Pharmaceuticals

Belgium Cardiovascular Diseases Therapeutics Market Analysis

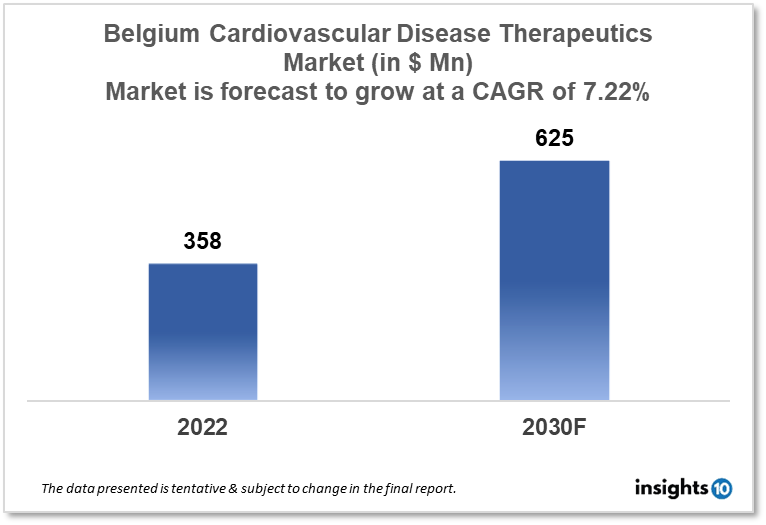

Belgium's cardiovascular disease therapeutics market is projected to grow from $358 Mn in 2022 to $625 Mn in 2030 with a CAGR of 7.22% for the year 2022-30. The major market drivers include the increasing aging population and supportive reimbursement policies in Belgium. The Belgium cardiovascular disease therapeutics market is segmented by disease indication, drug type, route of administration, drug classification, mode of purchase, and by end user. Galapagos, Ablynx, and UCB are the major players in the Belgian cardiovascular disease therapeutics market.

Buy Now

Belgium Cardiovascular Disease Therapeutics Market Executive Analysis

Belgium's cardiovascular disease therapeutics market size is at around $358 Mn in 2022 and is projected to reach $625 Mn in 2030, exhibiting a CAGR of 7.22% during the forecast period. With a score of 51.99, Belgium is ranked ninth overall in the World Index of Healthcare Innovation. In both 2021 and 2022, Belgium was placed ninth. Belgium's success in science and technology is superior to that of other nations. (8th overall, with the second highest R&D spending per capita among Index countries). For fiscal sustainability, Belgium comes in at number 10. The third-lowest in the Index in terms of public healthcare expenditure is Belgium, but the country's fiscal trajectory is on the wrong track. As public healthcare spending rises, Belgium falls into the bottom third of the Index (22nd). Given Belgium's even lower (23rd) national solvency ranking and alarmingly high debt-to-GDP ratio, the country's increased public healthcare expenditure is particularly concerning. Due to its tax code, which gives net income from intellectual property an 85% discount, Belgium is home to a varied and expanding innovative biotechnology industry. Due to the discount, Belgian-based innovative drug firms pay an effective income tax rate of 3.8 %.

With an estimated 4 Mn fatalities per year and 25% of all-cause disability-adjusted life years (DALYs), cardiovascular disease (CVD) is the main cause of death in Europe. In Belgium, CVDs are responsible for 28.8% of all fatalities and 14.2% of all DALYs. Anticoagulants, antiplatelet agents, and lipid-lowering drugs are just a few of the modern medicine that has been created in Belgium for the therapy of CVD. Clinical studies of these drugs have yielded encouraging results, and it is anticipated that their use will lower the incidence of CVD and enhance patient outcomes. A significant advancement in CVD therapeutics has been the creation of personalized medicine. Personalized medicine is being used in Belgium to identify patients who are at high risk for CVD and to customize therapies based on unique patient traits. In Belgium, minimally invasive procedures like transcatheter aortic valve replacement (TAVR) and percutaneous coronary intervention (PCI) are now broadly accessible. These methods have been demonstrated to lower morbidity and mortality rates in CVD patients because they are less invasive than conventional surgery.

Market Dynamics

Market Growth Drivers

Ageing populations are more prone to cardiovascular illnesses, which is the case in Belgium. The demand for cardiovascular disease treatments is anticipated to rise as a result, especially among the aged. Belgium is at the forefront of technological advancements in healthcare and has a robust healthcare system. This is anticipated to stimulate the creation of novel therapeutics for cardiovascular illness, which might spur the Belgium cardiovascular disease therapeutics market expansion. The reimbursement of medical services, including treatments for cardiovascular disease, is advantageous in Belgium. This is anticipated to improve patient access to therapeutics for cardiovascular diseases and spur market expansion.

Market Restraints

The cost of treating the cardiovascular disease may thwart some patients from receiving therapy. The intricacy of Belgium's regulatory atmosphere may cause delays in the approval of new medications and increase research costs. Since Belgium has an inadequate healthcare budget, the government may decide to devote more money to other aspects of healthcare, which could decrease capital for cardiovascular disease treatments thereby hampering the growth of Belgium's cardiovascular disease therapeutics market.

Competitive Landscape

Key Players

- Neogen (BEL)

- Mirrhia (BEL)

- Tilman (BEL)

- Galapagos (BEL)

- Ablynx (BEL)

- UCB

- Janssen

- AstraZeneca

- Merck

- Sanofi

- Novartis

- Daiichi Sankyo

Healthcare Policies and Regulatory Landscape

Most healthcare providers are commercial. Six of the seven major national associations of disease funds, which provide health insurance to Belgians, are private non-profits. The Commission for the Reimbursement of Pharmaceuticals negotiates prescription drug settlements, with the Belgian Minister of Social Affairs making the final choices. The Belgian government also establishes a yearly global budget for public pharmaceutical expenditure and mandates that pharmaceutical companies pay back the government for any expenditures that are in surplus of that budget. The Bismarckian health insurance system in Belgium is less expensive than those in analogous nations (the Czech Republic is the only one). Moreover, despite having a world-class selection of providers (tied for first), the nation lacks competent access to both innovative drug treatments and generic medicines.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiovascular Disease Therapeutics Segmentation

By Disease Indication (Revenue, USD Billion):

- Hypertension

- Coronary Artery Disease

- Hyperlipidaemia

- Arrhythmia

- Others

By Drug Type (Revenue, USD Billion):

- Antihypertensive

- Anticoagulants

- Antihyperlipidemic

- Antiplatelet Drugs

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Drug Classification (Revenue, USD Billion):

- Branded Drugs

- Generic Drugs

By Mode of Purchase (Revenue, USD Billion):

- Prescription-Based Drugs

- Over-The-Counter Drugs

By End Users (Revenue, USD Billion):

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Vietnam Pressure Sensor Market Analysis

Pharmaceuticals

UAE Pigments Market Analysis

Related reports (by geography)

Healthcare Services

Belgium Home Healthcare Market Analysis

Pharmaceuticals

Belgium Vitamin and Minerals Market Analysis

Pharmaceuticals

Belgium Cancer Immunotherapy Market Analysis

Medical Devices