Rare Diseases

Canada Fabry Disease Drugs Market Analysis

Canada Fabry disease drugs market is projected to grow from $xx Mn in 2023 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2023 - 2030. The market for fabry disease drugs is growing rapidly as a result of increase in incidence and prevalence of fabry disease globally, increase in awareness about the disease globally, better diagnosis rates, improved access to treatment, development of new emerging therapies, orphan drug designations provided by regulatory body?s, increase in stratergic collaborations, rise in research and development activities and approval of promising pipeline products. Chiesi Farmaceutici SpA , Sanofi, Shire ,Takeda Pharmaceutical Company Limited, Amicus Therapeutics, Inc., JCR Pharmaceuticals, Moderna are the key market players operating in global fabry disease drugs market.

Buy Now

Canada Fabry Disease Drugs Market Analysis Summary

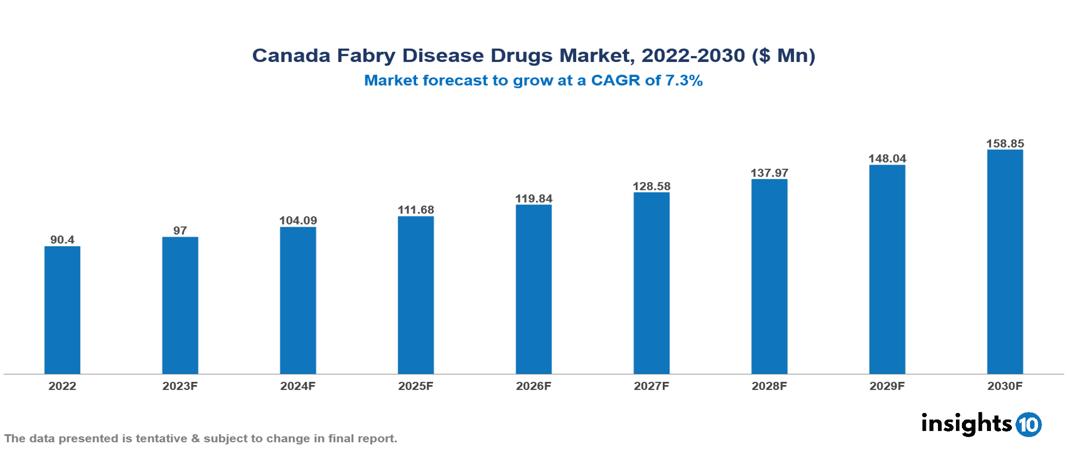

Canada Fabry Disease Drugs Market is valued at around $90.4 Mn in 2022 and is projected to reach $158.85 Mn by 2030, exhibiting a CAGR of 7.3% during the forecast period 2023-2030.

Fabry disease is a rare X-chromosome-linked genetic disease which is caused by deficient activity of a lysosomal enzyme called α-galactosidase. This results in the dysfunction of glycosphingolipid (fat) metabolism. α-galactosidase enzyme is responsible for breaking down complex sugar-lipid molecules called glycolipids or digesting particular compounds. The deficiency of this enzyme may result in cell abnormalities and organ system dysfunction which is caused by an abnormal buildup of a specific fatty matter called globotriaosylceramide in multiple tissues of the body including eyes, skin, kidney, gastrointestinal system, brain, heart, and central nervous system. Since there is no known cure for Fabry's disease, treatment options often focus on managing difficulties brought on by the disease's development and relieving symptoms. Current treatments include enzyme replacement therapy (ERT), chaperone treatment, and substrate reduction therapy (SRT). Development in oral chaperone therapy is taking place which is projected to drive the market in future years. The popularity of substrate reduction therapies and gene therapies in the market is also expected to increase.

Market Dynamics

Market Drivers

Increase in incidence and prevalence of Fabry disease – As the patient population suffering from this disease increase this acts as a market growth driver.

An increase in awareness about the disease globally is a market growth driver

The increase in the prevalence and adoption of novel therapies like chaperone treatment, substrate therapy and gene therapy acts as a market growth driver. Chaperone therapy includes oral small molecules, which aim to stabilize and enhance the function of the deficient enzyme.

Extensive research and development activities and collaborations between pharmaceutical companies and research organizations also act as market growth drivers.

Orphan Drug Designations provided by regulatory bodies also act as a growth driver.

Market Restraints

Side effects associated with treatment options and high treatment costs act as a market growth restraint

A lower rate of diagnosis due to a lack of technologies and the late onset of symptoms also acts as a market growth restraint.

Key players

Alexion Pharmaceuticals Genzyme Corporation BioMarin Pharmaceutical Inc Shire plc Genzyme Corporation BioMarin Pharmaceutical Inc Alexion Pharmaceuticals Shire plc BioMarin Pharmaceutical Inc1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Market Segmentations For Canada Fabry disease drugs market

By Type

- Classic Fabry disease

- Atypical late-onset Fabry disease

By Treatment type

- Enzyme replacement therapy (ERT)

- Chaperone treatment

- Substrate reduction therapy (SRT)

- Others

By Mechanism of action

- Alpha-galactosidase A (Alpha-Gal A) agonist

- Globotriaosylceramide (GL-3) deposition reducer

- Pancreatic replacement enzymes

- Pain management

- Others

By Route of Administration

- Oral

- Parenteral

By end users

- Hospitals

- Homecare

- Speciality clinics

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Related reports (by geography)

Pharmaceuticals

Canada Dry Eye Medication Market Analysis

Pharmaceuticals