Canada Teleradiology Market Analysis

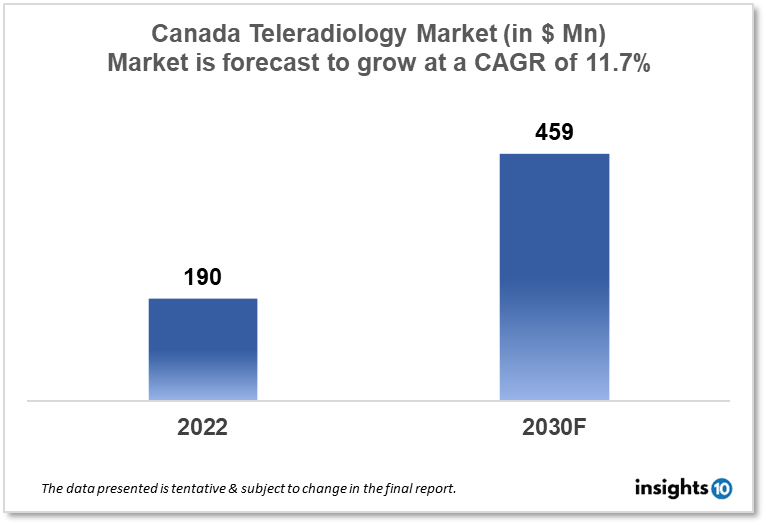

The Canada Teleradiology market size was valued at $190 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 11.7% from 2022 to 2030 and will reach $ 459 Mn in 2030. The market is segmented by application, modality, technology solutions, and end user. The Canada teleradiology market will grow due to Increasing demand for remote radiology services. The key market players are Radiology Consultants Associated (RCA), NightHawk Radiology Services, Calgary Scientific, and others.

Buy Now

Canada Teleradiology Market Executive Summary

The Canada Teleradiology market size was valued at $190 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 11.7% from 2022 to 2030 and will reach $ 459 Mn in 2030. Healthcare expenditure in Canada is primarily funded through a publicly funded, single-payer system known as Medicare. The system is administered by the provinces and territories, with federal funding provided to support the delivery of healthcare services across the country.

In 2021, total healthcare spending in Canada is projected to reach $298.5 Bn CAD, representing approximately 11.6% of the country's gross domestic product (GDP). This includes spending on hospitals, physicians, drugs, and other healthcare services and supplies. The largest portion of healthcare spending in Canada is on hospitals, which account for approximately 28% of total healthcare spending. Physician services represent the second-largest category of spending, at 15%, while drugs and other medical goods and services account for roughly 10% each.

Teleradiology is a medical practice in which radiological images, such as X-rays, CT scans, and MRI scans, are transmitted from one location to another for the purpose of interpretation and diagnosis. This allows radiologists and other medical professionals to review images remotely, which can be especially useful in situations where patients are located far away from medical facilities, or in emergency situations where a radiologist is not immediately available on site.

Canada has a well-established teleradiology system, which has been in place for many years. In fact, Canada was one of the first countries to adopt teleradiology as a standard practice. Today, teleradiology services are available in many parts of Canada and are widely used by hospitals, clinics, and other medical facilities. One of the key advantages of teleradiology is that it allows radiologists to provide rapid, accurate diagnoses even when they are not physically present at the site where the images were taken. This can help to reduce patient wait times, improve patient outcomes, and increase the efficiency of the healthcare system as a whole. Teleradiology has me an essential part of modern healthcare in Canada and is likely to continue to play a growing role in the years to come. Therefore, the demand for the teleradiology market will increase during the forecast period.

Market Dynamics

Market Growth Drivers

- Increasing demand for remote radiology services: The demand for remote radiology services has been on the rise, particularly in remote and rural areas where access to radiologists may be limited. Teleradiology enables patients to receive prompt and accurate diagnoses regardless of their location.

- Advancements in technology: The development of new technologies and software has made it easier and more efficient to transmit and interpret radiology images remotely. This has led to increased adoption of teleradiology services by healthcare providers in Canada.

- Cost-effectiveness: Teleradiology can be a cost-effective solution for healthcare providers, as it eliminates the need for on-site radiologists and reduces wait times for patients.

- Growing healthcare industry: The healthcare industry in Canada is growing, driven by an aging population and increasing demand for medical services. This is expected to drive growth in the teleradiology market as well.

Market Restraints:

- Regulatory barriers: Teleradiology is subject to regulations and guidelines, which can create barriers to entry for new providers. This can limit competition and slow down market growth.

- Concerns about data privacy and security: Teleradiology involves the transmission and storage of sensitive patient information, which can raise concerns about data privacy and security. Providers must take steps to ensure that patient information is protected, which can add to the cost and complexity of teleradiology services.

- Technical challenges: Teleradiology requires reliable and high-speed internet connections to transmit images and data, which can be a challenge in remote and rural areas. Additionally, technical issues with equipment or software can disrupt the teleradiology process and affect the quality of patient care.

- Lack of standardization: The lack of standardized protocols and guidelines for teleradiology can make it difficult for healthcare providers to compare and evaluate different teleradiology services, which can limit adoption and growth in the market.

Competitive Landscape

Key Players

- Radiology Consultants Associated (RCA)

- NightHawk Radiology Services

- Calgary Scientific

- Canadian Teleradiology Services

- Teleradiology Solutions

- MedRay Imaging

- Teleradiology Providers

- Canaray

- Virtual Radiologic (vRad)

- Aris Radiology

Recent Developments

2020: MedRay Imaging, a Canadian teleradiology provider, was acquired by US-based imaging services company NucleusHealth.

2020: Teleradiology Solutions, a global teleradiology provider, acquired Canadian teleradiology company Canadian Teleradiology Services.

2020: Canaray, a Canadian teleradiology provider specializing in dental imaging, raised CAD $7.5 million in a funding round to support its growth and expansion.

Healthcare Policies and Regulatory Landscape

In Canada, teleradiology is subject to regulations and guidelines that are established by provincial and territorial medical regulatory bodies, as well as by the Canadian Medical Association (CMA). These regulations and guidelines are designed to ensure that teleradiology services are safe, effective, and meet established standards of practice.

One of the key areas of regulation in teleradiology is data privacy and security. Patient images and data must be transmitted and stored securely to protect patient confidentiality and prevent unauthorized access. Teleradiology providers are also required to comply with applicable privacy laws, such as the Personal Information Protection and Electronic Documents Act (PIPEDA). In addition, teleradiology providers must ensure that their equipment and processes meet established standards for image quality and accuracy. Radiologists who interpret teleradiology images must be licensed to practice medicine in the relevant province or territory, and must meet the same standards of practice as radiologists who interpret images in person.

Finally, teleradiology providers must establish appropriate policies and procedures for communication and collaboration with other healthcare providers, to ensure that patients receive appropriate follow-up care based on the results of their imaging exams. The regulatory framework for teleradiology in Canada is designed to ensure that patients receive safe, effective, and high-quality care, regardless of where they are located or where their imaging exams are performed.

Teleradiology Market Segmentation

By Application

- Picture Archiving and Communication System (PACS)

- Radiology Information System (RIS)

By Modality:

The market is divided into X-ray, computed tomography (CT), ultrasound, magnetic resonance imaging (MRI), nuclear imaging, fluoroscopy, and mammography segments based on Modality. The computed tomography market category held the biggest market share in 2020. Several medical specialties employ computed tomography, including cardiology, cancer, neurology, abdominal and pelvic imaging, as well as spine and musculoskeletal imaging. The teleradiology market is expanding in this sector due to factors including the rising demand for early and accurate diagnosis, technical improvements, and digitalization in this industry. Around 100 million CT scans are performed annually worldwide, according to the WHO. The demand for CT scans over other imaging modalities has increased due to the desire to avoid exploratory procedures and advancements in cancer diagnosis and therapy.

- X-Ray

- Magnetic Resonance Imaging

- Computed Tomography

- Ultrasound Systems

- Nuclear Imaging

By Technology Solutions

- Web-Based Teleradiology Solutions

- Cloud-Based Teleradiology Solutions

By End User

The market is divided into four categories based on the end users: long-term care facilities, nursing homes, and assisted living facilities; hospitals and clinics; diagnostic imaging centres and laboratories; and other end users. In 2019, the hospitals and clinics segment's revenue contribution was the highest. This segment's significant market share can be ascribed to the increase in diagnostic imaging operations carried out in hospitals, the hospitals' growing propensity to automate and digitise patient data, and the growing demand to raise the standard of patient care. In addition, the COVID-19 pandemic shortage of radiologists and the growing usage of new imaging modalities to boost hospital workflow efficiency are anticipated to enhance the development of this end-user segment.

- Hospitals and Clinics

- Diagnostic Imaging Center and Laboratories

- Long-term Care Centres, Nursing Homes, Assisted Living Facilities

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.