technological advancements in CRT devices have significantly transformed the landscape of heart failure treatment. The latest generation of CRT devices is distinguished by its compact design, enhanced energy efficiency, and sophisticated functionalities including wireless connectivity and remote monitoring. These improvements lead to better treatment outcomes in addition to increased patient comfort. The use of CRT therapy is being fuelled by its greater accessibility and appeal to patients and healthcare professionals.

Ageing Population: In 2023, over 264 Mn individuals aged 60 and above make up 18.9% of China's population, with projections suggesting an increase to 27% by 2035 and 37% by 2050. The aging demographic in China is associated with a higher risk of cardiovascular diseases (CVD) due to the established link between age and CVD. This shift emphasizes the need to address cardiovascular health and boosts the market potential for Cardiac Resynchronization Therapy (CRT) as a response to the growing prevalence of cardiovascular conditions in the aging population.

Market Restraints

Elevated Device Expenses: The cost of CRT devices is substantial, amounting to tens of thousands of dollars per unit. This significant initial expenditure poses a notable obstacle for patients, even with ongoing enhancements in reimbursement policies. Insufficient insurance coverage, particularly prevalent in rural areas, can further constrain patients' access to CRT therapy.

Insufficient Healthcare Workforce: China confronts a shortage of adequately trained healthcare professionals specializing in CRT implantation and monitoring procedures. This scarcity of expertise may limit the availability of this therapy in specific regions and lead to delays in patient treatment. It becomes imperative to address this shortage by expanding specialist training programs and ensuring an equitable distribution of qualified professionals across the country to facilitate broader CRT adoption.

Reimbursement Challenges: Despite some advancements, reimbursement policies for CRT in China are still in flux and exhibit regional variations. Ambiguities surrounding the long-term sustainability of reimbursement may present investment risks for hospitals and medical device companies. To bolster the case for broader and more stable reimbursement coverage, it is crucial to underscore the cost-effectiveness of CRT through comprehensive data collection and analysis.

Healthcare Policies and Regulatory Landscape

In China, the oversight of healthcare policies and regulations concerning treatment drugs is primarily overseen by the National Medical Products Administration (NMPA), formerly recognized as the China Food and Drug Administration (CFDA). The NMPA plays a crucial role in the evaluation and approval of pharmaceutical marketing, ensuring the safety, efficacy, and quality of these products. Regulatory clearance from the NMPA is also mandatory for the initiation of clinical trials, emphasizing adherence to ethical and safety standards. Moreover, the NMPA enforces Good Manufacturing Practices (GMP) to uphold pharmaceutical manufacturing quality and consistency. The pricing and reimbursement dynamics of treatment drugs in China are shaped by the National Healthcare Security Administration (NHSA), highlighting the government's participation in negotiating pricing and reimbursement policies.

Competitive Landscape

Key Players

- Medtronic

- Boston Scientific

- Abbott

- Siemens Healthineers

- MicroPort Apsara

- Lepu Medical Technology (Beijing) Co.

- Beijing Easywell Medical Device Co.

- Shenzhen Lepu Heart Valve Technology Co.

- Terumo Corporation

- Osram Health

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

China Cardiac Resynchronization Therapy Market Segmentation

By Product

- CRT-Defibrillator

- CRT-Pacemaker

By Age

- Below 44 years

- 45-64 years

- 65-84 years

- Above 85 years

By End-Users

- Hospitals

- Cardiac care Centres

- Ambulatory Surgical Centres

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

US Graft-versus-Host Disease (GvHD) Therapeutics Market Analysis

Pharmaceuticals

Canada Atherosclerosis Drugs Market Analysis

Pharmaceuticals

UK H1N1 Vaccines Market Analysis

Related reports (by geography)

Pharmaceuticals

China Vitamin and Minerals Market Analysis

Rare Diseases

China Fragile-X Syndrome Therapeutics Market Analysis

Healthcare Services

China Connected Healthcare Market Analysis

Pharmaceuticals