Canada Alopecia (Hair Loss) Therapeutics Market Analysis

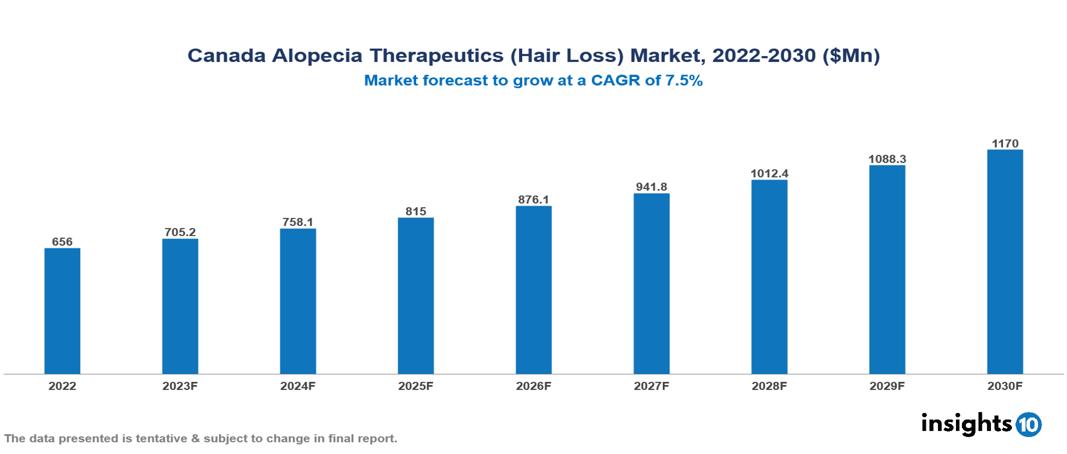

The Canada Alopecia (Hair Loss) Therapeutics Market was valued at US $0.65 Bn in 2022, and is predicted to grow at (CAGR) of 7.50% from 2023 to 2030, to US $1.17 Bn by 2030. The key drivers of this industry include the upward trend in the prevalence of Alopecia (hair loss), improved treatment options. The industry is primarily dominated by players such as Eli Lilly, Pfizer, Allergan, Valeant, Bayer, Roche, AbbVie among others.

Buy Now

Canada Alopecia Therapeutics Market Analysis: Executive Summary

The Canada Alopecia (Hair Loss) Therapeutics Market is at around US $0.65 Bn in 2022 and is projected to reach US $1.17 Bn in 2030, exhibiting a CAGR of 7.50% during the forecast period.

Alopecia, characterized by the occurrence of patchy hair loss, affects a considerable number of individuals. The predominant form, Alopecia areata, is an autoimmune disorder resulting in circular or oval areas of hair loss. The most common symptoms include sudden or gradual hair loss, itching, and alterations in the nails. However, there are various treatment alternatives. Topical medications such as Minoxidil or corticosteroids can be directly applied to the scalp, while injections and oral medications provide more potent immunosuppressive effects. Light therapy and hair transplantation are also viable options. Companies like Eli Lilly, with their JAK inhibitor Baricitinib, and Bayer, with Rogaine (Minoxidil), are at the forefront of developing treatment advancements in addressing this condition.

The prevalence of Alopecia in Canada is estimated to be approximately 2% in both males and females. The market is propelled by significant factors such as the growing aging population at a risk of developing Alopecia, improved treatment options and increased government initiatives and consumer knowledge of the therapeutics industry. However, high treatment costs like JAK inhibitors, transplantation and limited coverage are few factors that limit the market's potential.

Market Dynamics

Market Growth Drivers

Surge in the prevalence of Alopecia: The estimated prevalence of Alopecia in Canada is approximately 2% in both the genders. The country is experiencing a surge in the prevalence of Alopecia Areata. The demand in the market is propelled by Canada's aging population, which faces a high risk of alopecia, creating a larger pool of patients in need of regular treatments, and the rising immigration patterns, which introduce diverse populations susceptible to various types of hair loss.

Enhanced treatment options: The field of Alopecia therapeutics is expanding, incorporating innovative options such as JAK inhibitors and gene therapy, which present the potential for enhanced effectiveness and less invasive treatment alternatives. Advances in diagnostic tools, including trichoscopy and genetic testing, contribute to early detection and personalized treatment strategies, thereby increasing overall market demand.

Government initiatives: The increased scope of health insurance coverage, particularly in regions such as Ontario, has the potential to enhance accessibility to costlier Alopecia treatments. Groups such as the Canadian Alopecia Areata Foundation and Canadian Dermatology Association actively work towards spreading awareness promoting early diagnosis and treatment.

Market Restraints

High costs of treatment: Oral JAK inhibitors and hair transplantation procedures come with substantial expenses, often surpassing the healthcare budgets of the majority of Canadians. This financial strain poses a barrier to access for many individuals, either relying on limited insurance coverage or finding themselves unable to afford the treatment altogether.

Limited coverage: Despite the universal coverage in Canadian healthcare, certain Alopecia treatments such as JAK inhibitors are not comprehensively covered by all provincial plans. This situation may result in patients having to bear co-payments which results in treatment non-compliance in many patients which restricts market growth.

Notable Updates

December 2023, LITFULO™ (ritlecitinib), a dual JAK3/TEC inhibitor from Pfizer, has received approval from Health Canada for the treatment of severe Alopecia areata in adults and adolescents aged 12 and above.

Healthcare Policies and Regulatory Landscape

The Canada Health Act (CHA) delineates the fundamental objectives of Canadian healthcare policy and governs the publicly funded healthcare system in the country. The policy strives to "safeguard, promote, and restore the physical and mental well-being of residents of Canada and to ensure reasonable access to health services without direct charges at the point of service for such services." The CHA establishes criteria that provinces and territories must meet to qualify for federal funding for both extended health care services and covered health services.

Acquiring a medical license in Canada involves a region-specific process mandated by Health Canada (HC), typically requiring the completion of a medical degree, residency training, and successful passage of licensing examinations.

Competitive Landscape

Key Players

- Eli Lilly

- Pfizer

- Bayer

- Allergan

- AbbVie

- Valeant Pharmaceuticals

- Stemson Therapeutics

- OliX Pharmaceuticals

- Aclaris

- Roche

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Canada Alopecia Therapeutics Market Segmentation

By Disease Type

- Alopecia Areata

- Cicatricial Alopecia

- Traction Alopecia

- Alopecia Totalis

- Androgenetic Alopecia

- Alopecia Universalis

- Others

By Treatment Type

- Pharmaceuticals

- Devices

- Others

By Gender

- Male

- Female

By Route of Administration

- Topical

- Injectable

- Oral

By Age Group

- Below 18 years

- 18-34 years

- 35-49 years

- 50 years and above

By End User

- Hospitals

- Physician’s Office

- Dermatology clinics

- Others

By Sales Channel

- Prescriptions

- OTC

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

China Blood Plasma Market Analysis

France Oncology/Cancer Drugs Market Analysis

Related reports (by geography)

Canada Top Selling Biologics Market Analysis

Canada Erythropoietin Drugs Market Analysis

Canada Paracetamol Market Analysis