Pharmaceuticals

Canada Dermatology Prescription Market Analysis

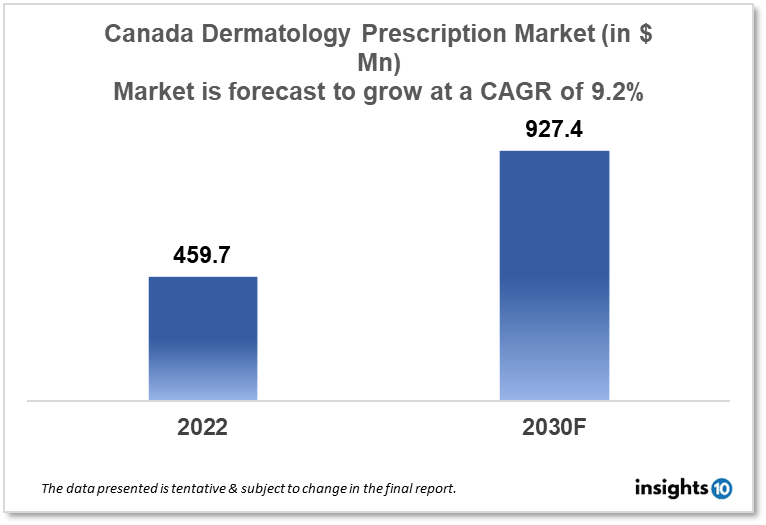

Canada's dermatology prescription market is expected to grow from $459.7 Mn in 2022 to $927.4 Mn in 2030 with a CAGR of 9.2% for the year 2022-30. Rising incidences of dermatology disorders involving the skin, nails, hair, etc, and the demand for novel therapeutics for the treatment of dermatology disorders in Canada are major market drivers of the Canadian dermatology prescription market. the market is segmented by disease type, drug class, route of administration, end-user, and by distribution channel. Affinium, Pfizer, and Sanofi are some of the key players in Canada's dermatology prescription market.

Buy Now

Canada Dermatology Prescription Market Executive Analysis

Canada's dermatology prescription market size is at around $459.7 Mn in 2022 and is projected to reach $927.4 Mn in 2030, exhibiting a CAGR of 9.2% during the forecast period. According to current projections, Canada's health spending will reach $331 Bn in 2022. According to Canadian Institute for Health Information (CIHI), the average cost of healthcare in Canada will be $8,653 per person, with the total cost of healthcare accounting for 12.2% of GDP, down from 13.8 % in 2020. As the number of claims for speciality pharmaceuticals rises and the cost of treating chronic conditions increases per person, spending on drugs is expected to rise by 5.4% in 2022.

Dermatology problems are more prevalent in Canada. Over half of all Canadians will suffer these skin issues throughout their lifetime, according to the Canadian Dermatology Association. Eczema (atopic dermatitis), acne, birthmarks, psoriasis, hair loss, vitiligo, molluscum, and warts are the conditions that are most frequently observed in Canada. Of all cancers, skin cancers are the most common in Canada. 6,800 new instances of cutaneous melanoma and 78,300 new cases of non-melanoma skin cancer were estimated by the Canadian Cancer Society. Topical corticosteroids for skin inflammation and irritation, topical retinoids for acne and wrinkles, oral antibiotics for acne, oral antifungal medications for fungal infections, topical or oral immunomodulators for atopic dermatitis, and topical or oral medications for psoriasis are some common prescription drugs used for dermatological conditions in Canada. The development of more egalitarian, varied, and inclusive dermatological care in Canada and around the world has advanced significantly. The Temerty Faculty of Medicine at the University of Toronto has received a $3 Mn grant from AbbVie, a multinational biopharmaceutical business with a focus on research and development. This is one of the first chairs of its sort to be established globally.

Market Dynamics

Market Growth Drivers

Increasing levels of disposable income among people, rising awareness of one's appearance among people around the world, rising numbers of patients with infectious diseases affecting the skin, nails, and hair, rising demand for homeopathy dermatology therapeutics due to their affordability, high efficacy, and safety, and rising preferences for biologics in developing new dermatological treatment solutions with distinctive organic components by various pharma companies are some of the major factors resulting in the growth of Canada dermatology prescription market.

Market Restraints

More stringent healthcare restrictions by healthcare authorities, along with rising concerns about the quality and safety of prescription drugs, are anticipated to act as market barriers to the growth of the Canada dermatology prescription market.

Competitive Landscape

Key Players

- Octapharma (CAN)

- Oxalys (CAN)

- Dalton (CAN)

- Attix (CAN)

- Affinium (CAN)

- Pfizer

- Sanofi

- GlaxoSmithKline

- Novartis

- Johnson & Johnson

Healthcare Policies and Regulatory Landscape

Health Canada is responsible for assisting Canadians in maintaining and improving their health. It seeks to lower health risks and guarantees that high-quality healthcare is accessible. Health Canada is the organization in charge of controlling the prescription use of dermatology medications in Canada. All prescription medications must first be reviewed and approved by Health Canada before they may be advertised and sold in Canada. Based on data from clinical studies and other scientific evidence, it assesses each medicine's safety and efficacy, and it keeps track of those factors once the drug is on the market. In addition to Health Canada, professional associations like the Canadian Society of Dermatologic Surgery and the Canadian Dermatology Association also offer recommendations and guidelines for the use of dermatology drugs in Canada.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Dermatology Prescription Market Segmentation

By Disease Type

- Acne

- Dermatitis

- Psoriasis

- Skin Cancer

- Alopecia

- Rosacea

By Drug Class

- Anti-infectives

- Corticosteroids

- Calcineurin inhibitors

- Retinoids

- Antirheumatic

By Route of Administration

- Oral

- Topical

- Parenteral Administration

By End User

- Home Care

- Hospital

- Dermatology Clinics

By Distribution Channel

- Pharmacy Store

- Retail Store

- Online

- Supermarkets

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

UK Respiratory Drugs Market Analysis

Pharmaceuticals

Malaysia Interstitial Cystitis Drugs Market Analysis

Related reports (by geography)

Healthcare Services

Canada Hospital Market Analysis

Rare Diseases

Canada Freidreich's Ataxia Market Analysis

Pharmaceuticals