Digital Health

Canada Artificial Intelligence (AI) in Diagnostics Market Analysis

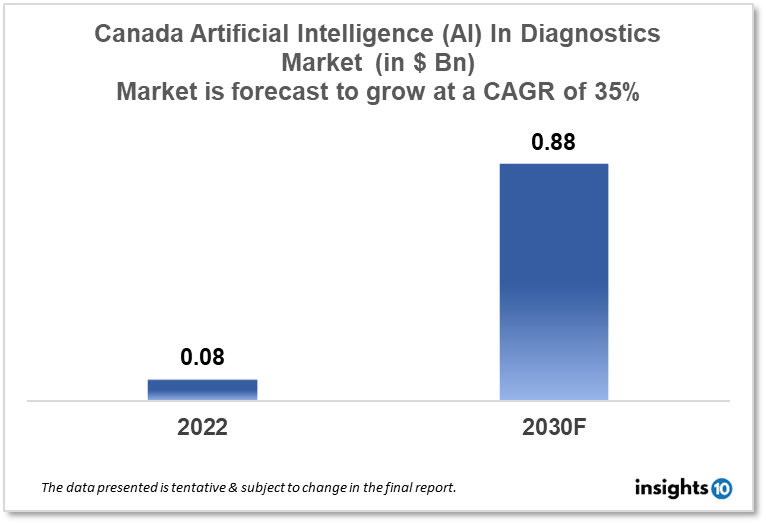

Canada's Artificial Intelligence (AI) in the diagnostics market is projected to grow from $0.08 Bn in 2022 to $0.88 Bn by 2030, registering a CAGR of 35% during the forecast period of 2022 - 2030. The market will be driven by a growing burden on the healthcare system and increasing investment in AI R&D and the formation of a robust AI ecosystem in Canada. The market is segmented by component & by diagnosis. Some of the major players include IBM Watson Health, Siemens Healthineers & Imagia.

Buy Now

Canada Artificial Intelligence (AI) In Diagnostics Market Executive Summary

Canada's Artificial Intelligence (AI) in the diagnostics market is projected to grow from $0.08 Bn in 2022 to $0.88 Bn by 2030, registering a CAGR of 35% during the forecast period of 2022 - 2030. In Canada, according to a new Fraser Institute analysis, a family of two adults and two children with an average household income of $156,086 was projected to spend an estimated $15,847 on public healthcare in 2022. Citizens of Canada, as well as foreigners who qualify for permanent residency, have access to a single-payer, universal healthcare system.

The use of diagnostic AI in Canada is quickly growing, with many fascinating research and efforts happening in a variety of disciplines of medicine such as Radiology, Pathology, Oncology, Cardiology, Neurology, and others. While there are still obstacles to overcome, such as legal constraints and data availability concerns, the potential advantages of diagnostic AI are enormous, and it is expected to play a growing role in Canadian healthcare in the coming years. Artificial intelligence (AI) is set to have a significant influence on medical practice in Canada. The Augmented Intelligence and Precision Health Laboratory (AIPHL) at McGill University Health Centre (MUHC) in Montreal was employing GE's Edison platform and machine learning technologies to forecast the progression of head and neck squamous cell carcinoma to the cervical lymph nodes. The federal government submitted Bill C-27, titled The Digital Charter Implementation Act, 2022, on June 16, 2022. The bill's introduction of the Artificial Intelligence and Data Act is one of its three cornerstones (AIDA).

Market Dynamics

Market Growth Drivers

The Ontario government created the "Artificial Intelligence (AI) Strategy" to encourage the research and use of AI in healthcare. The initiative emphasizes the application of AI for diagnostic imaging, particularly the creation of AI tools for the early diagnosis of illnesses like breast cancer. Various researches have been carried out in the field of cancer diagnostics and radiology by researchers at universities such as McGill University, The University of Alberta & Dalhousie University in Halifax which have the potential to enhance diagnosis accuracy, boost efficiency, and lower healthcare costs, eventually benefiting both patients and providers.

Increasing adoption of more accurate and timely diagnostic tools, a growing burden on the healthcare system including rising healthcare costs and a dearth of healthcare providers, and a rising preference for the use of AI and other modern applications in healthcare, both in Canada and globally. This has resulted in increasing investment in AI R&D and the formation of a robust AI ecosystem in Canada. As a result, there is enormous potential for AI diagnostics to revolutionize the Canadian healthcare scene in the coming years.

Market Restraints

According to a 2022 study, 63% of Canadians perceive the national healthcare system's top concern is a shortage of workers. Access to therapy and/or excessive wait periods were also deemed critical difficulties. The most common concern among adopters of AI was making a bad strategic decision based on AI suggestions. There are significant organizational challenges in adapting and deploying AI. Then there were concerns about cybersecurity breaches and unspecified legal liability for AI system judgments, as well as unintended consequences caused by AI-powered decisions made by both corporations and consumers.

Competitive Landscape

Key Players

- IBM Watson Health

- Siemens Healthineers

- Philips Healthcare

- GE Healthcare

- Google Health

- AliveCor, Inc

- Riverain Technologies

- Imagia (CAN)

- DarwinAI (CAN)

- CorVista (CAN)

Notable Deals

- February 2023, GE HealthCare to Acquire Caption Health The acquisition adds AI-enabled image guiding to the ultrasound device portfolios of GE HealthCare's $3 billion Ultrasound division

- November 2022, During RSNA 2022, Philips promotes AI-powered diagnostic technologies and transformational workflow solutions

- In November 2022, Google Health reached an agreement with iCAD to commercialize mammography AI

Healthcare Policies and Regulatory Landscape & Reimbursement Scenario

Health Canada is in charge of overseeing the regulation of medical equipment, including AI diagnostics. Before permitting medical devices to be sold in Canada, they evaluate their safety, efficacy, and quality. Before medical products, including AI diagnostics, may be commercialized in Canada, they must first receive a Medical Device License from Health Canada. The Canadian Agency for Drugs and Technologies in Health (CADTH) is a national organization in Canada that conducts analysis and research for healthcare decision-makers regarding the usage of technologies.

AI diagnostics are normally reimbursed by public health insurance programs in each province and territory. Each insurer has its own method for analyzing the clinical and cost-effectiveness of healthcare technology, including AI diagnostics, before determining whether to cover them.

1. Executive Summary

1.1 Digital Health Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Digital Health Policy in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Artificial Intelligence (AI) in Diagnostics Market Segmentation

- By Component Outlook Type (Revenue, USD Billion):

- Software

- Hardware

- Services

- By Diagnosis Outlook Type (Revenue, USD Billion):

- Cardiology

- Oncology

- Pathology

- Radiology

- Chest and Lung

- Neurology

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Digital Health

Nigeria Digital Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Canada Head and Neck Cancer Drugs Market Analysis

Medical Devices

Canada Pain Management Devices Market Analysis

Rare Diseases

Canada Wilson?s Disease Therapeutics Market Analysis

Rare Diseases