Healthcare Services

Canada Urgent Care Center Market Analysis

Canada Urgent Care Center Market is projected to grow from $xx Mn in 2023 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2023 - 2030. The market for Urgent Care Center is expanding as a result of favorable government policies and increasing prevalence of chronic diseases and accidents. This demand is fueling the development of better infrastructures and facilities for urgent care center. Some of the key players in the global Urgent Care center market include Concentra, Inc.; American Family Care; CityMD Urgent Care; MedExpress Urgent Care; NextCare Urgent Care; Tenet Health Urgent Care; FastMed Urgent Care; Ascension Health Urgent Care; WellNow Urgent Care; Sutter Health; Aurora Urgent Care; and Intuitive Health.

Buy Now

Canada Urgent Care Center Market Executive Summary

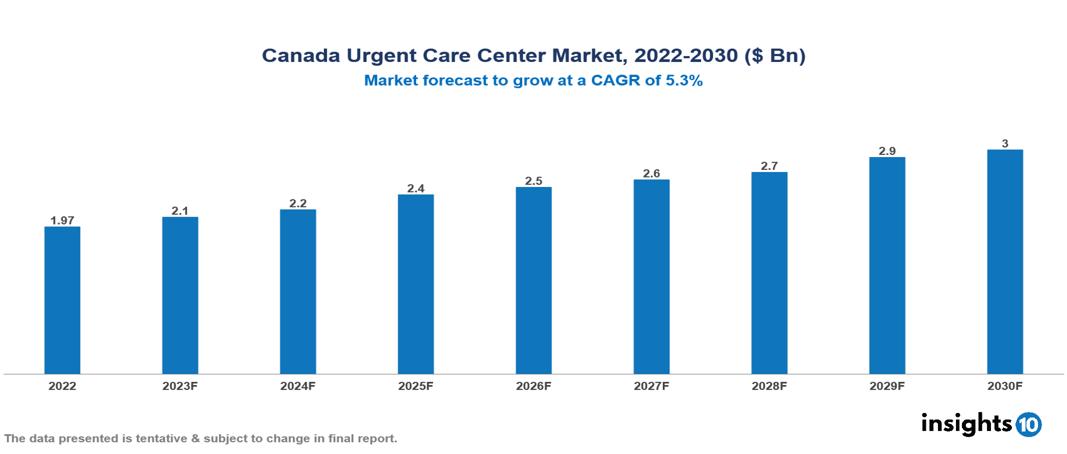

Canada Urgent Care Center Market is valued at around $1.97 Bn in 2022 and is projected to reach $2.97 Bn by 2030, exhibiting a CAGR of 5.3% during the forecast period 2023-2030.

Urgent Care Center Market refers to the market for healthcare facilities that provide treatment or medical care for injuries and sicknesses that require immediate attention but are not life-threatening. However, any delay in these treatments can affect to health of the patient or lead to disability. It is affordable and has a shorter waiting time compared to hospitals or other healthcare facilities.

The increasing prevalence of chronic diseases and road accidents has contributed to the growth of the global market for urgent care centers in recent years. Increasing demand for more affordable, convenient, and effective medical care or treatment has led to the global market for urgent care centers. They provide access to quality care services to patients.

There are many global players in the market of Urgent Care centers but Concentra, Inc.; American Family Care; CityMD Urgent Care; MedExpress Urgent Care; NextCare Urgent Care; Tenet Health Urgent Care; FastMed Urgent Care; Ascension Health Urgent Care; WellNow Urgent Care; Sutter Health; Aurora Urgent Care; and Intuitive Health are major players.

Demand for urgent care facilities is projected to increase in the younger population in the coming years. The elderly population is gradually shifting towards urgent care centers as it is affordable, convenient, and less time-consuming compared to other healthcare facilities. Urgent care centers are focusing on ground floor locations for easy access, streamlined appointment procedures, and a patient-centric approach. It is attributed to driving the Market for Urgent Care Centers.

Cost efficiency, the aging population, and investments in the healthcare sector are projected to fuel the market for Urgent Care centers in coming years. The market still has many challenges including patient preference, the limited scope of services, retention and recruitment of skilled surgeons, regulatory compliances, and increasing market competition.

Market Dynamics

Drivers of Canada Urgent Care Center Market

Increasing Need for Accessible Healthcare Services: People are turning towards more accessible healthcare facilities for shorter waiting times and timely medical care or treatment. Urgent care facilities are a practical substitute for hospitals and other healthcare facilities to get proper medical care during emergency situations when conditions are not life-threatening.

Cost-Effective: Urgent care centers are more affordable than hospital facilities or emergency rooms. Healthcare cost is increasing with time and people try to balance it with a more affordable and viable substitute. It is increasing demand for the urgent care center market.

Technological Advancement: There has been continuous advancements and new developments in the healthcare sector which has increased the demand for urgent care center. Telemedicine has boosted market demand as it allows patients to receive remote medical consultations with healthcare specialists from urgent care centers.

Focus on Preventive Care: Urgent care centers are focusing on vaccination, regular health checkups, and health screenings. With preventive care services urgent care centers are expanding their services and it has boosted the growth of the Urgent Care Center Market.

Partnerships and Consolidation: Hospitals, healthcare systems, and physicians’ groups are establishing an Urgent Care center to expand their services. It will improve healthcare infrastructure and better integration of care across the continuum.

Restraints of Canada Urgent Care Center Market

Patient Preference: Lack of awareness about Urgent Care centers and some patients prefer treatment in hospitals because of reservations in their minds, are affecting the growth of the Urgent Care center market. Hospitals have a wide range of services and facilities while urgent care centers have limits in services.

Limited Scope of Services: Urgent care centers provide immediate care for non-life-threatening conditions but it does not provide services to complex or critical cases because of a lack of specialized instruments and devices. For these conditions, patients have to be referred to hospitals or advanced healthcare facilities. It can hamper the growth of the Urgent Care Center Market.

Market Competition: Hospitals and healthcare systems are entering the market which is making it more competitive. Urgent Care centers need to differentiate themselves from other competitors by providing quality services, maintaining patient satisfaction rates, and building relationships with physicians and insurance companies to stay in the market.

Physician Recruitment and Retention: Urgent Care centers require skilled physicians, qualified nursing staff, and physician assistants for the treatment of patients. Hospitals and Urgent Care centers have an intense competition to attract and retain physicians. Work-life balance, compensation, and professional autonomy are the factors that play a major role in physicians’ retention and recruitment. Continuously looking out for these factors is challenging for Urgent Care centers.

Adapting to Changing Healthcare Policies: healthcare policies and regulations change for the Urgent Care market and adaptation to change is a challenge that can affect the market demand for Urgent Care centers.

Key players

Primacy Management Inc. Lifemark Health Group Appletree Medical Group TELUS Health MedCare Clinics Copeman Healthcare UHealth Clinic Medisys Health Group MCI The Doctor's Office Medvisit1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Market Segmentations For Canada Urgent Care Center Market

By Application

- Acute respiratory infection

- General Symptoms

- Injuries

- Joint/Soft Tissue Issues

- Digestive System Issues

- Skin Infections

- Urinary Tract Infections

- Ear Infections

- Sprains, Strains, and Fractures

- Influenza Pneumonia

- Disease of Respiratory Tract

- Others

By Ownership

- Hospital

- Corporation

- Physicians

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

India Medical Billing Outsourcing Market Analysis

Healthcare Services

Spain Community Oncology service Market Analysis

Healthcare Services

UK Urgent Care Center Market Analysis

Related reports (by geography)

Healthcare Services

Canada Interventional Radiology Market Analysis

Healthcare Services

Canada Laboratory Information System Market Analysis

Healthcare Services

Canada Soft Tissue Repair Market Analysis

Healthcare Services