Pharmaceuticals

Canada Gram-Negative Infection Therapeutics Market Analysis

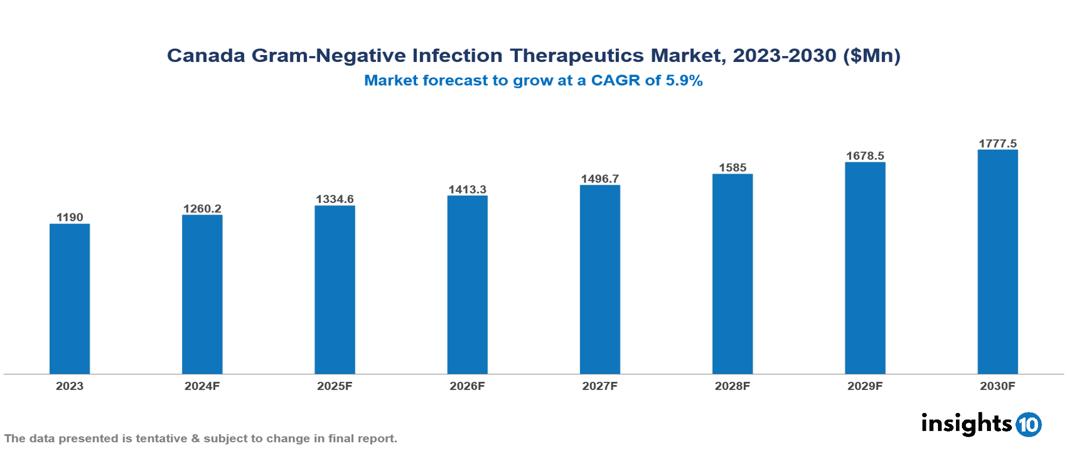

The Canada Gram-Negative Infection Therapeutics Market was valued at $1190.08 Mn in 2023 and is predicted to grow at a CAGR of 5.9% from 2023 to 2030 to $1777.5 Mn by 2030. Market dynamics are driven by the increasing incidence of infections, unmet medical needs, and favourable government initiatives. Leading companies in this market include AstraZeneca and Johnson & Johnson, among others.

Buy Now

Canada Gram-Negative Infection Therapeutics Market Executive Summary

The Canada Gram-Negative Infection Therapeutics Market was valued at $1190.08 Mn in 2023 and is predicted to grow at a CAGR of 5.9% from 2023 to 2030 to $1777.5 Mn by 2030.

Gram-Negative Bacteria (GNB) represent one of the world's most significant public health challenges due to their high antibiotic resistance. These microorganisms are essential in clinical settings, as they pose a high risk to ICU patients and contribute to significant morbidity and mortality. The Enterobacteriaceae family and non-fermenters are responsible for most clinical isolates, although other concerning gram-negative organisms include Neisseria, Haemophilus spp., Helicobacter pylori, and Chlamydia trachomatis. Gram-Negative Bacteria can cause many serious infections, such as pneumonia, wound or surgical site infections, meningitis, etc.

Canada has a rising incidence of infections, with hospital-acquired pneumonia caused by gram-negative pathogens occurring in 5 to 10 cases per 1,000 hospital admissions. Market drivers are propelled by the increasing incidence of infections, unmet medical needs, and favourable government initiatives. In contrast, market restraints include a limited pipeline of new antibiotics, antimicrobial resistance (AMR) restraint, and high costs.

Market Dynamics

Market Growth Drivers

Increasing Incidence of Infections: In Canada, the incidence of hospital-acquired pneumonia caused by gram-negative pathogens is between 5 and 10 cases per 1,000 hospital admissions. The growing incidence of gram-negative bacterial infections, particularly pneumonia and bloodstream infections, fuels the demand for effective therapeutics.

Unmet Medical Needs: The persistent challenges in treating gram-negative bacterial infections due to their unique cell wall structure and ability to develop resistance to many antibiotics create an unmet medical need that the market aims to address. Approximately 78% of Canadian physicians reported an increase in antibiotic-resistant infections in their practice over the past five years. This increases demand for effective therapeutics, thus driving the market.

Favourable Government Initiatives: Supportive government policies and funding for research and development of novel antibiotics and therapies to combat antimicrobial resistance could further propel the market in Canada. The Canadian government has invested over $100 Mn in the past decade to support antimicrobial resistance research and surveillance. This enhances growth opportunities by fostering innovation and addressing public health concerns, thus driving the market.

Market Restraints

Limited Pipeline of New Antibiotics: Over the past few decades, there has been a decline in the development of new classes of antibiotics, particularly those targeting gram-negative pathogens. Only a few new antibiotics targeting gram-negative bacteria have recently been approved in Canada, such as ceftolozane/tazobactam and ceftazidime/avibactam. This restricts market growth by limiting the availability of effective treatment options.

Antimicrobial Resistance (AMR): Restraint: The increasing prevalence of antibiotic-resistant strains of gram-negative bacteria makes existing treatments less effective. Over 30% of E. coli isolates in Canadian hospitals are resistant to third-generation cephalosporins, a critical antibiotic class for treating gram-negative infections, reducing the efficacy of existing treatments, posing a significant constraint on market expansion.

High Costs: The annual cost of antibiotic resistance in Canada is between $1.1 Bn and $2.3 Bn, with gram-negative bacteria being a significant contributor. These costs encompass hospital stays, extended treatment regimens, and supportive care for patients with infections caused by resistant strains. The high cost of treating gram-negative bacterial infections due to increasing antibiotic resistance strains a limited healthcare budget, thus limiting market growth.

Regulatory Landscape and Reimbursement Scenario

Health Canada oversees drug authorization in Canada through the Notice of Compliance (NOC) process. The Therapeutic Products Directorate (TPD) and the Biologics and Genetic Therapies Directorate (BGTD) regulate pharmaceutical drugs, ensuring they meet stringent safety, efficacy, and quality standards before receiving market authorization. Additionally, the Patented Medicine Prices Review Board (PMPRB) monitors and regulates the prices of patented medicines in the country.

The reimbursement scenario in Canada varies depending on factors such as the drug's therapeutic class and the specific provincial or territorial drug plan. Reimbursement coverage is more likely for drugs deemed essential for specific conditions or those demonstrating clinical effectiveness, ensuring access to vital treatments for Canadian patients.

Competitive Landscape

Key Players

Here are some of the major key players in the Canada Gram-Negative Infection Therapeutics Market:

- Merck & Co., Inc.

- AstraZeneca

- Johnson & Johnson

- Roche

- AbbVie Inc.

- GlaxoSmithKline plc (GSK)

- Pfizer Inc.

- Sanofi-Aventis

- Takeda Pharmaceutical Company Limited

- Nektar Therapeutics

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Canada Gram-Negative Infection Therapeutics Market Segmentation

By Drug Types:

- Antibiotics

- Combination Therapies

- Adjunctive Therapies

By Infection Types:

- Urinary Tract Infections (UTIs)

- Pneumonia

- Bloodstream Infections (Bacteremia)

- Wound/Surgical Site Infections

- Gastrointestinal Infections

- Meningitis

- Hospital-Acquired Infections (HAIs)

- Respiratory Tract Infections (RTIs)

- Other Infections

By Route of Administration:

- Oral

- Parenteral (injections, intravenous)

- Topical

By Distribution Channel:

- Hospitals

- Clinics

- Ambulatory Surgical Centres

- Home Healthcare

- Long-term Care Facilities

- Community Health Centres

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Indonesia Mouth Ulcer Therapeutics Market Analysis

Pharmaceuticals

Kuwait Antifungal Drugs Market Analysis

Pharmaceuticals

China Lipid Disorder Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Canada Anti-Venom Market Analysis

Pharmaceuticals

Canada Cord Blood Banking Service Market Analysis

Pharmaceuticals