Pharmaceuticals

Belgium Oncology Therapeutics Market Analysis

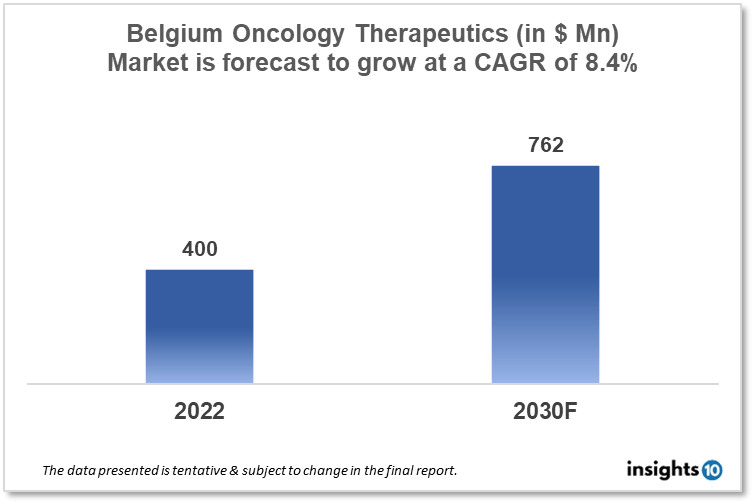

By 2030, it is anticipated that the Belgium Oncology Therapeutics Market will reach a value of $762 Mn from $400 Mn in 2022, growing at a CAGR of 8.9% during 2022-2030. The Oncology Therapeutics Market in Belgium is dominated by a few domestic pharmaceutical companies such as Hyloris Pharmaceuticals, OncoDNA, and Iteos Therapeutics. The Oncology Therapeutics Market in Belgium is segmented into different types of cancer and different therapy types. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for Belgium Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

Belgium Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the Belgium Oncology Therapeutics Market will reach a value of $762 Mn from $400 Mn in 2022, growing at a CAGR of 8.9% during 2022-30.

Belgium is a high-income, developed country in Western Europe that borders the North Sea. The Belgian Cancer Registry (BCR) is a population-based registry that began nationwide coverage in 2004. The statistics from the Belgian Cancer Registry are comprehensive and nationally representative. Belgium has a high cancer rate, with 44,452 new cancer cases in males and 38,815 new cancer cases in females in 2020, according to a WHO report.

In Belgium, 68.782 new cancer cases were recorded in 2020. Prostate, lung, and colorectal cancer are the three most frequent kinds of cancer in males. Breast, colorectal, and lung cancer are the most common cancers in women. This ranking also applies to those aged 70 and up. Belgium's government spent 11.1% of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

Since 2006, the number of new cancer diagnoses in both men and women has grown, owing in part to population ageing. Women's incidence has only increased after controlling for age. With 24 radiation treatment centres and 13 satellite facilities, Belgium has the highest RT equipment density in the world. Cancer care is now mandated to be organised in multidisciplinary care programmes guided by structural and volume indicators, thanks to the 2008 National Cancer Plan (NCP) support. Belgium is currently conducting cutting-edge research into various kinds of the disease and provides first-world care to everyone suffering from cancer, despite claims that the country underutilizes radiotherapy. These aspects could boost Belgium Oncology Therapeutics Market.

Market restraints

Health insurance in Belgium is supplied by a group of primarily private insurers. These health insurers are private companies, but they are state-approved and strictly regulated. In Belgium, new systemic anticancer therapies are difficult to obtain. Because Belgian health insurance is based on a co-pay reimbursement model, you may have to pay some out-of-pocket expenses for portion of your oncological treatment. These factors may deter new entrants into the Belgium Oncology Therapeutics Market.

Competitive Landscape

Key Players

- Iteos Therapeutics - Iteos Therapeutics is a Belgian biotechnology company that focuses on developing cancer immunotherapies. They have a pipeline of oncology therapeutics, including drugs for treating solid tumours and haematological malignancies

- OncoDNA - OncoDNA is a Belgian biotechnology company that specializes in the development of precision oncology solutions. They provide genomic testing services to healthcare providers to help them make informed treatment decisions for cancer patients

- Hyloris Pharmaceuticals - Hyloris Pharmaceuticals is a Belgian biopharmaceutical company that focuses on the development of oncology drugs and other therapeutic products. They have a pipeline of oncology therapeutics, including drugs for the treatment of breast cancer and pancreatic cancer

- iTeos Therapeutics - iTeos Therapeutics is a Belgian biopharmaceutical company that focuses on developing cancer immunotherapies. They have a pipeline of oncology therapeutics, including drugs for treating solid tumours and haematological malignancies

- BePharBel Manufacturing - BePharBel Manufacturing is a Belgian pharmaceutical company that specializes in the development and production of oncology drugs

Recent Notable Updates

January 2023: DeuterOncology, based in Liege, Belgium, is a clinical-stage medication research firm seeking to advance in this sector. The Belgian business has now acquired $6.1 Mn in Series A funding from Belgian venture capitalists Newton Biocapital, Noshaq (who also backed Eclo and LiveDrop), and Investsud Tech. According to the firm news release, the cash will be used to begin Phase I clinical research for its main product, DO-2, an enhanced MET kinase inhibitor being developed to treat lung cancer.

Healthcare Policies and Reimbursement Scenarios

In Belgium, the administrative body liable for supporting and observing oncology therapeutics is the Federal Agency for Medicines and Health Products (FAMHP). Regarding repayment, Belgium has a required healthcare coverage program known as the National Institute for Health and Disability Insurance (INAMI). Furthermore, a few non-governmental organizations (NGOs) give monetary help to disease patients who cannot manage the cost of their medicines.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Egypt Cholesterol / Lipid Lowering Drugs Market Analysis

Pharmaceuticals

Philippines Mouth Ulcer Therapeutics Market Analysis

Pharmaceuticals

Germany Infectious Disease Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Belgium Obesity Drugs Market Analysis

Pharmaceuticals

Belgium Dermatological Therapeutics Market Analysis

Pharmaceuticals

Belgium Liver Disease Drugs Market Analysis

Healthcare Services