Pharmaceuticals

Canada Periodontal Therapeutics Market Analysis

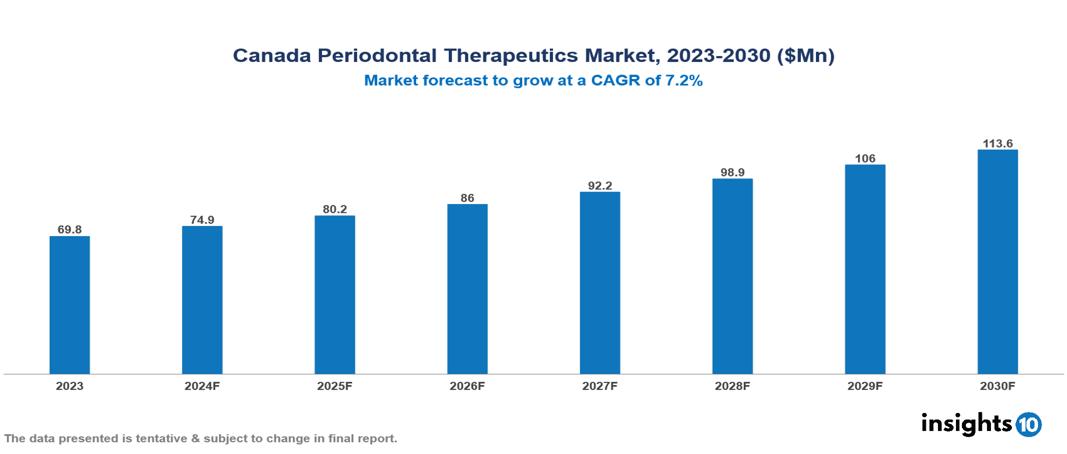

The Canada Periodontal Therapeutics Market was valued at $69.8 Mn in 2023 and is predicted to grow at a CAGR of 7.2% from 2023 to 2030, to $113.6 Mn by 2030. Canada Periodontal Therapeutics Market is growing due to Prevalence of periodontitis, Rise in Demand for Non-surgical Periodontal Therapies, and Emphasis on Preventive Oral Care. The market is primarily dominated by players such as Pfizer Inc., Lupin Ltd, Teva Pharmaceuticals USA, Sun Pharmaceutical Industries Ltd, Tokyo Chemical Industry Co. Ltd., and Bausch Health Companies Inc.

Buy Now

Canada Periodontal Therapeutics Market Executive Summary

Canada Periodontal Therapeutics Market is at around $69.8 Mn in 2023 and is projected to reach $113.6 Mn in 2030, exhibiting a CAGR of 7.2% during the forecast period.

Gum disease, sometimes referred to as periodontal disease, is a serious dental condition that is linked to infection and inflammation of the gums that surround teeth. A frequent ailment that is typically brought on by poor oral hygiene is periodontitis, which is mostly preventable with the use of therapeutic, non-surgical, or surgical treatment methods. Periodontal therapeutics, a relatively new yet profitable approach that is gaining favour with patients and dentists, comprises treating periodontitis with antibiotics alone. In periodontal therapy, metronidazole, amoxicillin, and doxycycline are often utilized antibiotics. A range of mouthwashes and rinses with antimicrobial ingredients such as hydrogen peroxide, chlorhexidine, and essential oils are adjunctive therapies for lowering gingival inflammation and plaque.

In Canada, 41% of adults with teeth have or have had, a moderate or severe periodontal problem. Demographically, it shows higher incidence rates in older adults. Healthcare expenses associated with treating periodontitis contribute substantially to Canada's dental care costs, influenced by treatments ranging from non-surgical interventions to surgical procedures. The market reflects ongoing efforts in public health and dentistry to manage and reduce the disease burden through preventive measures and effective treatments, highlighting the importance of oral hygiene and regular dental care in mitigating its prevalence and associated costs. Therefore, the market is driven by significant factors like Prevalence of periodontitis, Rise in Demand for Non-surgical Periodontal Therapies, and Emphasis on Preventive Oral Care. However, Regulatory Complications, Adverse Effects, and High Cost restrict the growth and potential of the market.

AMD Lasers announced the development of the Monet™ laser curing light, the first handheld laser in curing light for dental materials.

Market Dynamics

Market Growth Drivers

Prevalence of periodontitis: The periodontal market thrives on widespread disease prevalence. 41% of the population is still affected by periodontal disease. This health crisis fuels a robust industry of treatments, tools, and preventive products. As awareness grows and risk factors persist, the market sees continued investment and innovation, contributing significantly to the overall dental economy. The situation is worsened by increasing urbanization and changing lifestyles, contributing to a rise in oral health issues.

Rise in Demand for Non-surgical Periodontal Therapies: Demand for non-surgical treatments for periodontal diseases has increased significantly in the past few years. The treatments include periodontal scaling & root planning and usage of antibiotics, especially in severe forms of periodontal disease. Advances in pharmacologic therapies are expected to create significant opportunities for companies in the market in the next few years.

Emphasis on Preventive Oral Care: Dental practitioners emphasize preventive care, patient education, and early intervention in periodontal health management. Regular check-ups, screenings, and tailored care plans are crucial for mitigating disease progression. Professionals advocate for comprehensive approaches, including maintenance therapies, hygiene instructions, and prophylaxis services. The focus on patient-centered care ensures that treatment plans are customized to meet specific needs, promoting long-term periodontal health and overall well-being.

Market Restraints

Regulatory Complications: Canada, stringent regulatory approval processes for new periodontal treatments and technologies significantly delay market entry, hampering innovation uptake. High compliance costs and rigorous clinical trial requirements further burden market players, limiting affordability and accessibility for patients.

Adverse Effects: In Canada, one significant restraint on the periodontal market is the potential for adverse side effects from treatments such as scaling and root planing, which can include tooth sensitivity and gum irritation. These side effects may deter patients from seeking or completing necessary treatments, impacting market demand.

High cost: With dental care not fully covered by the national healthcare system, many Canadians face out-of-pocket expenses that can be prohibitive. Advanced periodontal procedures, such as dental implants and regenerative surgeries, often exceed the financial reach of average citizens, discouraging timely treatment and leading to deteriorating oral health. According to a report by the Canadian Dental Association, over 32% of Canadians do not have dental insurance, exacerbating this issue.

Regulatory Landscape and Reimbursement scenario

Periodontics market is governed by stringent regulatory frameworks aimed at ensuring patient safety and treatment efficacy. Regulations set by Health Canada and provincial dental regulatory bodies oversee aspects such as practitioner qualifications, treatment standards, and the use of dental materials. These guidelines dictate licensing requirements for periodontists, sterilization protocols for instruments, and the approval process for new treatment methodologies or technologies. Compliance with these regulations is essential for practitioners and industry stakeholders to maintain high standards of care and uphold patient trust in the dental periodontics market across Canada.

Dental insurance plans typically cover periodontal treatments to varying extents, influenced by deductibles, co-payments, and annual maximums. Direct billing by practitioners to insurance companies is common, ensuring patients receive timely reimbursements. Fee schedules and coverage policies differ among insurers, impacting treatment decisions and patient outcomes. Understanding these reimbursement dynamics is crucial for periodontists, shaping treatment planning and patient affordability while navigating the complexities of insurance guidelines. Clear communication between practitioners, insurers, and patients is essential to optimize care delivery and financial transparency in Canada's periodontics landscape.

Competitive Landscape

Key Players

Here are some of the major key players in Canada Periodontal Therapeutics Market:

- Pfizer Inc.

- Lupin Ltd

- Teva Pharmaceuticals USA, Inc.

- Sun Pharmaceutical Industries Ltd.

- Tokyo Chemical Industry Co., Ltd.

- Bausch Health Companies Inc.

- Melinta Therapeutics LLC

- Cipla, Inc.

- Chartwell Pharmaceuticals LLC.

- ASA Dental S.p.A.

- Steris-Hu-Friedy

- Carl Martin GmBH

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Canada Periodontal Therapeutics Market Segmentation

By Disease

- Gingivitis

- Chronic Periodontal Disease

- Aggressive Periodontal Disease

- Others

By Drug Type

- Doxycycline

- Minocycline

- Chlorhexidine

- Metronidazole

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Channel

By Treatment procedures

- Scaling And Root Planing

- Gum Grafting

- Regenerative Therapy

- Dental Crown Lengthening

- Periodontal Pocket Procedures

- Single Tooth Dental Implants

- Multiple Tooth Dental Implants

- others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Egypt Microspheres Market Analysis

Pharmaceuticals

UK Pharmaceutical Waste Management Market Analysis

Pharmaceuticals

Egypt Opioid Pain Management Market Analysis

Related reports (by geography)

Rare Diseases

Canada Neuroendocrine Tumor Therapeutics Market Analysis

Pharmaceuticals

Canada Ulcerative Colitis Market Analysis

Rare Diseases

Canada Fanconi Anemia (FA) Therapeutics Market Analysis

Pharmaceuticals